Advertisement

- Sweden

- /

- Aerospace & Defense

- /

- OM:AAC

Further Upside For AAC Clyde Space AB (publ) (STO:AAC) Shares Could Introduce Price Risks After 28% Bounce

AAC Clyde Space AB (publ) (STO:AAC) shares have continued their recent momentum with a 28% gain in the last month alone. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 39% in the last twelve months.

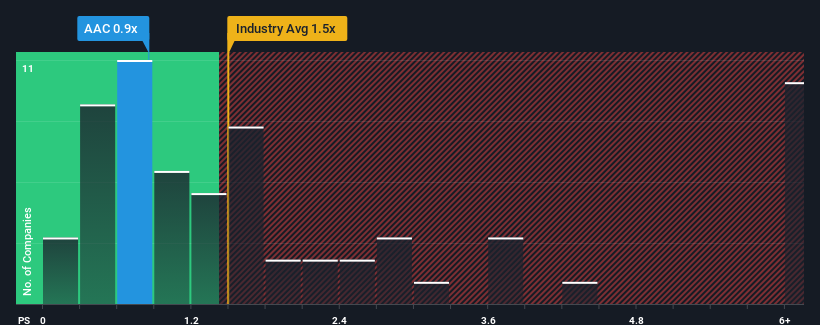

In spite of the firm bounce in price, AAC Clyde Space may still be sending buy signals at present with its price-to-sales (or "P/S") ratio of 0.9x, considering almost half of all companies in the Aerospace & Defense industry in Sweden have P/S ratios greater than 2.8x and even P/S higher than 8x aren't out of the ordinary. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/S.

See our latest analysis for AAC Clyde Space

What Does AAC Clyde Space's Recent Performance Look Like?

There hasn't been much to differentiate AAC Clyde Space's and the industry's revenue growth lately. Perhaps the market is expecting future revenue performance to dive, which has kept the P/S suppressed. If you like the company, you'd be hoping this isn't the case so that you could pick up some stock while it's out of favour.

Want the full picture on analyst estimates for the company? Then our free report on AAC Clyde Space will help you uncover what's on the horizon.How Is AAC Clyde Space's Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as low as AAC Clyde Space's is when the company's growth is on track to lag the industry.

If we review the last year of revenue growth, the company posted a terrific increase of 34%. Pleasingly, revenue has also lifted 199% in aggregate from three years ago, thanks to the last 12 months of growth. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Shifting to the future, estimates from the lone analyst covering the company suggest revenue should grow by 43% over the next year. With the industry only predicted to deliver 14%, the company is positioned for a stronger revenue result.

In light of this, it's peculiar that AAC Clyde Space's P/S sits below the majority of other companies. Apparently some shareholders are doubtful of the forecasts and have been accepting significantly lower selling prices.

The Bottom Line On AAC Clyde Space's P/S

Despite AAC Clyde Space's share price climbing recently, its P/S still lags most other companies. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

A look at AAC Clyde Space's revenues reveals that, despite glowing future growth forecasts, its P/S is much lower than we'd expect. When we see strong growth forecasts like this, we can only assume potential risks are what might be placing significant pressure on the P/S ratio. While the possibility of the share price plunging seems unlikely due to the high growth forecasted for the company, the market does appear to have some hesitation.

Before you take the next step, you should know about the 5 warning signs for AAC Clyde Space (1 is significant!) that we have uncovered.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:AAC

AAC Clyde Space

Provides small satellite technologies and services in Sweden, the United Kingdom, rest of Europe, the United States, Asia, and internationally.

High growth potential and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor