Advertisement

- Poland

- /

- Specialty Stores

- /

- WSE:BTF

With A 31% Price Drop For Vakomtek S.A. (WSE:VKT) You'll Still Get What You Pay For

Vakomtek S.A. (WSE:VKT) shareholders that were waiting for something to happen have been dealt a blow with a 31% share price drop in the last month. Looking back over the past twelve months the stock has been a solid performer regardless, with a gain of 18%.

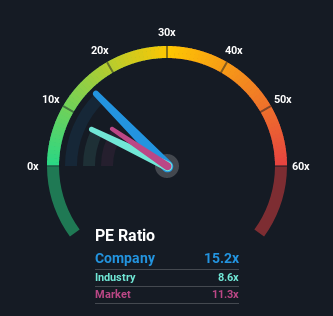

Although its price has dipped substantially, Vakomtek's price-to-earnings (or "P/E") ratio of 15.2x might still make it look like a sell right now compared to the market in Poland, where around half of the companies have P/E ratios below 11x and even P/E's below 6x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's lofty.

With earnings growth that's exceedingly strong of late, Vakomtek has been doing very well. The P/E is probably high because investors think this strong earnings growth will be enough to outperform the broader market in the near future. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

See our latest analysis for Vakomtek

Is There Enough Growth For Vakomtek?

There's an inherent assumption that a company should outperform the market for P/E ratios like Vakomtek's to be considered reasonable.

Taking a look back first, we see that the company grew earnings per share by an impressive 161% last year. Although, its longer-term performance hasn't been as strong with three-year EPS growth being relatively non-existent overall. Therefore, it's fair to say that earnings growth has been inconsistent recently for the company.

In contrast to the company, the rest of the market is expected to decline by 4.1% over the next year, which puts the company's recent medium-term positive growth rates in a good light for now.

With this information, we can see why Vakomtek is trading at a high P/E compared to the market. Investors are willing to pay more for a stock they hope will buck the trend of the broader market going backwards. However, its current earnings trajectory will be very difficult to maintain against the headwinds other companies are facing at the moment.

The Key Takeaway

There's still some solid strength behind Vakomtek's P/E, if not its share price lately. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Vakomtek maintains its high P/E on the strength of its recentthree-year growth beating forecasts for a struggling market, as expected. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. Our only concern is whether its earnings trajectory can keep outperforming under these tough market conditions. Otherwise, it's hard to see the share price falling strongly in the near future if its earnings performance persists.

Don't forget that there may be other risks. For instance, we've identified 4 warning signs for Vakomtek (2 shouldn't be ignored) you should be aware of.

You might be able to find a better investment than Vakomtek. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a P/E below 20x (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if BTCS might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:BTF

Medium-low risk with worrying balance sheet.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor