Advertisement

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Norditek Group AB (publ) (STO:NOTEK) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Norditek Group's Debt?

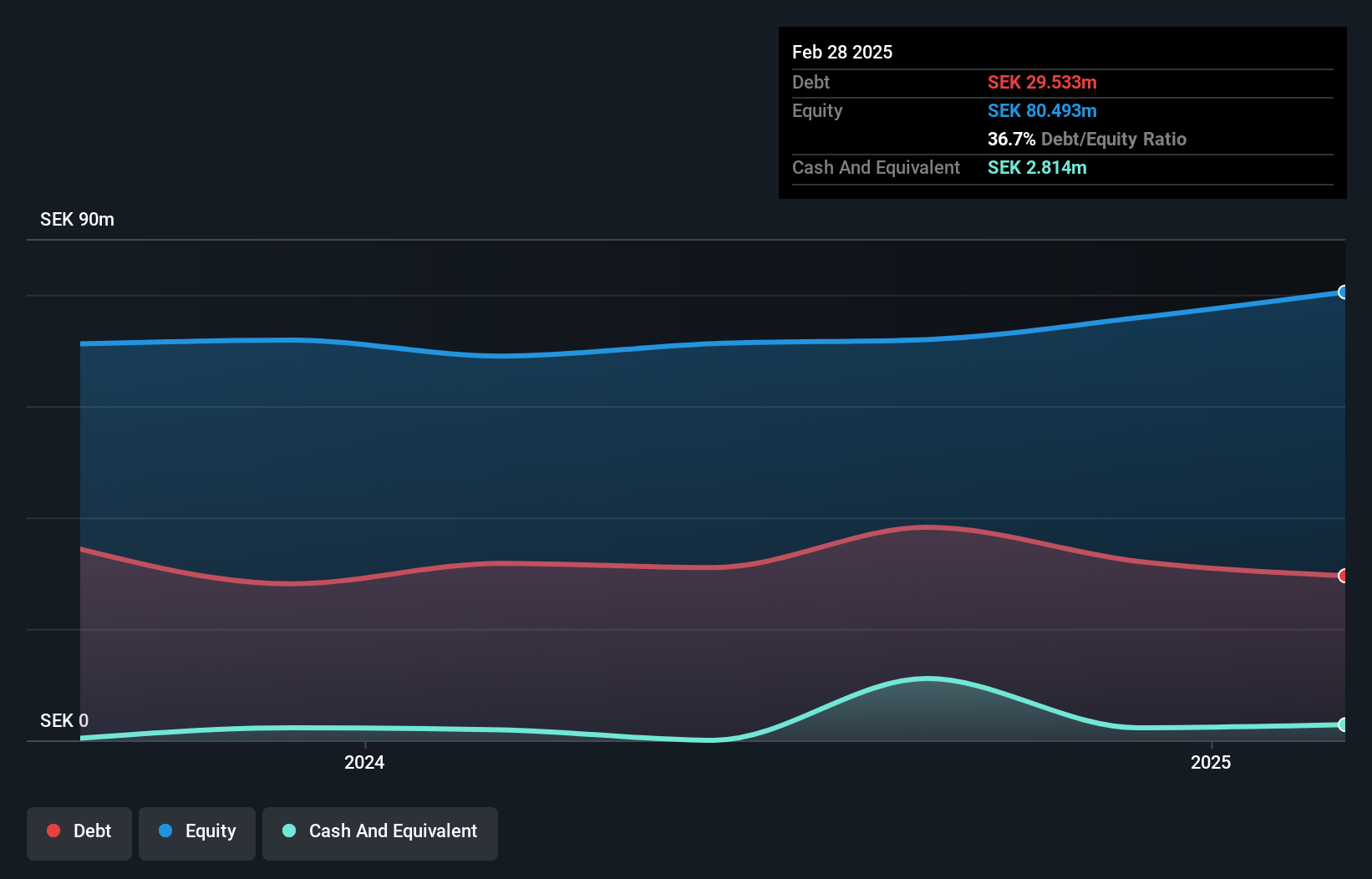

As you can see below, Norditek Group had kr29.5m of debt at February 2025, down from kr31.8m a year prior. However, it does have kr2.81m in cash offsetting this, leading to net debt of about kr26.7m.

How Strong Is Norditek Group's Balance Sheet?

According to the last reported balance sheet, Norditek Group had liabilities of kr25.9m due within 12 months, and liabilities of kr30.9m due beyond 12 months. Offsetting this, it had kr2.81m in cash and kr31.9m in receivables that were due within 12 months. So its liabilities total kr22.1m more than the combination of its cash and short-term receivables.

Given Norditek Group has a market capitalization of kr201.6m, it's hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

View our latest analysis for Norditek Group

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

While Norditek Group's low debt to EBITDA ratio of 1.2 suggests only modest use of debt, the fact that EBIT only covered the interest expense by 6.9 times last year does give us pause. So we'd recommend keeping a close eye on the impact financing costs are having on the business. It was also good to see that despite losing money on the EBIT line last year, Norditek Group turned things around in the last 12 months, delivering and EBIT of kr18m. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Norditek Group's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it's worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. During the last year, Norditek Group generated free cash flow amounting to a very robust 96% of its EBIT, more than we'd expect. That puts it in a very strong position to pay down debt.

Our View

Happily, Norditek Group's impressive conversion of EBIT to free cash flow implies it has the upper hand on its debt. And its net debt to EBITDA is good too. Taking all this data into account, it seems to us that Norditek Group takes a pretty sensible approach to debt. That means they are taking on a bit more risk, in the hope of boosting shareholder returns. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. We've identified 2 warning signs with Norditek Group , and understanding them should be part of your investment process.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're here to simplify it.

Discover if Norditek Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:NOTEK

Norditek Group

Develops, sells, leases, or rents out crushers, sorting plants, and self-developed machines to recycle and convert materials into salable products in Sweden.

Excellent balance sheet and good value.

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.1% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.2% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.2% undervalued

MA

Community Contributor