Advertisement

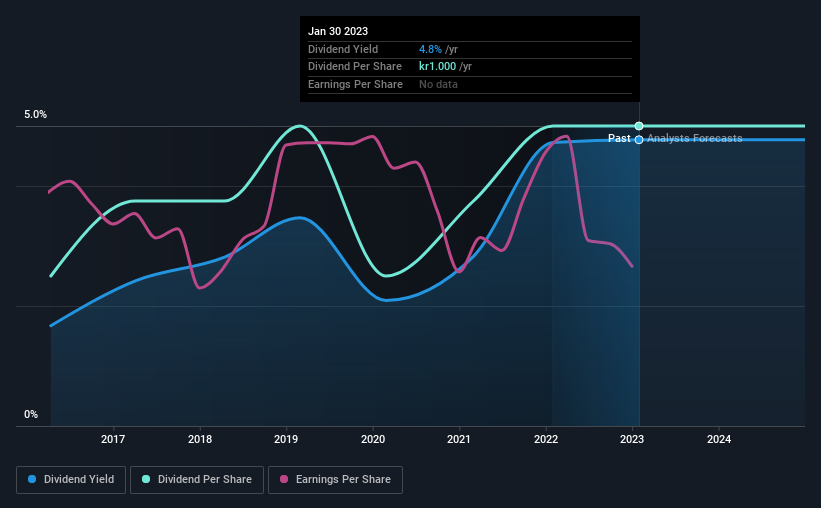

Cloetta AB (publ) (STO:CLA B) has announced that it will pay a dividend of SEK1.00 per share on the 13th of April. Based on this payment, the dividend yield on the company's stock will be 4.8%, which is an attractive boost to shareholder returns.

Check out our latest analysis for Cloetta

Cloetta's Earnings Easily Cover The Distributions

A big dividend yield for a few years doesn't mean much if it can't be sustained. Based on the last payment, the dividend made up 95% of cash flows, but a higher proportion of net income. While the cash payout ratio isn't necessarily a cause for concern, the company is probably focusing more on returning cash to shareholders than growing the business.

Looking forward, earnings per share is forecast to rise by 124.2% over the next year. Under the assumption that the dividend will continue along recent trends, we think the payout ratio could be 49% which would be quite comfortable going to take the dividend forward.

Cloetta's Dividend Has Lacked Consistency

Cloetta has been paying dividends for a while, but the track record isn't stellar. If the company cuts once, it definitely isn't argument against the possibility of it cutting in the future. Since 2016, the dividend has gone from SEK0.50 total annually to SEK1.00. This means that it has been growing its distributions at 10% per annum over that time. It is great to see strong growth in the dividend payments, but cuts are concerning as it may indicate the payout policy is too ambitious.

Cloetta May Find It Hard To Grow The Dividend

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. Earnings per share has been crawling upwards at 2.9% per year. The earnings growth is anaemic, and the company is paying out 104% of its profit. Limited recent earnings growth and a high payout ratio makes it hard for us to envision strong future dividend growth, unless the company should have substantial pricing power or some form of competitive advantage.

Cloetta's Dividend Doesn't Look Sustainable

In summary, while it's good to see that the dividend hasn't been cut, we are a bit cautious about Cloetta's payments, as there could be some issues with sustaining them into the future. The track record isn't great, and the payments are a bit high to be considered sustainable. This company is not in the top tier of income providing stocks.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. For example, we've identified 3 warning signs for Cloetta (1 is potentially serious!) that you should be aware of before investing. Is Cloetta not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:CLA B

Solid track record with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|25.1% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.04% overvalued

LI

Community Contributor