Stock Analysis

- Sweden

- /

- Capital Markets

- /

- OM:EQT

EQT (STO:EQT) Has Announced That It Will Be Increasing Its Dividend To €1.40

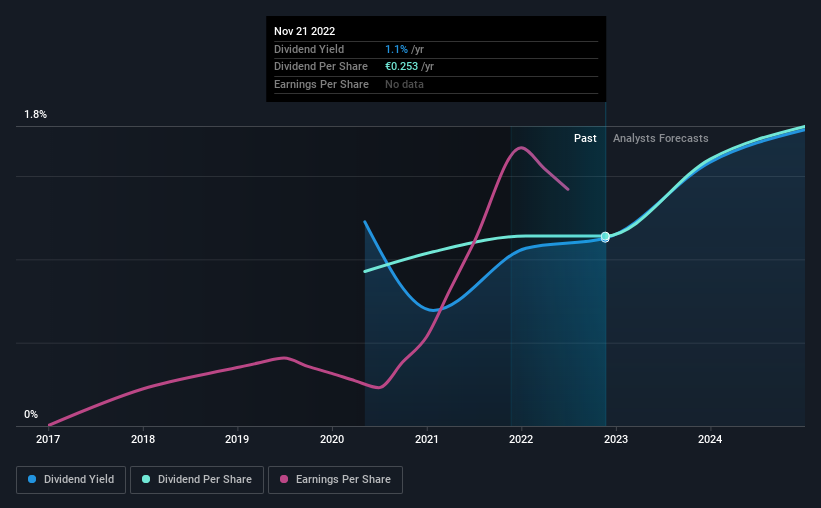

EQT AB (publ) (STO:EQT) will increase its dividend from last year's comparable payment on the 6th of December to €1.40. Even though the dividend went up, the yield is still quite low at only 1.1%.

Check out our latest analysis for EQT

EQT Doesn't Earn Enough To Cover Its Payments

While yield is important, another factor to consider about a company's dividend is whether the current payout levels are feasible. However, prior to this announcement, EQT's dividend was comfortably covered by both cash flow and earnings. This means that most of what the business earns is being used to help it grow.

The next 12 months is set to see EPS grow by 84.4%. However, if the dividend continues along recent trends, it could start putting pressure on the balance sheet with the payout ratio getting very high over the next year.

EQT Doesn't Have A Long Payment History

The dividend hasn't seen any major cuts in the past, but the company has only been paying a dividend for 3 years, which isn't that long in the grand scheme of things. The dividend has gone from an annual total of €0.206 in 2019 to the most recent total annual payment of €0.253. This implies that the company grew its distributions at a yearly rate of about 7.1% over that duration. EQT has been growing its dividend at a decent rate, and the payments have been stable. However, the payment history is very short, so there is no evidence yet that the dividend can be sustained over a full economic cycle.

The Dividend Looks Likely To Grow

Investors could be attracted to the stock based on the quality of its payment history. We are encouraged to see that EQT has grown earnings per share at 268% per year over the past five years. A low payout ratio gives the company a lot of flexibility, and growing earnings also make it very easy for it to grow the dividend.

An additional note is that the company has been raising capital by issuing stock equal to 20% of shares outstanding in the last 12 months. Trying to grow the dividend when issuing new shares reminds us of the ancient Greek tale of Sisyphus - perpetually pushing a boulder uphill. Companies that consistently issue new shares are often suboptimal from a dividend perspective.

EQT Looks Like A Great Dividend Stock

Overall, a dividend increase is always good, and we think that EQT is a strong income stock thanks to its track record and growing earnings. Distributions are quite easily covered by earnings, which are also being converted to cash flows. Taking this all into consideration, this looks like it could be a good dividend opportunity.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. For example, we've picked out 1 warning sign for EQT that investors should know about before committing capital to this stock. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Valuation is complex, but we're helping make it simple.

Find out whether EQT is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:EQT

EQT

A global private equity firm specializing in private capital and real asset segments.

High growth potential with excellent balance sheet.