- Sweden

- /

- Hospitality

- /

- OM:BETS B

Exploring December 2024's Undiscovered Gems on None Exchange

Reviewed by Simply Wall St

As global markets continue to hit record highs, small-cap stocks are finally joining their larger peers in this upward trajectory, with the Russell 2000 Index recently reaching an intraday high. Despite geopolitical tensions and tariff uncertainties, robust consumer spending and strong personal income growth have helped sustain market momentum. In such a dynamic environment, identifying potential "undiscovered gems" involves looking for companies that demonstrate resilience and adaptability amidst economic shifts—qualities that could position them well for future growth.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| China Leon Inspection Holding | 8.55% | 21.36% | 22.77% | ★★★★★★ |

| Al-Enma'a Real Estate Company K.S.C.P | 16.88% | -13.58% | 13.65% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Arab Banking Corporation (B.S.C.) | 213.15% | 18.58% | 29.63% | ★★★★☆☆ |

| National Investments Company K.S.C.P | 26.01% | 3.66% | 4.99% | ★★★★☆☆ |

| Al-Ahleia Insurance CompanyK.P | 8.09% | 10.04% | 16.85% | ★★★★☆☆ |

| Wilson | 64.79% | 30.09% | 68.29% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Al-Deera Holding Company K.P.S.C | 6.11% | 51.44% | 59.77% | ★★★★☆☆ |

Let's review some notable picks from our screened stocks.

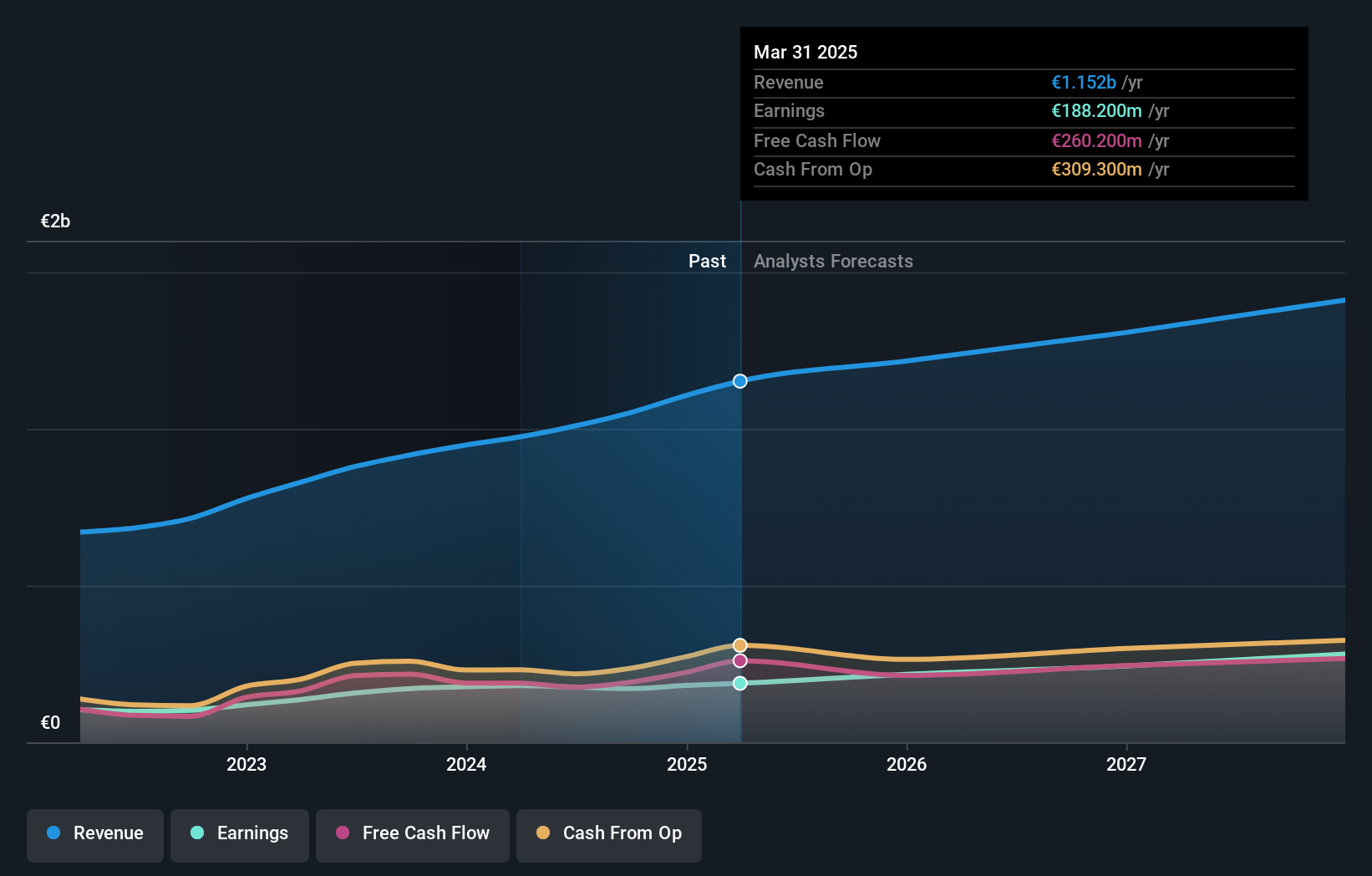

Betsson (OM:BETS B)

Simply Wall St Value Rating: ★★★★★★

Overview: Betsson AB (publ) operates as an online gaming company through its subsidiaries, focusing on markets in the Nordic countries, Latin America, Western Europe, Central and Eastern Europe, Central Asia, and globally; it has a market cap of approximately SEK20.19 billion.

Operations: The company generates revenue primarily from its Casinos & Resorts segment, which amounts to €1.05 billion.

Betsson, a notable player in the market, is trading at a significant discount of 68.8% below its estimated fair value. Despite facing stagnant earnings growth over the past year, it continues to demonstrate high-quality earnings and positive free cash flow. Its debt management has been prudent, with a reduction in the debt-to-equity ratio from 29.7% to 26.9% over five years and interest payments well-covered by EBIT at 13.8 times coverage. Recent financial maneuvers include redeeming existing bonds and issuing new ones worth SEK 100 million, reflecting active capital management strategies in place for future growth prospects.

- Navigate through the intricacies of Betsson with our comprehensive health report here.

Gain insights into Betsson's historical performance by reviewing our past performance report.

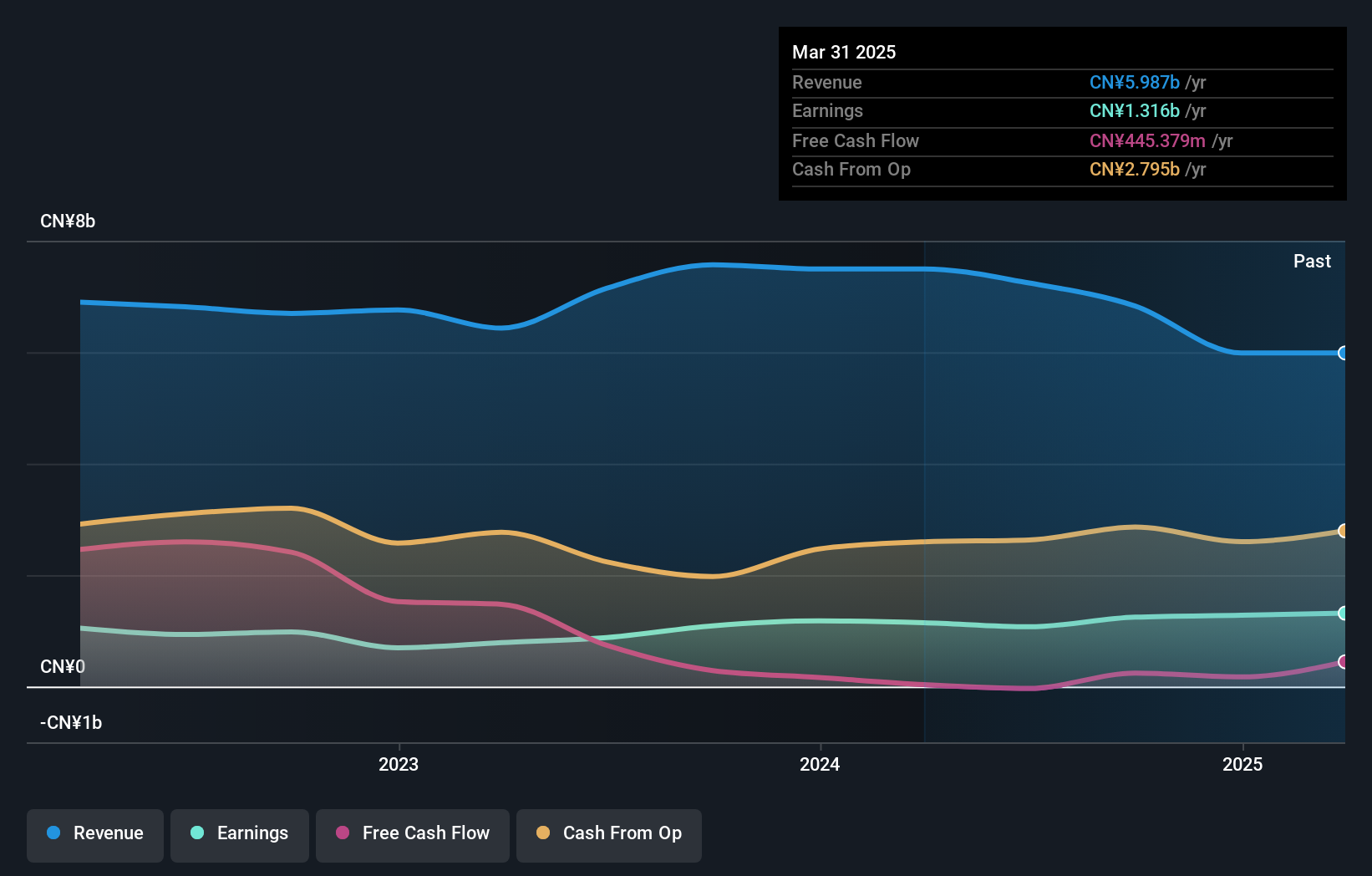

Jiangxi Ganyue ExpresswayLTD (SHSE:600269)

Simply Wall St Value Rating: ★★★★★★

Overview: Jiangxi Ganyue Expressway Co., Ltd., along with its subsidiaries, operates and manages expressways in China, with a market capitalization of CN¥12.68 billion.

Operations: The primary revenue for Jiangxi Ganyue Expressway Co., Ltd. is derived from operating and managing expressways in China. The company focuses on optimizing its cost structure to improve financial performance, with particular attention to controlling operational expenses. An interesting trend observed is the fluctuation in net profit margin over recent periods, reflecting changes in both revenue streams and cost management strategies.

Jiangxi Ganyue Expressway's recent performance highlights its potential as an intriguing investment opportunity. The company reported a net income of CNY 1.15 billion for the first nine months of 2024, up from CNY 1.08 billion the previous year, despite sales dipping to CNY 4.56 billion from CNY 5.22 billion. With earnings per share rising to CNY 0.49 from last year's CNY 0.46, it reflects solid profitability amidst challenges in revenue generation. Its debt management appears commendable as the net debt-to-equity ratio improved significantly over five years, dropping from 86% to a more comfortable level of around 47%.

Asseco Business Solutions (WSE:ABS)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Asseco Business Solutions S.A. designs and develops enterprise software solutions in Poland and internationally, with a market cap of PLN1.79 billion.

Operations: Asseco Business Solutions generates revenue primarily from its ERP (Enterprise Resource Planning) segment, amounting to PLN388.19 million.

Asseco Business Solutions, a nimble player in the software sector, showcases high-quality earnings and maintains a satisfactory net debt to equity ratio of 3.9%. Despite its earnings growth of 10.1% over the past year lagging behind the industry average of 15.2%, it has consistently grown profits by 7.8% annually over five years. The company is trading at an attractive valuation, estimated to be 29% below fair value, and recently completed a share buyback worth PLN 35.16 million for 600,000 shares or about 1.8%. With revenue forecasted to grow at a steady pace of around 7.45% per year, Asseco seems poised for continued stability in its niche market segment.

- Click to explore a detailed breakdown of our findings in Asseco Business Solutions' health report.

Assess Asseco Business Solutions' past performance with our detailed historical performance reports.

Key Takeaways

- Click this link to deep-dive into the 4642 companies within our Undiscovered Gems With Strong Fundamentals screener.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Betsson might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:BETS B

Betsson

Through its subsidiaries, invests in and manages online gaming business in the Nordic countries, Latin America, Western Europe, Central and Eastern Europe, Central Asia, and internationally.

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion