Advertisement

- Romania

- /

- Food and Staples Retail

- /

- BVB:OMAL

Why We're Not Concerned Yet About Comaliment SA (Resita)'s (BVB:OMAL) 35% Share Price Plunge

Comaliment SA (Resita) (BVB:OMAL) shareholders that were waiting for something to happen have been dealt a blow with a 35% share price drop in the last month. To make matters worse, the recent drop has wiped out a year's worth of gains with the share price now back where it started a year ago.

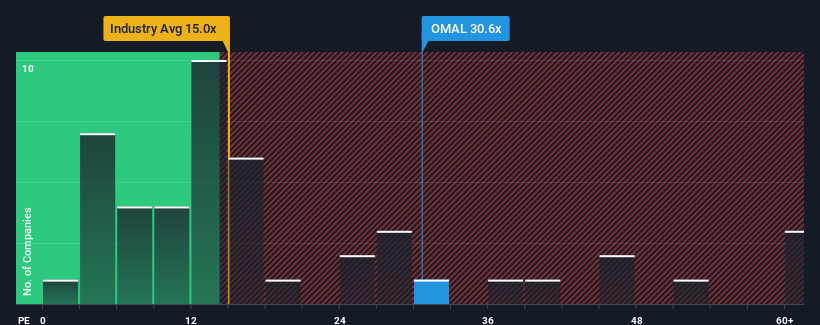

Even after such a large drop in price, given close to half the companies in Romania have price-to-earnings ratios (or "P/E's") below 15x, you may still consider Comaliment SA (Resita) as a stock to avoid entirely with its 30.6x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

For example, consider that Comaliment SA (Resita)'s financial performance has been poor lately as its earnings have been in decline. It might be that many expect the company to still outplay most other companies over the coming period, which has kept the P/E from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

View our latest analysis for Comaliment SA (Resita)

What Are Growth Metrics Telling Us About The High P/E?

In order to justify its P/E ratio, Comaliment SA (Resita) would need to produce outstanding growth well in excess of the market.

Retrospectively, the last year delivered a frustrating 8.8% decrease to the company's bottom line. Still, the latest three year period has seen an excellent 1,537% overall rise in EPS, in spite of its unsatisfying short-term performance. Although it's been a bumpy ride, it's still fair to say the earnings growth recently has been more than adequate for the company.

Weighing the recent medium-term upward earnings trajectory against the broader market's one-year forecast for contraction of 5.5% shows it's a great look while it lasts.

In light of this, it's understandable that Comaliment SA (Resita)'s P/E sits above the majority of other companies. Presumably shareholders aren't keen to offload something they believe will continue to outmanoeuvre the bourse. However, its current earnings trajectory will be very difficult to maintain against the headwinds other companies are facing at the moment.

The Bottom Line On Comaliment SA (Resita)'s P/E

A significant share price dive has done very little to deflate Comaliment SA (Resita)'s very lofty P/E. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that Comaliment SA (Resita) maintains its high P/E on the strength of its recentthree-year growth beating forecasts for a struggling market, as expected. Right now shareholders are comfortable with the P/E as they are quite confident earnings aren't under threat. Our only concern is whether its earnings trajectory can keep outperforming under these tough market conditions. Otherwise, it's hard to see the share price falling strongly in the near future if its earnings performance persists.

We don't want to rain on the parade too much, but we did also find 3 warning signs for Comaliment SA (Resita) that you need to be mindful of.

Of course, you might also be able to find a better stock than Comaliment SA (Resita). So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BVB:OMAL

Flawless balance sheet with solid track record.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor