Advertisement

ESOTIQ & Henderson (WSE:EAH) Takes On Some Risk With Its Use Of Debt

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies ESOTIQ & Henderson S.A. (WSE:EAH) makes use of debt. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for ESOTIQ & Henderson

How Much Debt Does ESOTIQ & Henderson Carry?

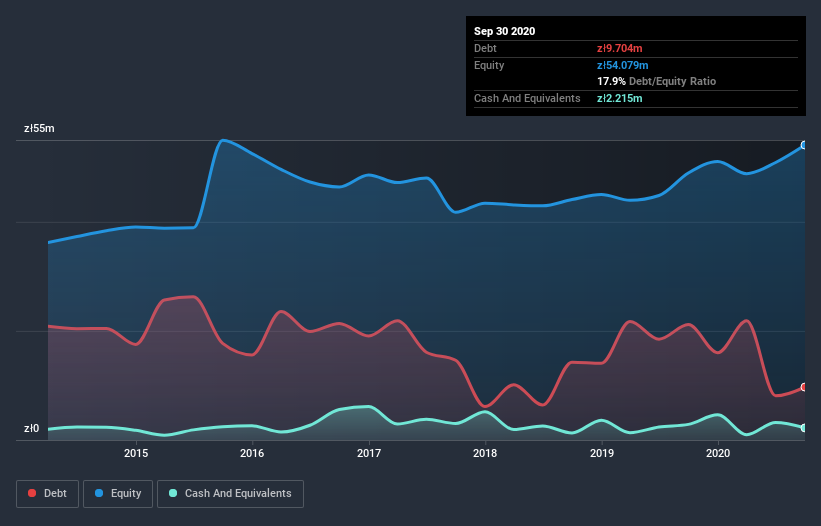

The image below, which you can click on for greater detail, shows that ESOTIQ & Henderson had debt of zł9.70m at the end of September 2020, a reduction from zł21.2m over a year. However, it does have zł2.22m in cash offsetting this, leading to net debt of about zł7.49m.

How Healthy Is ESOTIQ & Henderson's Balance Sheet?

The latest balance sheet data shows that ESOTIQ & Henderson had liabilities of zł44.2m due within a year, and liabilities of zł41.8m falling due after that. On the other hand, it had cash of zł2.22m and zł16.7m worth of receivables due within a year. So its liabilities total zł67.1m more than the combination of its cash and short-term receivables.

The deficiency here weighs heavily on the zł39.9m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we definitely think shareholders need to watch this one closely. At the end of the day, ESOTIQ & Henderson would probably need a major re-capitalization if its creditors were to demand repayment.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

While ESOTIQ & Henderson's low debt to EBITDA ratio of 0.49 suggests only modest use of debt, the fact that EBIT only covered the interest expense by 3.7 times last year does give us pause. So we'd recommend keeping a close eye on the impact financing costs are having on the business. Also relevant is that ESOTIQ & Henderson has grown its EBIT by a very respectable 21% in the last year, thus enhancing its ability to pay down debt. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since ESOTIQ & Henderson will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. Happily for any shareholders, ESOTIQ & Henderson actually produced more free cash flow than EBIT over the last three years. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Our View

While ESOTIQ & Henderson's level of total liabilities has us nervous. For example, its conversion of EBIT to free cash flow and net debt to EBITDA give us some confidence in its ability to manage its debt. Looking at all the angles mentioned above, it does seem to us that ESOTIQ & Henderson is a somewhat risky investment as a result of its debt. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Consider for instance, the ever-present spectre of investment risk. We've identified 3 warning signs with ESOTIQ & Henderson , and understanding them should be part of your investment process.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

When trading ESOTIQ & Henderson or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if ESOTIQ & Henderson might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About WSE:EAH

ESOTIQ & Henderson

Designs, manufactures, and sells lingerie, clothing, and cosmetics in Poland and internationally.

Medium-low risk and fair value.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor