Advertisement

- New Zealand

- /

- Software

- /

- NZSE:SDL

Solution Dynamics' (NZSE:SDL) Dividend Will Be NZ$0.04

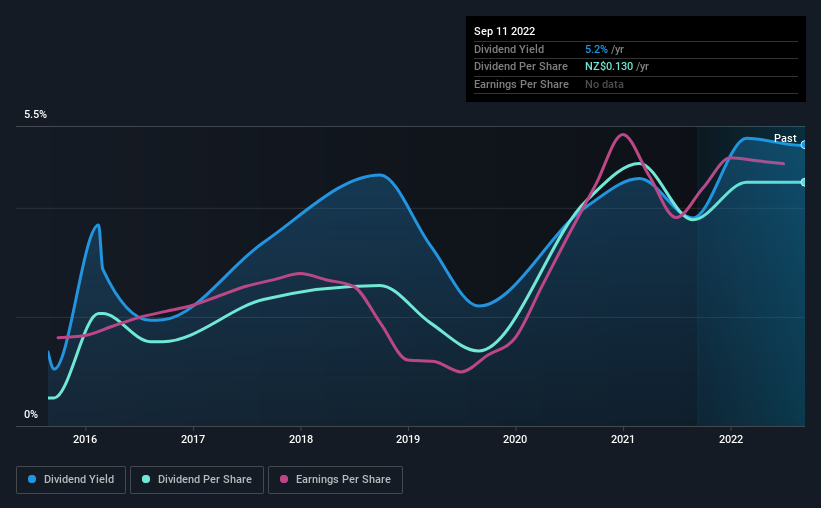

Solution Dynamics Limited's (NZSE:SDL) investors are due to receive a payment of NZ$0.04 per share on 30th of September. Based on this payment, the dividend yield on the company's stock will be 5.2%, which is an attractive boost to shareholder returns.

See our latest analysis for Solution Dynamics

Solution Dynamics' Payment Has Solid Earnings Coverage

If the payments aren't sustainable, a high yield for a few years won't matter that much. The last payment made up 74% of earnings, but cash flows were much higher. In general, cash flows are more important than earnings, so we are comfortable that the dividend will be sustainable going forward, especially with so much cash left over for reinvestment.

EPS is set to grow by 13.3% over the next year if recent trends continue. Assuming the dividend continues along recent trends, our estimates say the payout ratio could reach 77%, which is definitely on the higher side, but we wouldn't necessarily say this is unsustainable.

Solution Dynamics' Dividend Has Lacked Consistency

Solution Dynamics has been paying dividends for a while, but the track record isn't stellar. If the company cuts once, it definitely isn't argument against the possibility of it cutting in the future. The dividend has gone from an annual total of NZ$0.015 in 2015 to the most recent total annual payment of NZ$0.13. This means that it has been growing its distributions at 36% per annum over that time. Despite the rapid growth in the dividend over the past number of years, we have seen the payments go down the past as well, so that makes us cautious.

The Dividend Looks Likely To Grow

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. We are encouraged to see that Solution Dynamics has grown earnings per share at 13% per year over the past five years. Past earnings growth has been decent, but unless this is one of those rare businesses that can grow without additional capital investment or marketing spend, we'd generally expect the higher payout ratio to limit its future growth prospects.

Solution Dynamics Looks Like A Great Dividend Stock

Overall, we think that this is a great income investment, and we think that maintaining the dividend this year may have been a conservative choice. The company is easily earning enough to cover its dividend payments and it is great to see that these earnings are being translated into cash flow. All in all, this checks a lot of the boxes we look for when choosing an income stock.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. For instance, we've picked out 2 warning signs for Solution Dynamics that investors should take into consideration. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NZSE:SDL

Solution Dynamics

Provides customer communication solutions in New Zealand, Australia, the United States, and Europe.

Flawless balance sheet with slight risk.

Market Insights

Advertisement

Weekly Picks

RI

Rick_Orford on Upside Gold ·

This OVERLOOKED Gold Stock Could TRIPLE - 3.3M Ounces, Bottom-of-Peer Valuation

Fair Value:CA$471.3% undervalued

45 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17030.5% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

FU

FundamentalFlow on Onto Innovation ·

Onto Innovation: The Advanced Packaging Chokepoint 51.3% undervalued intrinsic discount

Fair Value:US$38026.8% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7447.5% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

Recently Updated Narratives

RO

Robbo on Barclays ·

Why Is Barclays Trading Below Book Value?

Fair Value:UK£5.6416.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DC

DCA_rules on Micron Technology ·

Micron Technology (MU): Riding the AI Supercycle to a $100B+ Revenue Horizon and Historic 40%+ Net Profit Margins

Fair Value:US$1.25k14.7% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on Aoyama Zaisan Networks CompanyLimited ·

Preparing for re-acceleration in FY12/27

Fair Value:JP¥1.31k0.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.2% undervalued

123 followersusers have followed this narrative

2 commentsusers have commented on this narrative

35 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9719.7% undervalued

56 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1926.5% undervalued

45 followersusers have followed this narrative

0 commentsusers have commented on this narrative

18 likesusers have liked this narrative