Advertisement

Readers hoping to buy Ifirma SA (WSE:IFI) for its dividend will need to make their move shortly, as the stock is about to trade ex-dividend. Investors can purchase shares before the 8th of December in order to be eligible for this dividend, which will be paid on the 16th of December.

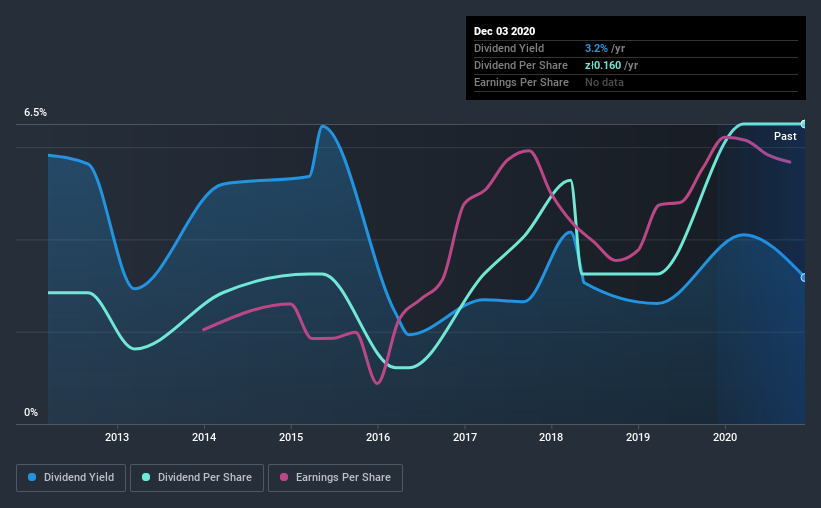

Ifirma's next dividend payment will be zł0.04 per share. Last year, in total, the company distributed zł0.16 to shareholders. Looking at the last 12 months of distributions, Ifirma has a trailing yield of approximately 3.2% on its current stock price of PLN5.04. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. So we need to investigate whether Ifirma can afford its dividend, and if the dividend could grow.

See our latest analysis for Ifirma

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. Ifirma is paying out an acceptable 52% of its profit, a common payout level among most companies. Yet cash flow is typically more important than profit for assessing dividend sustainability, so we should always check if the company generated enough cash to afford its dividend. Fortunately, it paid out only 43% of its free cash flow in the past year.

It's encouraging to see that the dividend is covered by both profit and cash flow. This generally suggests the dividend is sustainable, as long as earnings don't drop precipitously.

Click here to see how much of its profit Ifirma paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Businesses with strong growth prospects usually make the best dividend payers, because it's easier to grow dividends when earnings per share are improving. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. Fortunately for readers, Ifirma's earnings per share have been growing at 17% a year for the past five years. Ifirma is paying out a bit over half its earnings, which suggests the company is striking a balance between reinvesting in growth, and paying dividends. This is a reasonable combination that could hint at some further dividend increases in the future.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. In the past nine years, Ifirma has increased its dividend at approximately 9.6% a year on average. It's encouraging to see the company lifting dividends while earnings are growing, suggesting at least some corporate interest in rewarding shareholders.

To Sum It Up

Is Ifirma worth buying for its dividend? We like Ifirma's growing earnings per share and the fact that - while its payout ratio is around average - it paid out a lower percentage of its cash flow. There's a lot to like about Ifirma, and we would prioritise taking a closer look at it.

So while Ifirma looks good from a dividend perspective, it's always worthwhile being up to date with the risks involved in this stock. For instance, we've identified 2 warning signs for Ifirma (1 doesn't sit too well with us) you should be aware of.

We wouldn't recommend just buying the first dividend stock you see, though. Here's a list of interesting dividend stocks with a greater than 2% yield and an upcoming dividend.

If you’re looking to trade Ifirma, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About WSE:IFI

Ifirma

IFirma SA provides accounting services. The company operates a website, ifirma.pl, which offers services and tools for tax settlements and supporting business activities.

Outstanding track record with flawless balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor