Advertisement

Don't Buy Nepa AB (publ) (STO:NEPA) For Its Next Dividend Without Doing These Checks

Readers hoping to buy Nepa AB (publ) (STO:NEPA) for its dividend will need to make their move shortly, as the stock is about to trade ex-dividend. The ex-dividend date is two business days before a company's record date in most cases, which is the date on which the company determines which shareholders are entitled to receive a dividend. The ex-dividend date is important because any transaction on a stock needs to have been settled before the record date in order to be eligible for a dividend. Therefore, if you purchase Nepa's shares on or after the 24th of June, you won't be eligible to receive the dividend, when it is paid on the 30th of June.

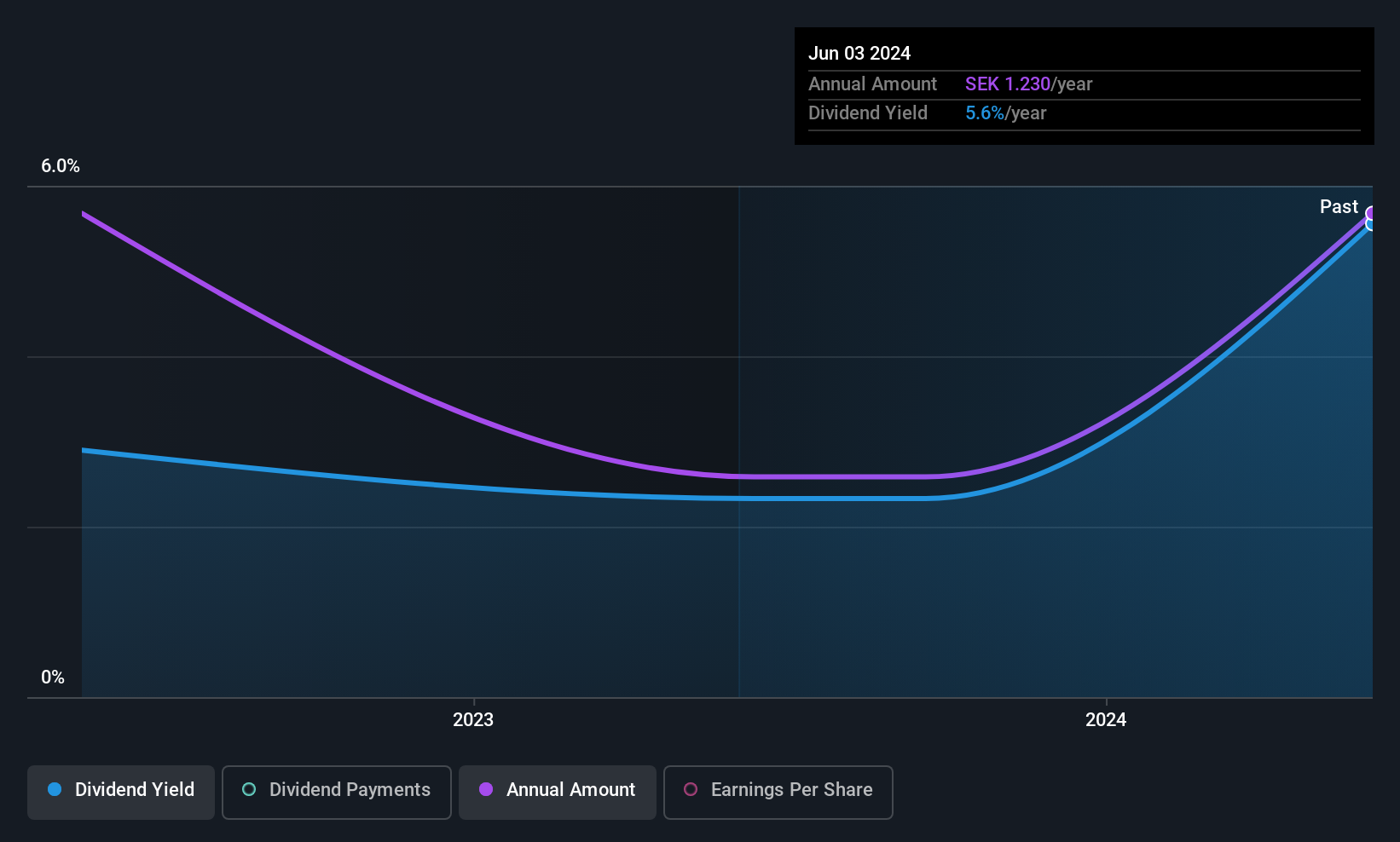

The company's next dividend payment will be kr01.23 per share, and in the last 12 months, the company paid a total of kr1.23 per share. Calculating the last year's worth of payments shows that Nepa has a trailing yield of 6.6% on the current share price of kr018.60. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. We need to see whether the dividend is covered by earnings and if it's growing.

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Nepa reported a loss after tax last year, which means it's paying a dividend despite being unprofitable. While this might be a one-off event, this is unlikely to be sustainable in the long term. Considering the lack of profitability, we also need to check if the company generated enough cash flow to cover the dividend payment. If Nepa didn't generate enough cash to pay the dividend, then it must have either paid from cash in the bank or by borrowing money, neither of which is sustainable in the long term. It paid out 96% of its free cash flow in the form of dividends last year, which is outside the comfort zone for most businesses. Cash flows are usually much more volatile than earnings, so this could be a temporary effect - but we'd generally want to look more closely here.

View our latest analysis for Nepa

Click here to see how much of its profit Nepa paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Businesses with shrinking earnings are tricky from a dividend perspective. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. Nepa reported a loss last year, and the general trend suggests its earnings have also been declining in recent years, making us wonder if the dividend is at risk.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. Nepa's dividend payments are effectively flat on where they were three years ago. When earnings are declining yet the dividends are flat, typically the company is either paying out a higher portion of its earnings, or paying out of cash or debt on the balance sheet, neither of which is ideal.

Remember, you can always get a snapshot of Nepa's financial health, by checking our visualisation of its financial health, here.

The Bottom Line

Should investors buy Nepa for the upcoming dividend? It's hard to get used to Nepa paying a dividend despite reporting a loss over the past year. Worse, the dividend was not well covered by cash flow. It's not that we think Nepa is a bad company, but these characteristics don't generally lead to outstanding dividend performance.

Although, if you're still interested in Nepa and want to know more, you'll find it very useful to know what risks this stock faces. Every company has risks, and we've spotted 3 warning signs for Nepa (of which 2 don't sit too well with us!) you should know about.

Generally, we wouldn't recommend just buying the first dividend stock you see. Here's a curated list of interesting stocks that are strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if Nepa might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:NEPA

Nepa

Operates as a consumer research and analytics company in Sweden and internationally.

Excellent balance sheet with low risk.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor