Advertisement

ESOTIQ & Henderson (WSE:EAH) Takes On Some Risk With Its Use Of Debt

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, ESOTIQ & Henderson S.A. (WSE:EAH) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for ESOTIQ & Henderson

What Is ESOTIQ & Henderson's Net Debt?

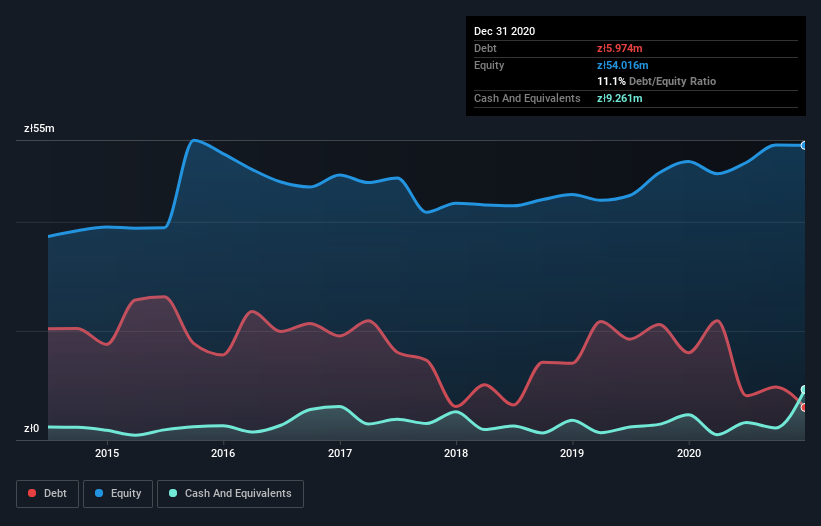

The image below, which you can click on for greater detail, shows that ESOTIQ & Henderson had debt of zł5.97m at the end of December 2020, a reduction from zł16.0m over a year. But on the other hand it also has zł9.26m in cash, leading to a zł3.29m net cash position.

How Strong Is ESOTIQ & Henderson's Balance Sheet?

According to the last reported balance sheet, ESOTIQ & Henderson had liabilities of zł48.3m due within 12 months, and liabilities of zł41.2m due beyond 12 months. Offsetting these obligations, it had cash of zł9.26m as well as receivables valued at zł13.5m due within 12 months. So it has liabilities totalling zł66.7m more than its cash and near-term receivables, combined.

This deficit casts a shadow over the zł42.4m company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. After all, ESOTIQ & Henderson would likely require a major re-capitalisation if it had to pay its creditors today. Given that ESOTIQ & Henderson has more cash than debt, we're pretty confident it can handle its debt, despite the fact that it has a lot of liabilities in total.

The bad news is that ESOTIQ & Henderson saw its EBIT decline by 12% over the last year. If earnings continue to decline at that rate then handling the debt will be more difficult than taking three children under 5 to a fancy pants restaurant. There's no doubt that we learn most about debt from the balance sheet. But it is ESOTIQ & Henderson's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. While ESOTIQ & Henderson has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the last three years, ESOTIQ & Henderson actually produced more free cash flow than EBIT. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Summing up

Although ESOTIQ & Henderson's balance sheet isn't particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of zł3.29m. The cherry on top was that in converted 119% of that EBIT to free cash flow, bringing in zł27m. Despite its cash we think that ESOTIQ & Henderson seems to struggle to handle its total liabilities, so we are wary of the stock. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 2 warning signs for ESOTIQ & Henderson that you should be aware of before investing here.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you’re looking to trade ESOTIQ & Henderson, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if ESOTIQ & Henderson might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About WSE:EAH

ESOTIQ & Henderson

Designs, manufactures, and sells lingerie, clothing, and cosmetics in Poland and internationally.

Medium-low risk and fair value.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor