Advertisement

- Poland

- /

- Paper and Forestry Products

- /

- WSE:KLN

KLON Spólka Akcyjna (WSE:KLN) Has A Pretty Healthy Balance Sheet

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, KLON Spólka Akcyjna (WSE:KLN) does carry debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for KLON Spólka Akcyjna

What Is KLON Spólka Akcyjna's Debt?

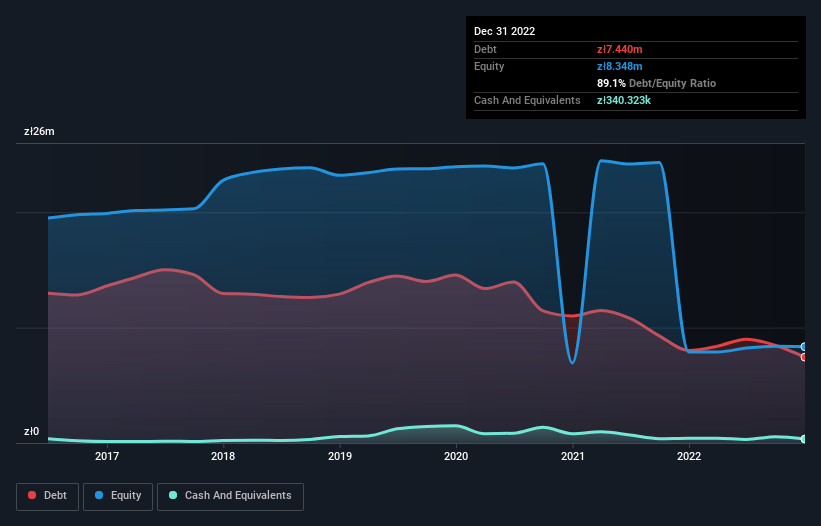

The image below, which you can click on for greater detail, shows that KLON Spólka Akcyjna had debt of zł7.44m at the end of December 2022, a reduction from zł8.02m over a year. However, because it has a cash reserve of zł340.3k, its net debt is less, at about zł7.10m.

A Look At KLON Spólka Akcyjna's Liabilities

According to the last reported balance sheet, KLON Spólka Akcyjna had liabilities of zł4.11m due within 12 months, and liabilities of zł6.09m due beyond 12 months. Offsetting this, it had zł340.3k in cash and zł3.78m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by zł6.08m.

Of course, KLON Spólka Akcyjna has a market capitalization of zł43.1m, so these liabilities are probably manageable. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

KLON Spólka Akcyjna's net debt is sitting at a very reasonable 2.4 times its EBITDA, while its EBIT covered its interest expense just 4.4 times last year. In large part that's due to the company's significant depreciation and amortisation charges, which arguably mean its EBITDA is a very generous measure of earnings, and its debt may be more of a burden than it first appears. Unfortunately, KLON Spólka Akcyjna's EBIT flopped 15% over the last four quarters. If that sort of decline is not arrested, then the managing its debt will be harder than selling broccoli flavoured ice-cream for a premium. When analysing debt levels, the balance sheet is the obvious place to start. But it is KLON Spólka Akcyjna's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we always check how much of that EBIT is translated into free cash flow. During the last three years, KLON Spólka Akcyjna generated free cash flow amounting to a very robust 82% of its EBIT, more than we'd expect. That puts it in a very strong position to pay down debt.

Our View

When it comes to the balance sheet, the standout positive for KLON Spólka Akcyjna was the fact that it seems able to convert EBIT to free cash flow confidently. But the other factors we noted above weren't so encouraging. In particular, EBIT growth rate gives us cold feet. When we consider all the factors mentioned above, we do feel a bit cautious about KLON Spólka Akcyjna's use of debt. While we appreciate debt can enhance returns on equity, we'd suggest that shareholders keep close watch on its debt levels, lest they increase. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 4 warning signs with KLON Spólka Akcyjna (at least 2 which make us uncomfortable) , and understanding them should be part of your investment process.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're here to simplify it.

Discover if KLON Spólka Akcyjna might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:KLN

KLON Spólka Akcyjna

Produces and sells timber, elements, and glued boards in Poland and internationally.

Low risk and slightly overvalued.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor