Advertisement

- Saudi Arabia

- /

- Basic Materials

- /

- SASE:3002

Najran Cement (TADAWUL:3002) Has Announced A Dividend Of ر.س0.75

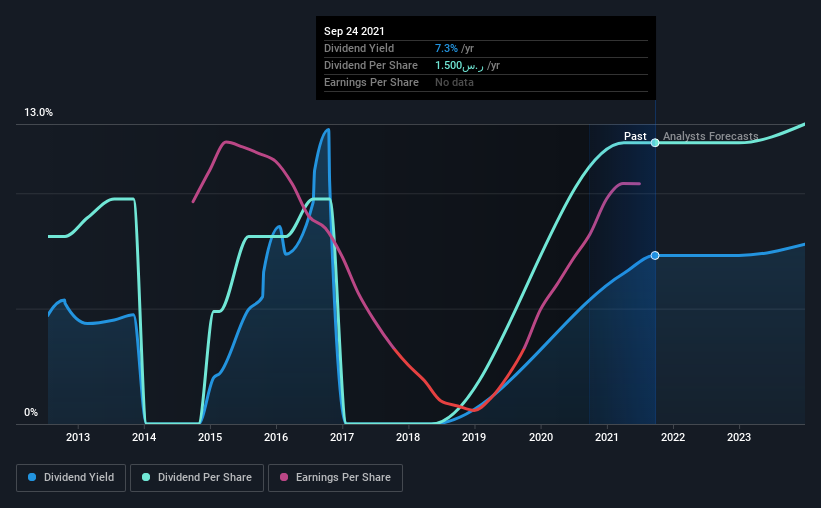

Najran Cement Company (TADAWUL:3002) will pay a dividend of ر.س0.75 on the 1st of January. Based on this payment, the dividend yield on the company's stock will be 7.3%, which is an attractive boost to shareholder returns.

Check out our latest analysis for Najran Cement

Najran Cement Doesn't Earn Enough To Cover Its Payments

Impressive dividend yields are good, but this doesn't matter much if the payments can't be sustained. Prior to this announcement, the company was paying out 113% of what it was earning and 75% of cash flows. While the cash payout ratio isn't necessarily a cause for concern, the company is probably focusing more on returning cash to shareholders than growing the business.

Looking forward, earnings per share is forecast to fall by 3.4% over the next year. If the dividend continues along the path it has been on recently, the payout ratio in 12 months could be 124%, which is definitely a bit high to be sustainable going forward.

Najran Cement's Dividend Has Lacked Consistency

Najran Cement has been paying dividends for a while, but the track record isn't stellar. This makes us cautious about the consistency of the dividend over a full economic cycle. Since 2012, the dividend has gone from ر.س1.00 to ر.س1.50. This works out to be a compound annual growth rate (CAGR) of approximately 4.6% a year over that time. Modest growth in the dividend is good to see, but we think this is offset by historical cuts to the payments. It is hard to live on a dividend income if the company's earnings are not consistent.

Najran Cement May Find It Hard To Grow The Dividend

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. However, Najran Cement has only grown its earnings per share at 4.5% per annum over the past five years. The earnings growth is anaemic, and the company is paying out 113% of its profit. As they say in finance, 'past performance is not indicative of future performance', but we are not confident a company with limited earnings growth and a high payout ratio will be a star dividend-payer over the next decade.

The Dividend Could Prove To Be Unreliable

In summary, while it's good to see that the dividend hasn't been cut, we are a bit cautious about Najran Cement's payments, as there could be some issues with sustaining them into the future. The payments are bit high to be considered sustainable, and the track record isn't the best. We would probably look elsewhere for an income investment.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Taking the debate a bit further, we've identified 1 warning sign for Najran Cement that investors need to be conscious of moving forward. Looking for more high-yielding dividend ideas? Try our curated list of strong dividend payers.

If you're looking for stocks to buy, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Najran Cement might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SASE:3002

Najran Cement

Engages in manufacture and sale of cement products in the Kingdom of Saudi Arabia.

Flawless balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$268.43|27.9% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|43.8% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$189.00|41.0% undervalued

AG

Community Contributor