Advertisement

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that WISE Finance S.A. (WSE:IBS) does use debt in its business. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for WISE Finance

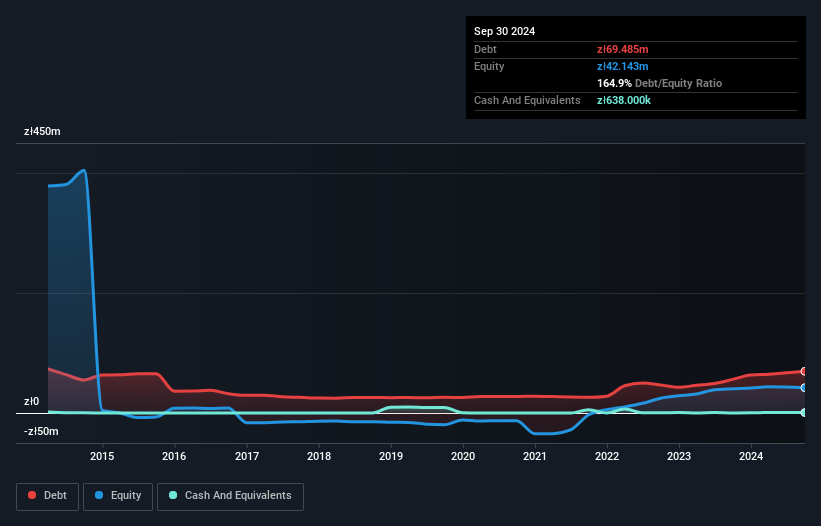

What Is WISE Finance's Debt?

The image below, which you can click on for greater detail, shows that at September 2024 WISE Finance had debt of zł69.5m, up from zł56.1m in one year. Net debt is about the same, since the it doesn't have much cash.

A Look At WISE Finance's Liabilities

The latest balance sheet data shows that WISE Finance had liabilities of zł62.2m due within a year, and liabilities of zł33.7m falling due after that. On the other hand, it had cash of zł638.0k and zł112.1m worth of receivables due within a year. So it can boast zł16.9m more liquid assets than total liabilities.

This luscious liquidity implies that WISE Finance's balance sheet is sturdy like a giant sequoia tree. With this in mind one could posit that its balance sheet means the company is able to handle some adversity. When analysing debt levels, the balance sheet is the obvious place to start. But it is WISE Finance's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year WISE Finance had a loss before interest and tax, and actually shrunk its revenue by 42%, to zł11m. That makes us nervous, to say the least.

Caveat Emptor

While WISE Finance's falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. Its EBIT loss was a whopping zł3.8m. That said, we're impressed with the strong balance sheet liquidity. That should give the business time to grow its cashflow. While the stock is probably a bit risky, there may be an opportunity if the business itself improves, allowing the company to stage a recovery. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. We've identified 5 warning signs with WISE Finance (at least 2 which are significant) , and understanding them should be part of your investment process.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Valuation is complex, but we're here to simplify it.

Discover if WISE Finance might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:IBS

WISE Finance

Provides consulting services in real estate sector in Poland.

Good value with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor