Advertisement

- Sweden

- /

- Life Sciences

- /

- OM:BIOT

Sartorius Stedim Biotech And 2 Other Undiscovered Gems With Strong Fundamentals

Simply Wall St

Reviewed by Simply Wall St

As European markets navigate renewed uncertainty surrounding U.S. trade policy and escalating geopolitical tensions in the Middle East, major stock indexes have experienced notable declines, with the pan-European STOXX Europe 600 Index ending 1.57% lower recently. Amidst these turbulent conditions, investors often turn their attention to companies with strong fundamentals that can weather economic fluctuations and potentially offer stability and growth opportunities. In this context, Sartorius Stedim Biotech and two other lesser-known stocks stand out as potential gems worth exploring for their robust financial health and strategic positioning in the market.

Top 10 Undiscovered Gems With Strong Fundamentals In Europe

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Caisse Régionale de Crédit Agricole Mutuel Brie Picardie Société coopérative | 26.90% | 4.14% | 7.22% | ★★★★★★ |

| La Forestière Equatoriale | NA | -65.30% | 37.55% | ★★★★★★ |

| Martifer SGPS | 102.88% | -0.23% | 7.16% | ★★★★★★ |

| Linc | NA | 101.28% | 29.81% | ★★★★★★ |

| ABG Sundal Collier Holding | 8.55% | -4.14% | -12.38% | ★★★★★☆ |

| Caisse Regionale de Credit Agricole Mutuel Toulouse 31 | 19.46% | 0.47% | 7.14% | ★★★★★☆ |

| Practic | 5.21% | 4.49% | 7.23% | ★★★★☆☆ |

| Darwin | 3.03% | 84.88% | 5.63% | ★★★★☆☆ |

| Grenobloise d'Electronique et d'Automatismes Société Anonyme | 0.01% | 5.17% | -13.11% | ★★★★☆☆ |

| Eurofins-Cerep | 0.46% | 6.80% | 6.93% | ★★★★☆☆ |

Here's a peek at a few of the choices from the screener.

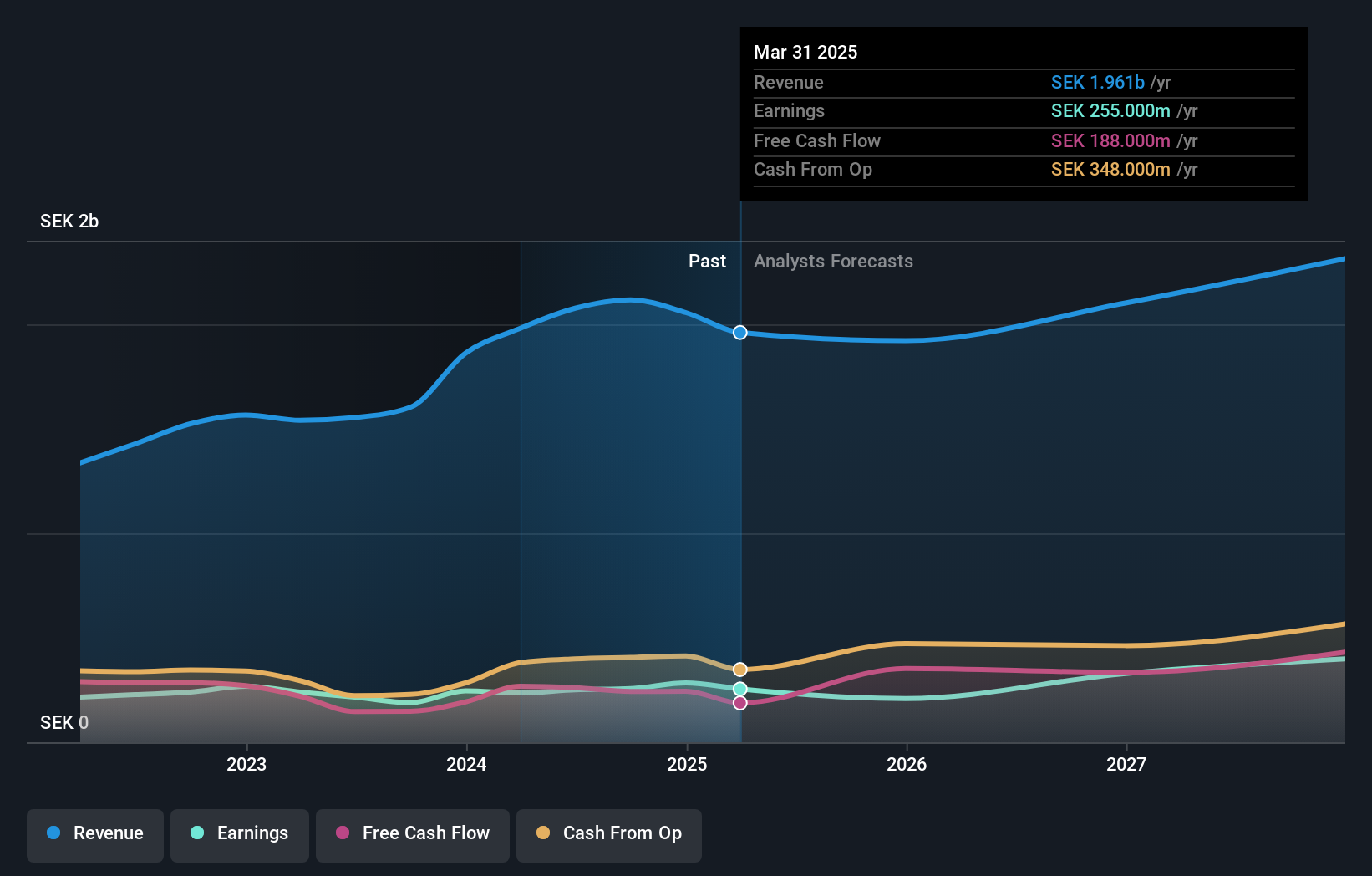

Biotage (OM:BIOT)

Simply Wall St Value Rating: ★★★★★★

Overview: Biotage AB (publ) offers solutions and products for drug discovery and development, analytical testing, and water and environmental testing, with a market cap of SEK11.48 billion.

Operations: Biotage generates revenue primarily from its healthcare software segment, which accounted for SEK1.96 billion.

Biotage, a nimble player in the life sciences sector, has seen its earnings grow by 8.1% over the past year, outpacing the industry average of -0.7%. The company’s debt-to-equity ratio improved significantly from 11.4% to 3.9% over five years, indicating a stronger financial footing with more cash than total debt. Despite a volatile share price recently, Biotage trades at about 20.8% below its fair value estimate and maintains high-quality earnings with forecasts suggesting annual revenue growth of around 5.4%. Recent developments include a SEK143 per share acquisition offer from Kohlberg Kravis Roberts & Co., reflecting potential strategic shifts ahead for Biotage amidst ongoing capacity upgrades in its bioprocessing segment that could boost future opportunities despite existing supply chain challenges and reliance on key customers potentially affecting consistent growth prospects.

XANO Industri (OM:XANO B)

Simply Wall St Value Rating: ★★★★★★

Overview: XANO Industri AB (publ) develops, manufactures, and sells industrial products and automation equipment across Sweden, the rest of the Nordic countries, Europe, and internationally with a market capitalization of SEK3.49 billion.

Operations: XANO Industri generates revenue primarily from three segments: Industrial Solutions (SEK2.07 billion), Industrial Products (SEK852.13 million), and Precision Technology (SEK461.89 million). The company's net profit margin reflects its profitability after accounting for all expenses, providing insight into its financial efficiency and overall performance.

XANO Industri, a nimble player in the machinery sector, has shown resilience with earnings growth of 2.8% over the past year, outpacing industry peers. The company is debt-free now, a significant shift from five years ago when its debt-to-equity ratio stood at 84.8%. Recent first-quarter results highlight sales climbing to SEK893 million from SEK825 million last year and net income leaping to SEK48 million from SEK13 million. However, a one-off gain of SEK66.1M skews recent financials slightly. With positive free cash flow and no debt concerns, XANO seems well-positioned for future opportunities despite past earnings declines.

- Navigate through the intricacies of XANO Industri with our comprehensive health report here.

Understand XANO Industri's track record by examining our Past report.

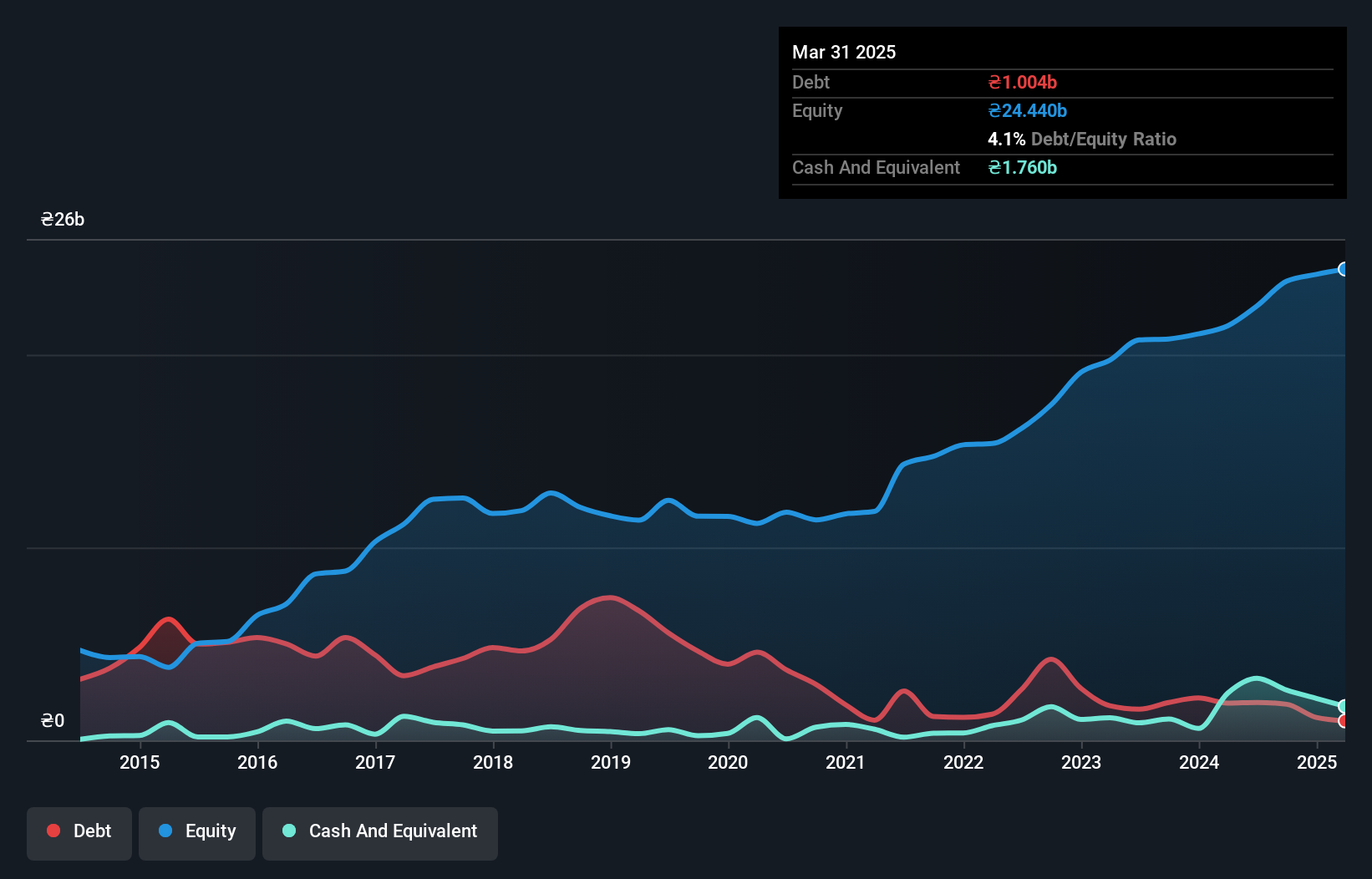

Astarta Holding (WSE:AST)

Simply Wall St Value Rating: ★★★★★★

Overview: Astarta Holding PLC operates in sugar production, crop growing, soybean processing, and cattle farming across Ukraine and internationally, with a market capitalization of PLN1.44 billion.

Operations: The company generates revenue primarily from agriculture (UAH13.29 billion), sugar production (UAH9.89 billion), and soybean processing (UAH4.64 billion). Cattle farming also contributes to its revenue streams with UAH2.48 billion.

Astarta Holding, a Ukrainian agricultural company, has seen its earnings grow by 61% over the past year, significantly outpacing the food industry's -9.2% performance. The company's debt to equity ratio improved from 40.7% to 4.1% over five years, reflecting effective financial management. Despite trading at an estimated 88% below fair value and having high-quality earnings with well-covered interest payments (4.3x EBIT coverage), recent challenges include declining sugar prices and adverse weather affecting margins. A USD$40 million financing deal supports their soy protein concentrate plant construction, yet going concern doubts persist due to geopolitical tensions impacting supply chains and investment delays.

Seize The Opportunity

- Dive into all 335 of the European Undiscovered Gems With Strong Fundamentals we have identified here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Biotage might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:BIOT

Biotage

Provides solutions and products in the areas of drug discovery and development, analytical testing, and water and environmental testing.

Flawless balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor