Advertisement

- Sweden

- /

- Medical Equipment

- /

- OM:INTEG B

We're Hopeful That Integrum (STO:INTEG B) Will Use Its Cash Wisely

There's no doubt that money can be made by owning shares of unprofitable businesses. For example, biotech and mining exploration companies often lose money for years before finding success with a new treatment or mineral discovery. But while history lauds those rare successes, those that fail are often forgotten; who remembers Pets.com?

So should Integrum (STO:INTEG B) shareholders be worried about its cash burn? For the purpose of this article, we'll define cash burn as the amount of cash the company is spending each year to fund its growth (also called its negative free cash flow). The first step is to compare its cash burn with its cash reserves, to give us its 'cash runway'.

How Long Is Integrum's Cash Runway?

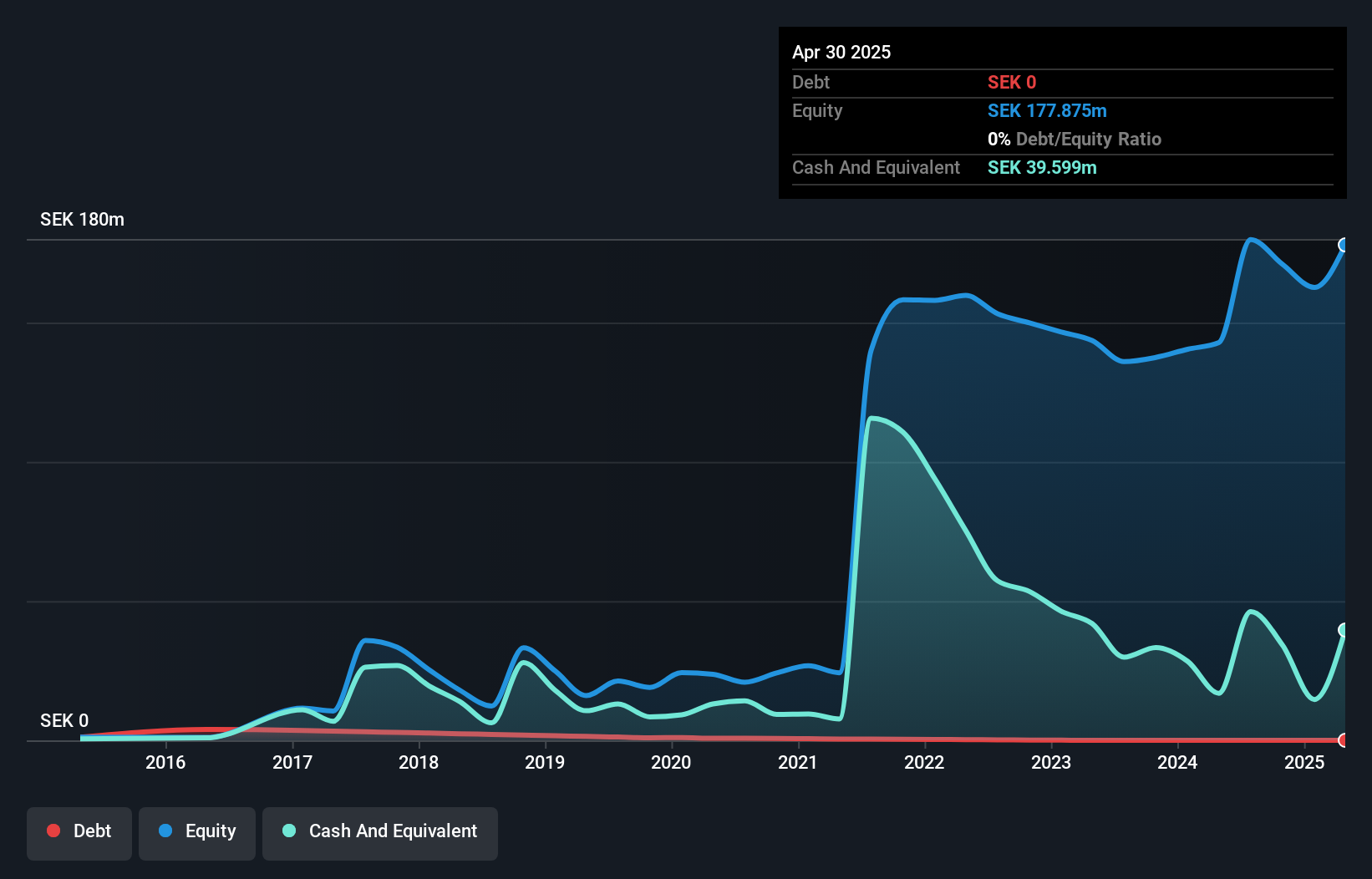

A company's cash runway is calculated by dividing its cash hoard by its cash burn. In April 2025, Integrum had kr40m in cash, and was debt-free. Importantly, its cash burn was kr51m over the trailing twelve months. That means it had a cash runway of around 9 months as of April 2025. Notably, analysts forecast that Integrum will break even (at a free cash flow level) in about 2 years. Essentially, that means the company will either reduce its cash burn, or else require more cash. Depicted below, you can see how its cash holdings have changed over time.

Check out our latest analysis for Integrum

How Well Is Integrum Growing?

Notably, Integrum actually ramped up its cash burn very hard and fast in the last year, by 108%, signifying heavy investment in the business. While that's concerning on it's own, the fact that operating revenue was actually down 12% over the same period makes us positively tremulous. Taken together, we think these growth metrics are a little worrying. Clearly, however, the crucial factor is whether the company will grow its business going forward. For that reason, it makes a lot of sense to take a look at our analyst forecasts for the company.

Can Integrum Raise More Cash Easily?

Since Integrum can't yet boast improving growth metrics, the market will likely be considering how it can raise more cash if need be. Generally speaking, a listed business can raise new cash through issuing shares or taking on debt. Many companies end up issuing new shares to fund future growth. We can compare a company's cash burn to its market capitalisation to get a sense for how many new shares a company would have to issue to fund one year's operations.

Since it has a market capitalisation of kr879m, Integrum's kr51m in cash burn equates to about 5.8% of its market value. That's a low proportion, so we figure the company would be able to raise more cash to fund growth, with a little dilution, or even to simply borrow some money.

How Risky Is Integrum's Cash Burn Situation?

On this analysis of Integrum's cash burn, we think its cash burn relative to its market cap was reassuring, while its increasing cash burn has us a bit worried. Shareholders can take heart from the fact that analysts are forecasting it will reach breakeven. Cash burning companies are always on the riskier side of things, but after considering all of the factors discussed in this short piece, we're not too worried about its rate of cash burn. Separately, we looked at different risks affecting the company and spotted 3 warning signs for Integrum (of which 1 is potentially serious!) you should know about.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of interesting companies, and this list of stocks growth stocks (according to analyst forecasts)

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:INTEG B

Integrum

Researches, develops, and sells various systems for bone-anchored prostheses.

Undervalued with high growth potential.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor