Advertisement

If you're looking for a multi-bagger, there's a few things to keep an eye out for. In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. However, after investigating AmRest Holdings (WSE:EAT), we don't think it's current trends fit the mold of a multi-bagger.

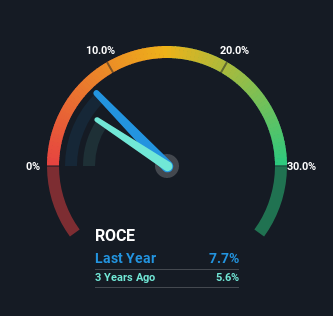

Understanding Return On Capital Employed (ROCE)

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. The formula for this calculation on AmRest Holdings is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.077 = €127m ÷ (€2.3b - €626m) (Based on the trailing twelve months to December 2022).

So, AmRest Holdings has an ROCE of 7.7%. On its own that's a low return on capital but it's in line with the industry's average returns of 8.4%.

View our latest analysis for AmRest Holdings

Above you can see how the current ROCE for AmRest Holdings compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like, you can check out the forecasts from the analysts covering AmRest Holdings here for free.

So How Is AmRest Holdings' ROCE Trending?

There are better returns on capital out there than what we're seeing at AmRest Holdings. The company has consistently earned 7.7% for the last five years, and the capital employed within the business has risen 106% in that time. This poor ROCE doesn't inspire confidence right now, and with the increase in capital employed, it's evident that the business isn't deploying the funds into high return investments.

What We Can Learn From AmRest Holdings' ROCE

In summary, AmRest Holdings has simply been reinvesting capital and generating the same low rate of return as before. And in the last five years, the stock has given away 58% so the market doesn't look too hopeful on these trends strengthening any time soon. Therefore based on the analysis done in this article, we don't think AmRest Holdings has the makings of a multi-bagger.

If you'd like to know more about AmRest Holdings, we've spotted 3 warning signs, and 1 of them is potentially serious.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:EAT

AmRest Holdings

Operates and manages quick service, fast casual, coffee, and casual dining restaurants in Central and Eastern Europe, Western Europe, China, and internationally.

Good value with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.5% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|30.7% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|88.1% undervalued

AG

Community Contributor