Advertisement

Health Check: How Prudently Does Ecoclime Group (STO:ECC B) Use Debt?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Ecoclime Group AB (publ) (STO:ECC B) does carry debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Ecoclime Group

What Is Ecoclime Group's Net Debt?

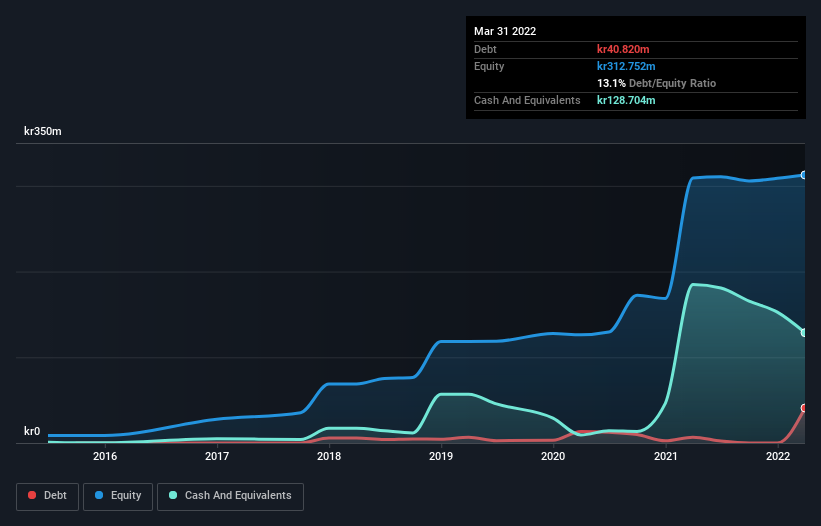

The image below, which you can click on for greater detail, shows that at March 2022 Ecoclime Group had debt of kr40.8m, up from kr6.79m in one year. But it also has kr128.7m in cash to offset that, meaning it has kr87.9m net cash.

How Healthy Is Ecoclime Group's Balance Sheet?

The latest balance sheet data shows that Ecoclime Group had liabilities of kr56.1m due within a year, and liabilities of kr40.8m falling due after that. Offsetting this, it had kr128.7m in cash and kr41.9m in receivables that were due within 12 months. So it actually has kr73.7m more liquid assets than total liabilities.

This surplus suggests that Ecoclime Group has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Simply put, the fact that Ecoclime Group has more cash than debt is arguably a good indication that it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Ecoclime Group can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

In the last year Ecoclime Group wasn't profitable at an EBIT level, but managed to grow its revenue by 20%, to kr184m. Shareholders probably have their fingers crossed that it can grow its way to profits.

So How Risky Is Ecoclime Group?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And in the last year Ecoclime Group had an earnings before interest and tax (EBIT) loss, truth be told. And over the same period it saw negative free cash outflow of kr40m and booked a kr16m accounting loss. With only kr87.9m on the balance sheet, it would appear that its going to need to raise capital again soon. Ecoclime Group's revenue growth shone bright over the last year, so it may well be in a position to turn a profit in due course. Pre-profit companies are often risky, but they can also offer great rewards. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For example - Ecoclime Group has 2 warning signs we think you should be aware of.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Valuation is complex, but we're here to simplify it.

Discover if Ecoclime Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NGM:ECC B

Ecoclime Group

Provides solutions for extraction, recycling, storage, and distribution of thermal energy in properties in Sweden.

Flawless balance sheet with low risk.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor