Advertisement

Przedsiebiorstwo Hydrauliki Silowej HYDROTOR (WSE:HDR) Seems To Use Debt Quite Sensibly

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Przedsiebiorstwo Hydrauliki Silowej HYDROTOR S.A. (WSE:HDR) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Przedsiebiorstwo Hydrauliki Silowej HYDROTOR

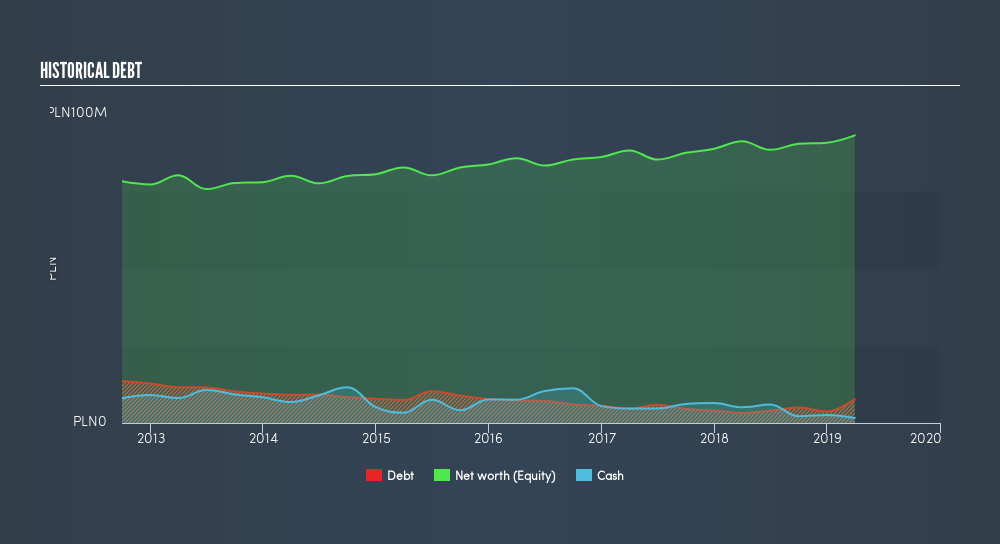

How Much Debt Does Przedsiebiorstwo Hydrauliki Silowej HYDROTOR Carry?

The image below, which you can click on for greater detail, shows that at March 2019 Przedsiebiorstwo Hydrauliki Silowej HYDROTOR had debt of zł7.72m, up from zł3.73m in one year. However, it also had zł1.66m in cash, and so its net debt is zł6.06m.

How Healthy Is Przedsiebiorstwo Hydrauliki Silowej HYDROTOR's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Przedsiebiorstwo Hydrauliki Silowej HYDROTOR had liabilities of zł21.5m due within 12 months and liabilities of zł20.4m due beyond that. On the other hand, it had cash of zł1.66m and zł24.0m worth of receivables due within a year. So its liabilities total zł16.2m more than the combination of its cash and short-term receivables.

Of course, Przedsiebiorstwo Hydrauliki Silowej HYDROTOR has a market capitalization of zł90.2m, so these liabilities are probably manageable. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. Because it carries more debt than cash, we think it's worth watching Przedsiebiorstwo Hydrauliki Silowej HYDROTOR's balance sheet over time.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Przedsiebiorstwo Hydrauliki Silowej HYDROTOR's net debt is only 0.42 times its EBITDA. And its EBIT easily covers its interest expense, being 45.3 times the size. So we're pretty relaxed about its super-conservative use of debt. But the other side of the story is that Przedsiebiorstwo Hydrauliki Silowej HYDROTOR saw its EBIT decline by 9.2% over the last year. That sort of decline, if sustained, will obviously make debt harder to handle. When analysing debt levels, the balance sheet is the obvious place to start. But it is Przedsiebiorstwo Hydrauliki Silowej HYDROTOR's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Looking at the most recent three years, Przedsiebiorstwo Hydrauliki Silowej HYDROTOR recorded free cash flow of 32% of its EBIT, which is weaker than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Our View

On our analysis Przedsiebiorstwo Hydrauliki Silowej HYDROTOR's interest cover should signal that it won't have too much trouble with its debt. But the other factors we noted above weren't so encouraging. For instance it seems like it has to struggle a bit to grow its EBIT. Looking at all this data makes us feel a little cautious about Przedsiebiorstwo Hydrauliki Silowej HYDROTOR's debt levels. While we appreciate debt can enhance returns on equity, we'd suggest that shareholders keep close watch on its debt levels, lest they increase. Given Przedsiebiorstwo Hydrauliki Silowej HYDROTOR has a strong balance sheet is profitable and pays a dividend, it would be good to know how fast its dividends are growing, if at all. You can find out instantly by clicking this link.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About WSE:HDR

Przedsiebiorstwo Hydrauliki Silowej HYDROTOR

Przedsiebiorstwo Hydrauliki Silowej HYDROTOR S.A.

Adequate balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|31.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|24.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|13.5% overvalued

DA

Community Contributor