Advertisement

- Sweden

- /

- Medical Equipment

- /

- OM:CEVI

There's Reason For Concern Over CellaVision AB (publ)'s (STO:CEVI) Massive 29% Price Jump

Those holding CellaVision AB (publ) (STO:CEVI) shares would be relieved that the share price has rebounded 29% in the last thirty days, but it needs to keep going to repair the recent damage it has caused to investor portfolios. The bad news is that even after the stocks recovery in the last 30 days, shareholders are still underwater by about 8.4% over the last year.

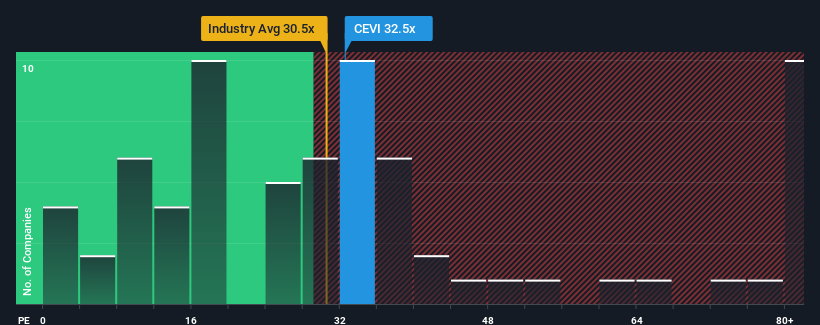

After such a large jump in price, CellaVision may be sending bearish signals at the moment with its price-to-earnings (or "P/E") ratio of 32.5x, since almost half of all companies in Sweden have P/E ratios under 21x and even P/E's lower than 13x are not unusual. However, the P/E might be high for a reason and it requires further investigation to determine if it's justified.

There hasn't been much to differentiate CellaVision's and the market's earnings growth lately. One possibility is that the P/E is high because investors think this modest earnings performance will accelerate. If not, then existing shareholders may be a little nervous about the viability of the share price.

Check out our latest analysis for CellaVision

How Is CellaVision's Growth Trending?

The only time you'd be truly comfortable seeing a P/E as high as CellaVision's is when the company's growth is on track to outshine the market.

If we review the last year of earnings growth, the company posted a worthy increase of 7.7%. The solid recent performance means it was also able to grow EPS by 12% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been respectable for the company.

Looking ahead now, EPS is anticipated to climb by 18% each year during the coming three years according to the four analysts following the company. Meanwhile, the rest of the market is forecast to expand by 20% per year, which is not materially different.

In light of this, it's curious that CellaVision's P/E sits above the majority of other companies. Apparently many investors in the company are more bullish than analysts indicate and aren't willing to let go of their stock right now. These shareholders may be setting themselves up for disappointment if the P/E falls to levels more in line with the growth outlook.

What We Can Learn From CellaVision's P/E?

The large bounce in CellaVision's shares has lifted the company's P/E to a fairly high level. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that CellaVision currently trades on a higher than expected P/E since its forecast growth is only in line with the wider market. Right now we are uncomfortable with the relatively high share price as the predicted future earnings aren't likely to support such positive sentiment for long. Unless these conditions improve, it's challenging to accept these prices as being reasonable.

Many other vital risk factors can be found on the company's balance sheet. Take a look at our free balance sheet analysis for CellaVision with six simple checks on some of these key factors.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:CEVI

CellaVision

Develops and sells instruments, software, and reagents for blood and body fluids analysis in Sweden and internationally.

Very undervalued with flawless balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor