Advertisement

- Russia

- /

- Renewable Energy

- /

- MISX:OGKB

Is Second Generating Company of the Electric Power Wholesale Market (MCX:OGKB) A Risky Investment?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Public Joint-Stock Company "Second Generating Company of the Electric Power Wholesale Market" (MCX:OGKB) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Second Generating Company of the Electric Power Wholesale Market

How Much Debt Does Second Generating Company of the Electric Power Wholesale Market Carry?

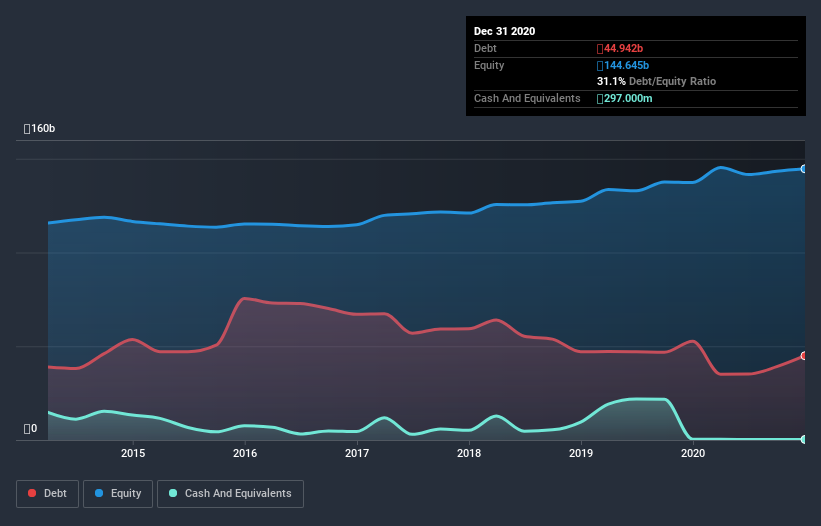

As you can see below, Second Generating Company of the Electric Power Wholesale Market had ₽44.9b of debt at December 2020, down from ₽52.6b a year prior. And it doesn't have much cash, so its net debt is about the same.

How Healthy Is Second Generating Company of the Electric Power Wholesale Market's Balance Sheet?

The latest balance sheet data shows that Second Generating Company of the Electric Power Wholesale Market had liabilities of ₽18.4b due within a year, and liabilities of ₽61.4b falling due after that. Offsetting this, it had ₽297.0m in cash and ₽25.8b in receivables that were due within 12 months. So its liabilities total ₽53.7b more than the combination of its cash and short-term receivables.

This is a mountain of leverage relative to its market capitalization of ₽87.9b. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

With net debt sitting at just 1.5 times EBITDA, Second Generating Company of the Electric Power Wholesale Market is arguably pretty conservatively geared. And it boasts interest cover of 8.8 times, which is more than adequate. It is just as well that Second Generating Company of the Electric Power Wholesale Market's load is not too heavy, because its EBIT was down 21% over the last year. When it comes to paying off debt, falling earnings are no more useful than sugary sodas are for your health. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Second Generating Company of the Electric Power Wholesale Market's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. During the last three years, Second Generating Company of the Electric Power Wholesale Market produced sturdy free cash flow equating to 76% of its EBIT, about what we'd expect. This cold hard cash means it can reduce its debt when it wants to.

Our View

Second Generating Company of the Electric Power Wholesale Market's struggle to grow its EBIT had us second guessing its balance sheet strength, but the other data-points we considered were relatively redeeming. For example its conversion of EBIT to free cash flow was refreshing. Looking at all the angles mentioned above, it does seem to us that Second Generating Company of the Electric Power Wholesale Market is a somewhat risky investment as a result of its debt. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. These risks can be hard to spot. Every company has them, and we've spotted 2 warning signs for Second Generating Company of the Electric Power Wholesale Market (of which 1 makes us a bit uncomfortable!) you should know about.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

If you decide to trade Second Generating Company of the Electric Power Wholesale Market, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About MISX:OGKB

Second Generating Company of the Electric Power Wholesale Market

Public Joint-Stock Company "Second Generating Company of the Electric Power Wholesale Market", together with its subsidiaries, generates and sells electricity and thermal energy in Russia.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor