Advertisement

- New Zealand

- /

- Healthcare Services

- /

- NZSE:EBO

EBOS Group (NZSE:EBO) Is Down 5.4% After Earnings Miss and Dividend Update – Has The Bull Case Changed?

Simply Wall St

Reviewed by Simply Wall St

- EBOS Group Limited recently reported full-year results for the period ending June 30, 2025, posting sales of A$12.27 billion and net income of A$215.14 million, both down from the previous year, and announced ordinary and special cash dividends totalling NZ$0.642 per share.

- This combination of softer earnings performance with continued dividend payouts highlights the company’s commitment to shareholder returns amid a period of operational and margin pressures.

- With earnings now lower and new dividend plans in focus, we’ll explore how this earnings miss reshapes EBOS Group’s outlook.

Explore 23 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

EBOS Group Investment Narrative Recap

To own EBOS Group as a shareholder, you need to believe in the company’s ability to maintain its leadership in pharmaceutical and medical distribution, especially as an aging population steadily drives healthcare demand in Australia and New Zealand. The recent slide in both revenue and net income does not appear to materially affect the company’s most important short-term catalyst, which remains the completion and ramp-up benefits expected from the distribution center renewal program. However, the biggest near-term risk, further margin pressure from competition and shifts in product mix, remains firmly in focus after this earnings miss.

Among the recent announcements, the affirmation of both ordinary and special cash dividends totalling NZ$0.642 per share stands out as most relevant. Despite the drop in earnings, this move underscores management’s aim to maintain shareholder returns, though the sustainability of payouts from current earnings is likely to be monitored closely by investors as cost pressures persist.

By contrast, what investors should be aware of is the ongoing risk that persistent margin compression, especially as industry competition intensifies, can continue to weigh on...

Read the full narrative on EBOS Group (it's free!)

EBOS Group's narrative projects A$14.3 billion revenue and A$311.7 million earnings by 2028. This requires 5.3% yearly revenue growth and an earnings increase of A$96.6 million from current earnings of A$215.1 million.

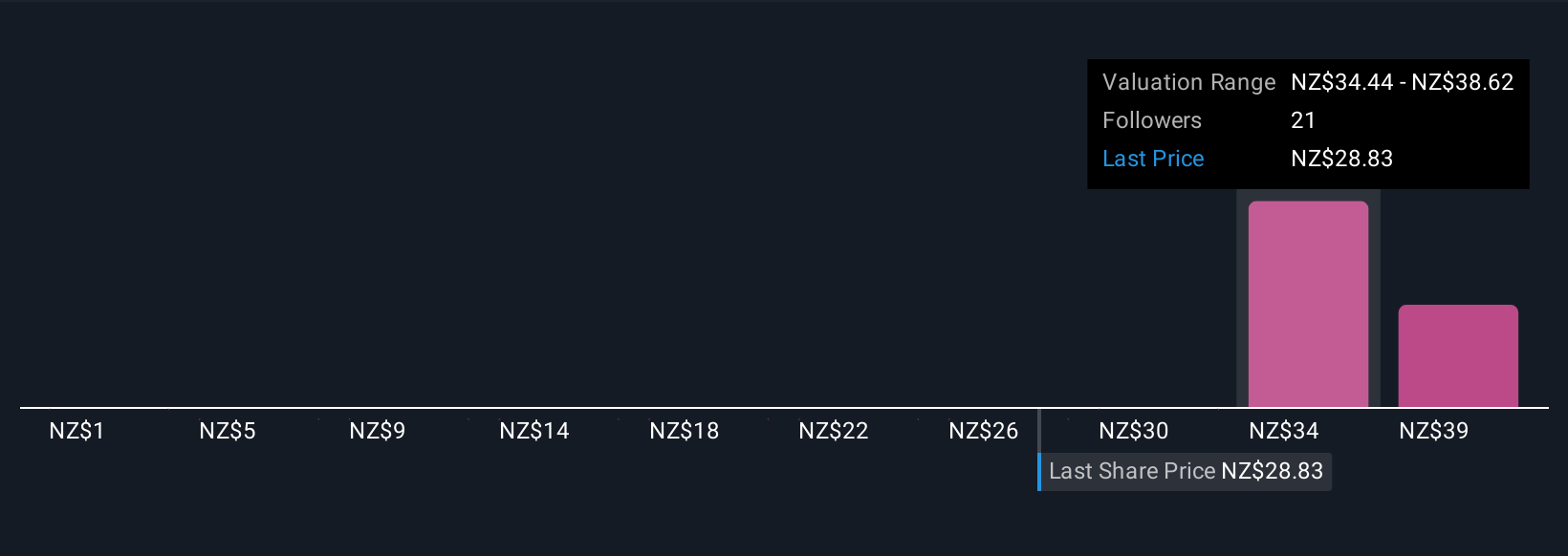

Uncover how EBOS Group's forecasts yield a NZ$37.96 fair value, a 23% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community fair value calculations for EBOS Group range from NZ$32.31 to NZ$42.80, reflecting four distinct viewpoints. With margins under pressure and dividends held steady, you can see how opinions about future performance can vary significantly, explore alternative perspectives to inform your own view.

Explore 4 other fair value estimates on EBOS Group - why the stock might be worth just NZ$32.31!

Build Your Own EBOS Group Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your EBOS Group research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free EBOS Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate EBOS Group's overall financial health at a glance.

Interested In Other Possibilities?

Our top stock finds are flying under the radar-for now. Get in early:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- We've found 18 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if EBOS Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NZSE:EBO

EBOS Group

Engages in the marketing, wholesale, and distribution of healthcare, medical, pharmaceutical, and animal care products in Australia, Southeast Asia, and New Zealand.

Flawless balance sheet average dividend payer.

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.6% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|90.0% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|14.9% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|97.2% undervalued

AG

Community Contributor