Advertisement

- Sweden

- /

- Medical Equipment

- /

- OM:BOUL

We Think Boule Diagnostics (STO:BOUL) Is Taking Some Risk With Its Debt

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Boule Diagnostics AB (publ) (STO:BOUL) makes use of debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

What Is Boule Diagnostics's Net Debt?

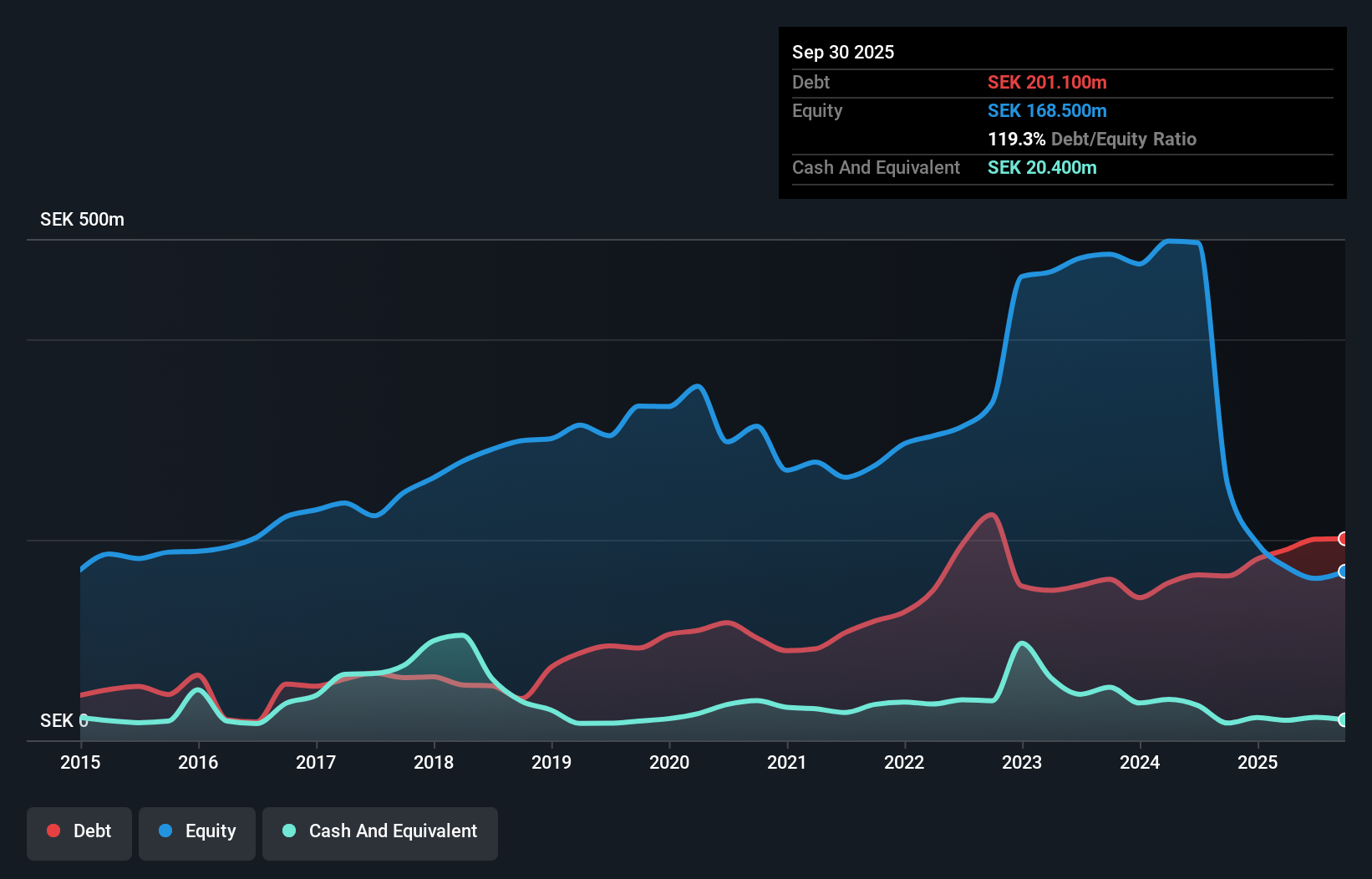

You can click the graphic below for the historical numbers, but it shows that as of September 2025 Boule Diagnostics had kr201.1m of debt, an increase on kr163.9m, over one year. However, it also had kr20.4m in cash, and so its net debt is kr180.7m.

How Healthy Is Boule Diagnostics' Balance Sheet?

The latest balance sheet data shows that Boule Diagnostics had liabilities of kr210.5m due within a year, and liabilities of kr82.2m falling due after that. On the other hand, it had cash of kr20.4m and kr131.1m worth of receivables due within a year. So its liabilities total kr141.2m more than the combination of its cash and short-term receivables.

This is a mountain of leverage relative to its market capitalization of kr208.9m. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

Check out our latest analysis for Boule Diagnostics

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Boule Diagnostics has a low net debt to EBITDA ratio of only 0.54. And its EBIT covers its interest expense a whopping 22.8 times over. So you could argue it is no more threatened by its debt than an elephant is by a mouse. It was also good to see that despite losing money on the EBIT line last year, Boule Diagnostics turned things around in the last 12 months, delivering and EBIT of kr321m. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Boule Diagnostics can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it's worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. Considering the last year, Boule Diagnostics actually recorded a cash outflow, overall. Debt is far more risky for companies with unreliable free cash flow, so shareholders should be hoping that the past expenditure will produce free cash flow in the future.

Our View

Boule Diagnostics's conversion of EBIT to free cash flow and level of total liabilities definitely weigh on it, in our esteem. But its interest cover tells a very different story, and suggests some resilience. It's also worth noting that Boule Diagnostics is in the Medical Equipment industry, which is often considered to be quite defensive. We think that Boule Diagnostics's debt does make it a bit risky, after considering the aforementioned data points together. That's not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 2 warning signs for Boule Diagnostics you should be aware of, and 1 of them is potentially serious.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're here to simplify it.

Discover if Boule Diagnostics might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:BOUL

Boule Diagnostics

Develops, manufactures, and markets instruments and consumable products for blood diagnostics in the United States of America, Asia, Eastern Europe, Latin America, Western Europe, Africa, and the Middle East.

Undervalued with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|10.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|20.3% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.1% undervalued

LI

Community Contributor