Advertisement

- Sweden

- /

- Commercial Services

- /

- OM:LOOMIS

Will Loomis' (OM:LOOMIS) Earnings Growth and Buyback Plan Shift Its Diversification Strategy?

Simply Wall St

Reviewed by Sasha Jovanovic

- Loomis AB recently reported its third quarter 2025 results, posting sales of SEK 7.64 billion and net income of SEK 528 million, alongside a new share buyback program of up to SEK 200 million to run through early 2026.

- Alongside higher operating margins and continued acquisition activity, Loomis' decision to repurchase shares highlights ongoing management focus on capital allocation and shareholder returns.

- We will assess how Loomis' improved earnings and share repurchase initiative may influence the outlook for its diversification and margin expansion plans.

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

Loomis Investment Narrative Recap

To be a Loomis shareholder, you need to believe in the company's ability to balance legacy cash handling with the growth of high-security logistics and automation, while navigating persistent headwinds around declining ATM volumes in Europe. The Q3 results and buyback program reinforce management’s focus on capital allocation, but do not meaningfully change the key short-term catalyst of successful diversification, while the fundamental risk remains a sustained downturn in European cash volumes. Among recent announcements, the Q3 share buyback plan, capped at SEK 200 million through early 2026, is closely tied to investor returns and signals confidence in Loomis’ stability as it pursues acquisitions and operational improvements. This initiative, however, does not materially alter the earnings impact from structural shifts in European cash usage, which continues to be closely watched by the market. Yet, against recent earnings strength, investors should remain alert to the risks if Loomis' digital ventures and adjacent markets…

Read the full narrative on Loomis (it's free!)

Loomis' outlook anticipates SEK33.0 billion in revenue and SEK3.1 billion in earnings by 2028. Achieving this would mean a 2.6% annual revenue growth and an increase in earnings of SEK1.4 billion from the current SEK1.7 billion.

Uncover how Loomis' forecasts yield a SEK479.33 fair value, a 25% upside to its current price.

Exploring Other Perspectives

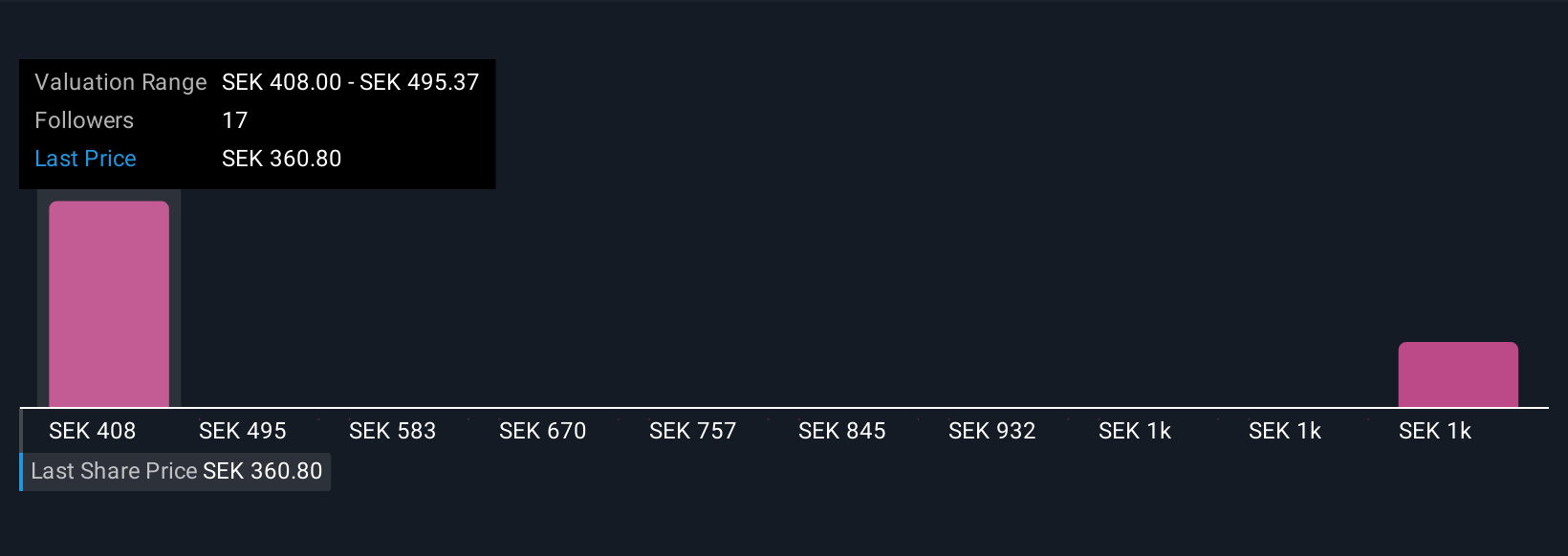

Fair value estimates for Loomis from the Simply Wall St Community range widely from SEK408 to SEK1,283 across five contributors. With market participants split, the company’s ongoing need for rapid, scalable diversification outside cash handling is a key question that could determine future performance.

Explore 5 other fair value estimates on Loomis - why the stock might be worth over 3x more than the current price!

Build Your Own Loomis Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Loomis research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Loomis research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Loomis' overall financial health at a glance.

No Opportunity In Loomis?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 37 companies in the world exploring or producing it. Find the list for free.

- Outshine the giants: these 26 early-stage AI stocks could fund your retirement.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:LOOMIS

Loomis

Provides secure payment solutions in the United States, France, Switzerland, Spain, the United Kingdom, Sweden, and internationally.

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor