Advertisement

- Sweden

- /

- Professional Services

- /

- OM:AFRY

Earnings Miss: Afry AB Missed EPS By 35% And Analysts Are Revising Their Forecasts

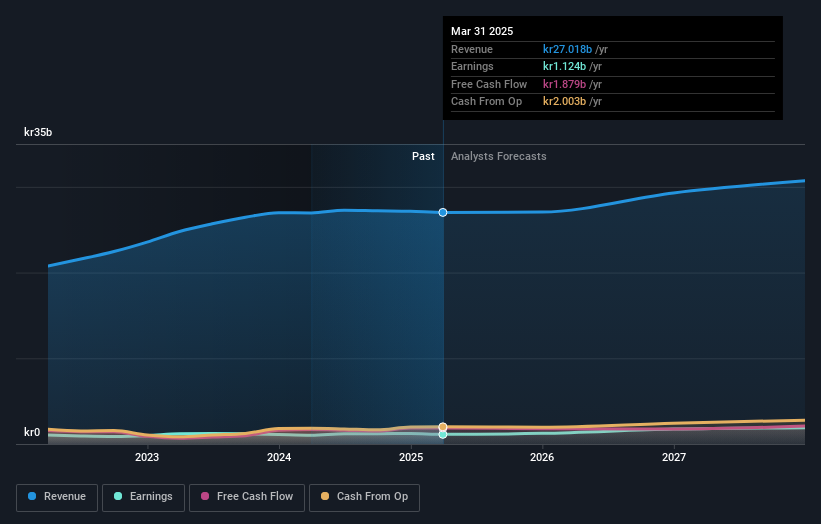

Afry AB (STO:AFRY) just released its latest first-quarter report and things are not looking great. It wasn't a great result overall - while revenue fell marginally short of analyst estimates at kr6.7b, statutory earnings missed forecasts by an incredible 35%, coming in at just kr2.21 per share. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

Taking into account the latest results, Afry's six analysts currently expect revenues in 2025 to be kr27.1b, approximately in line with the last 12 months. Statutory earnings per share are predicted to grow 10% to kr10.96. Before this earnings report, the analysts had been forecasting revenues of kr28.0b and earnings per share (EPS) of kr13.02 in 2025. The analysts seem less optimistic after the recent results, reducing their revenue forecasts and making a substantial drop in earnings per share numbers.

See our latest analysis for Afry

Despite the cuts to forecast earnings, there was no real change to the kr233 price target, showing that the analysts don't think the changes have a meaningful impact on its intrinsic value. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. The most optimistic Afry analyst has a price target of kr265 per share, while the most pessimistic values it at kr200. This is a very narrow spread of estimates, implying either that Afry is an easy company to value, or - more likely - the analysts are relying heavily on some key assumptions.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. It's pretty clear that there is an expectation that Afry's revenue growth will slow down substantially, with revenues to the end of 2025 expected to display 0.2% growth on an annualised basis. This is compared to a historical growth rate of 8.8% over the past five years. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 6.0% per year. So it's pretty clear that, while revenue growth is expected to slow down, the wider industry is also expected to grow faster than Afry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Afry. Unfortunately, they also downgraded their revenue estimates, and our data indicates underperformance compared to the wider industry. Even so, earnings per share are more important to the intrinsic value of the business. The consensus price target held steady at kr233, with the latest estimates not enough to have an impact on their price targets.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. We have estimates - from multiple Afry analysts - going out to 2027, and you can see them free on our platform here.

However, before you get too enthused, we've discovered 1 warning sign for Afry that you should be aware of.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:AFRY

Afry

Provides engineering, design, and advisory services for the infrastructure, industry, and energy sectors in the Nordics, North America, South America, Asia, rest of Europe, and internationally.

Very undervalued with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|31.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|24.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|13.5% overvalued

DA

Community Contributor