Mota-Engil SGPS (ENXTLS:EGL) just made a move that is catching the eye of investors interested in the future of smart cities and clean energy. The company’s ATIV division has entered into a major partnership with Wirtek A/S to deliver an advanced, real-time energy data management system for municipalities. While the immediate impact might not grab headlines on earnings day, the strategic positioning here is clear: Mota-Engil is aligning itself with trends in sustainable infrastructure and digital transformation.

Over the past year, the company’s stock has quietly staged a transformation of its own. After some short-term ups and downs, momentum has built steadily, with shares up a remarkable 118% over the past year and surging almost 80% from the start of the year. This performance stands out especially given the continued push into new areas of energy and urban development.

With this collaboration fueling optimism and the stock riding a wave of strong momentum, the question is whether the market has fully priced in these growth prospects or if there is still an opportunity for investors to buy in before the next phase.

Advertisement

Price-to-Earnings of 12.2x: Is it justified?

Based on its price-to-earnings (P/E) multiple, EGL appears to be undervalued compared to the broader European construction industry. The stock trades at a lower earnings multiple, which signals the market may not be fully reflecting its underlying profit generation.

The P/E ratio measures how much investors are willing to pay for each euro of earnings. In construction and capital goods, it is a key metric used to evaluate companies with steady, predictable earnings streams. A lower P/E can indicate either overlooked value or anticipated challenges ahead, depending on profit trends and outlook.

For EGL, the current figure of 12.2x sits well below the industry average of 14.9x and its peer average of 13.8x. This suggests the market may be underestimating the sustainability of its recent earnings growth and future potential.

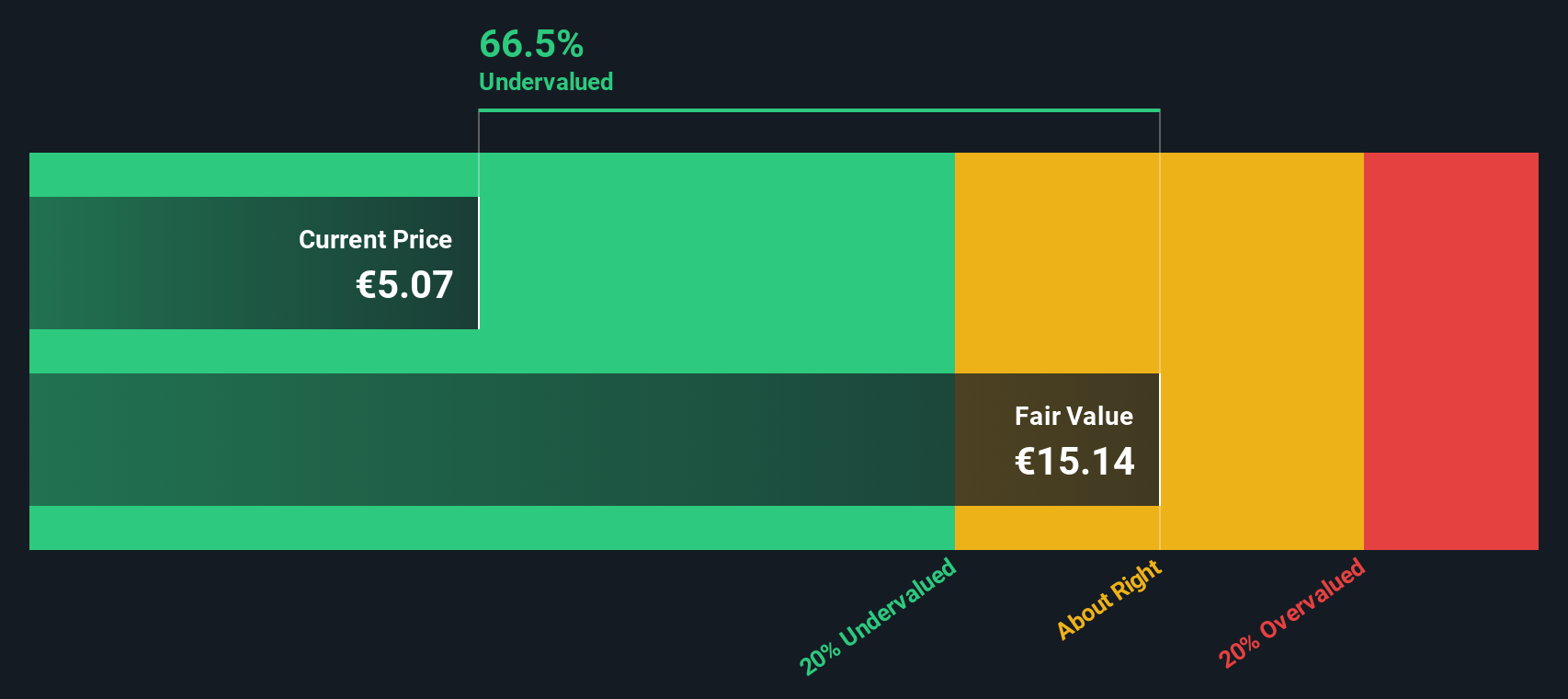

Looking at EGL through the lens of our DCF model, the stock also appears to be trading well below its intrinsic value. This method supports the earlier suggestion of undervaluation; however, does it capture all the risks?

If you see the story differently or want to dive deeper into the numbers yourself, you can build your own view in just a few minutes. Do it your way.

A great starting point for your Mota-Engil SGPS research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Don’t let your next great stock slip by. Smart investors are using the Simply Wall St Screener to spot fresh opportunities beyond the obvious choices.

Unlock growth by tracking potential market leaders in artificial intelligence with our selection of AI penny stocks, which are making big moves in the sector.

Capture stable income streams by checking out dividend stocks with yields > 3%. This features high-yield picks for steady returns.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks