Advertisement

- Saudi Arabia

- /

- Insurance

- /

- SASE:8060

Walaa Cooperative Insurance Company (TADAWUL:8060) Stock's Been Sliding But Fundamentals Look Decent: Will The Market Correct The Share Price In The Future?

It is hard to get excited after looking at Walaa Cooperative Insurance's (TADAWUL:8060) recent performance, when its stock has declined 17% over the past month. However, stock prices are usually driven by a company’s financials over the long term, which in this case look pretty respectable. Particularly, we will be paying attention to Walaa Cooperative Insurance's ROE today.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. Put another way, it reveals the company's success at turning shareholder investments into profits.

View our latest analysis for Walaa Cooperative Insurance

How To Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Walaa Cooperative Insurance is:

9.6% = ر.س130m ÷ ر.س1.4b (Based on the trailing twelve months to September 2024).

The 'return' is the amount earned after tax over the last twelve months. Another way to think of that is that for every SAR1 worth of equity, the company was able to earn SAR0.10 in profit.

What Has ROE Got To Do With Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

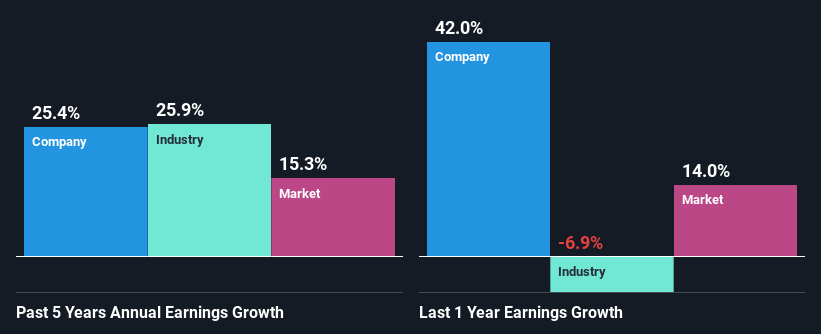

A Side By Side comparison of Walaa Cooperative Insurance's Earnings Growth And 9.6% ROE

As you can see, Walaa Cooperative Insurance's ROE looks pretty weak. Further, we noted that the company's ROE is similar to the industry average of 9.6%. However, the exceptional 25% net income growth seen by Walaa Cooperative Insurance over the past five years is pretty remarkable. Given the low ROE, it is likely that there could be some other reasons behind this growth as well. For instance, the company has a low payout ratio or is being managed efficiently.

Next, on comparing Walaa Cooperative Insurance's net income growth with the industry, we found that the company's reported growth is similar to the industry average growth rate of 26% over the last few years.

Earnings growth is an important metric to consider when valuing a stock. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. Doing so will help them establish if the stock's future looks promising or ominous. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if Walaa Cooperative Insurance is trading on a high P/E or a low P/E, relative to its industry.

Is Walaa Cooperative Insurance Efficiently Re-investing Its Profits?

Walaa Cooperative Insurance doesn't pay any regular dividends to its shareholders, meaning that the company has been reinvesting all of its profits into the business. This is likely what's driving the high earnings growth number discussed above.

Summary

In total, it does look like Walaa Cooperative Insurance has some positive aspects to its business. With a high rate of reinvestment, albeit at a low ROE, the company has managed to see a considerable growth in its earnings. While we won't completely dismiss the company, what we would do, is try to ascertain how risky the business is to make a more informed decision around the company. Our risks dashboard would have the 2 risks we have identified for Walaa Cooperative Insurance.

Valuation is complex, but we're here to simplify it.

Discover if Walaa Cooperative Insurance might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SASE:8060

Walaa Cooperative Insurance

Provides cooperative insurance and reinsurance products and services in the Kingdom of Saudi Arabia.

High growth potential with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor