Advertisement

- Poland

- /

- Consumer Durables

- /

- WSE:1AT

This Is The Reason Why We Think Atal S.A.'s (WSE:1AT) CEO Might Be Underpaid

Key Insights

- Atal to hold its Annual General Meeting on 20th of June

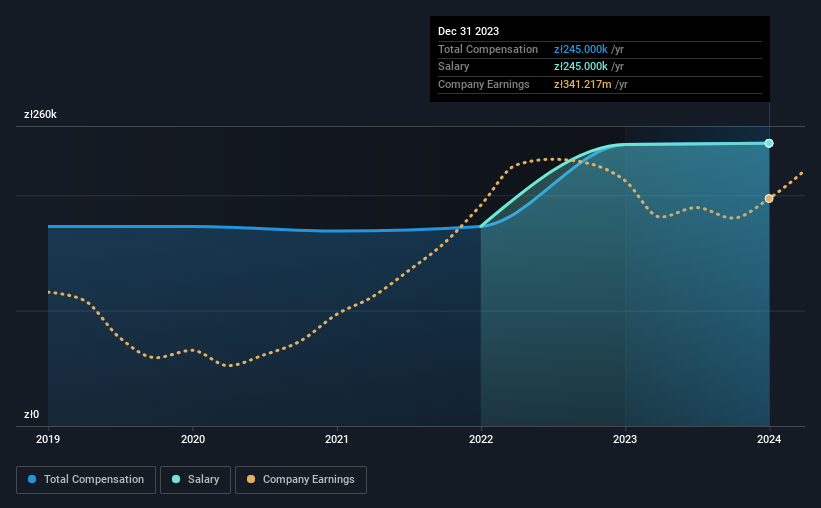

- Salary of zł245.0k is part of CEO Zbigniew Juroszek's total remuneration

- The total compensation is 93% less than the average for the industry

- Atal's total shareholder return over the past three years was 56% while its EPS grew by 21% over the past three years

Shareholders will be pleased by the impressive results for Atal S.A. (WSE:1AT) recently and CEO Zbigniew Juroszek has played a key role. At the upcoming AGM on 20th of June, they would be interested to hear about the company strategy going forward and get a chance to cast their votes on resolutions such as executive remuneration and other company matters. Here we will show why we think CEO compensation is appropriate and discuss the case for a pay rise.

See our latest analysis for Atal

How Does Total Compensation For Zbigniew Juroszek Compare With Other Companies In The Industry?

At the time of writing, our data shows that Atal S.A. has a market capitalization of zł2.5b, and reported total annual CEO compensation of zł245k for the year to December 2023. This means that the compensation hasn't changed much from last year. Notably, the salary of zł245k is the entirety of the CEO compensation.

On comparing similar companies from the Polish Consumer Durables industry with market caps ranging from zł1.6b to zł6.5b, we found that the median CEO total compensation was zł3.6m. In other words, Atal pays its CEO lower than the industry median. Furthermore, Zbigniew Juroszek directly owns zł1.9b worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | zł245k | zł244k | 100% |

| Other | - | - | - |

| Total Compensation | zł245k | zł244k | 100% |

On an industry level, around 60% of total compensation represents salary and 40% is other remuneration. Speaking on a company level, Atal prefers to tread along a traditional path, disbursing all compensation through a salary. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

A Look at Atal S.A.'s Growth Numbers

Over the past three years, Atal S.A. has seen its earnings per share (EPS) grow by 21% per year. It achieved revenue growth of 18% over the last year.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's also good to see decent revenue growth in the last year, suggesting the business is healthy and growing. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Atal S.A. Been A Good Investment?

We think that the total shareholder return of 56%, over three years, would leave most Atal S.A. shareholders smiling. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

To Conclude...

Atal rewards its CEO solely through a salary, ignoring non-salary benefits completely. The company's solid performance might have made most shareholders happy, possibly making CEO remuneration the least of the matters to be discussed in the AGM. Instead, investors might be more interested in discussions that would help manage their longer-term growth expectations such as company business strategies and future growth potential.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. That's why we did some digging and identified 2 warning signs for Atal that investors should think about before committing capital to this stock.

Important note: Atal is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About WSE:1AT

Atal

Engages in the construction and sale of residential real estate and the rental of commercial real estate in Poland.

Very undervalued with high growth potential.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CE

cementafriend on Constellation Energy ·

Constellation Energy Dividends and Growth

Fair Value:US$348.054.7% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KH

Khagani on CoreWeave ·

CoreWeave's Revenue Expected to Rocket 77.88% in 5-Year Forecast

Fair Value:US$11033.5% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

108 followersusers have followed this narrative

10 commentsusers have commented on this narrative

21 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

936 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

144 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative