Advertisement

- Portugal

- /

- Hospitality

- /

- ENXTLS:IBS

Bearish: Analysts Just Cut Their Ibersol, S.G.P.S., S.A. (ELI:IBS) Revenue and EPS estimates

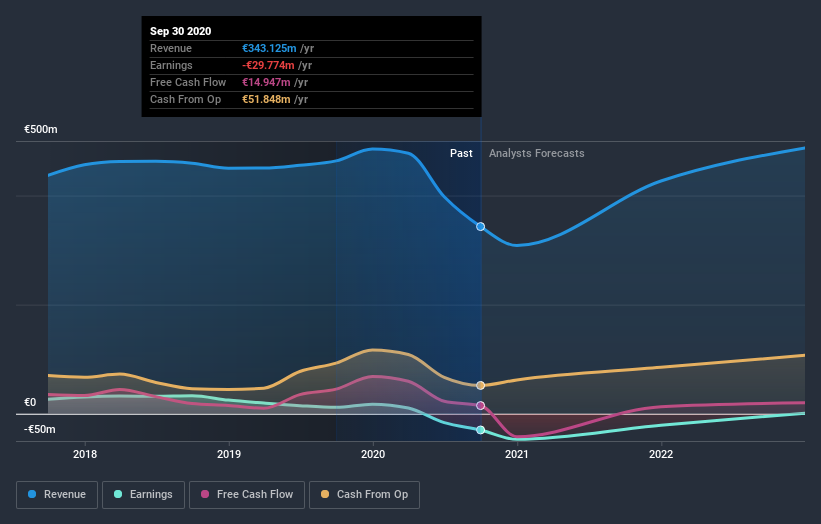

One thing we could say about the analysts on Ibersol, S.G.P.S., S.A. (ELI:IBS) - they aren't optimistic, having just made a major negative revision to their near-term (statutory) forecasts for the organization. Both revenue and earnings per share (EPS) forecasts went under the knife, suggesting analysts have soured majorly on the business. Shares are up 4.1% to €5.10 in the past week. We'd be curious to see if the downgrade is enough to reverse investor sentiment on the business.

After the downgrade, the consensus from Ibersol S.G.P.S' dual analysts is for revenues of €308m in 2020, which would reflect a considerable 10% decline in sales compared to the last year of performance. Per-share losses are expected to explode, reaching €1.69 per share. Yet prior to the latest estimates, the analysts had been forecasting revenues of €364m and losses of €1.36 per share in 2020. Ergo, there's been a clear change in sentiment, with the analysts administering a notable cut to this year's revenue estimates, while at the same time increasing their loss per share forecasts.

Check out our latest analysis for Ibersol S.G.P.S

There was no major change to the consensus price target of €6.55, signalling that the business is performing roughly in line with expectations, despite lower earnings per share forecasts. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. Currently, the most bullish analyst values Ibersol S.G.P.S at €6.60 per share, while the most bearish prices it at €6.50. The narrow spread of estimates could suggest that the business' future is relatively easy to value, or that the analysts have a clear view on its prospects.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. These estimates imply that sales are expected to slow, with a forecast revenue decline of 10%, a significant reduction from annual growth of 14% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 15% next year. It's pretty clear that Ibersol S.G.P.S' revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most important thing to note from this downgrade is that the consensus increased its forecast losses this year, suggesting all may not be well at Ibersol S.G.P.S. Unfortunately analysts also downgraded their revenue estimates, and industry data suggests that Ibersol S.G.P.S' revenues are expected to grow slower than the wider market. The lack of change in the price target is puzzling in light of the downgrade but, with a serious decline expected this year, we wouldn't be surprised if investors were a bit wary of Ibersol S.G.P.S.

Worse, Ibersol S.G.P.S is labouring under a substantial debt burden, which - if today's forecasts prove accurate - the forecast downgrade could potentially exacerbate. To see more of our financial analysis, you can click through to our free platform to learn more about its balance sheet and specific concerns we've identified.

We also provide an overview of the Ibersol S.G.P.S Board and CEO remuneration and length of tenure at the company, and whether insiders have been buying the stock, here.

If you’re looking to trade Ibersol S.G.P.S, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ENXTLS:IBS

Ibersol S.G.P.S

Through its subsidiaries, operates a network of restaurants in Portugal, Spain, and Angola.

Average dividend payer and fair value.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor