Advertisement

- Poland

- /

- Specialty Stores

- /

- WSE:APR

Could The Market Be Wrong About Auto Partner SA (WSE:APR) Given Its Attractive Financial Prospects?

It is hard to get excited after looking at Auto Partner's (WSE:APR) recent performance, when its stock has declined 22% over the past three months. But if you pay close attention, you might gather that its strong financials could mean that the stock could potentially see an increase in value in the long-term, given how markets usually reward companies with good financial health. In this article, we decided to focus on Auto Partner's ROE.

Return on equity or ROE is a key measure used to assess how efficiently a company's management is utilizing the company's capital. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

View our latest analysis for Auto Partner

How Do You Calculate Return On Equity?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Auto Partner is:

17% = zł198m ÷ zł1.2b (Based on the trailing twelve months to September 2024).

The 'return' is the profit over the last twelve months. So, this means that for every PLN1 of its shareholder's investments, the company generates a profit of PLN0.17.

Why Is ROE Important For Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

Auto Partner's Earnings Growth And 17% ROE

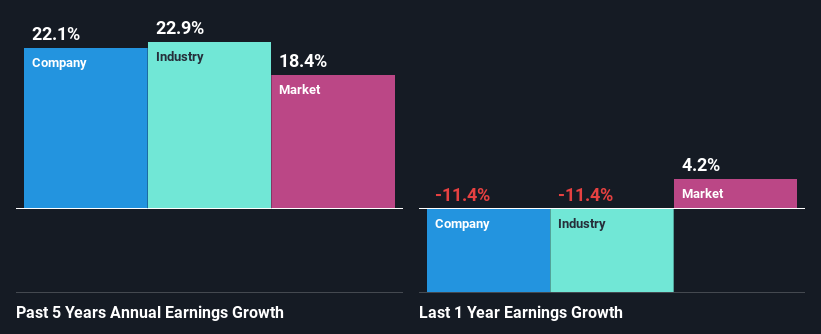

At first glance, Auto Partner seems to have a decent ROE. Be that as it may, the company's ROE is still quite lower than the industry average of 24%. However, we are pleased to see the impressive 22% net income growth reported by Auto Partner over the past five years. Therefore, there could be other causes behind this growth. Such as - high earnings retention or an efficient management in place. Bear in mind, the company does have a respectable ROE. It is just that the industry ROE is higher. So this also does lend some color to the high earnings growth seen by the company.

As a next step, we compared Auto Partner's net income growth with the industry and found that the company has a similar growth figure when compared with the industry average growth rate of 23% in the same period.

Earnings growth is a huge factor in stock valuation. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. Doing so will help them establish if the stock's future looks promising or ominous. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if Auto Partner is trading on a high P/E or a low P/E, relative to its industry.

Is Auto Partner Using Its Retained Earnings Effectively?

Auto Partner has a really low three-year median payout ratio of 9.5%, meaning that it has the remaining 91% left over to reinvest into its business. This suggests that the management is reinvesting most of the profits to grow the business as evidenced by the growth seen by the company.

Additionally, Auto Partner has paid dividends over a period of six years which means that the company is pretty serious about sharing its profits with shareholders.

Conclusion

Overall, we are quite pleased with Auto Partner's performance. Particularly, we like that the company is reinvesting heavily into its business at a moderate rate of return. Unsurprisingly, this has led to an impressive earnings growth. The latest industry analyst forecasts show that the company is expected to maintain its current growth rate. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:APR

Auto Partner

Imports and distributes spare parts for cars, light commercial vehicles, and motorcycles in Poland.

Very undervalued with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor