Advertisement

Some investors rely on dividends for growing their wealth, and if you're one of those dividend sleuths, you might be intrigued to know that Seeka Limited (NZSE:SEK) is about to go ex-dividend in just 3 days. You will need to purchase shares before the 4th of March to receive the dividend, which will be paid on the 30th of March.

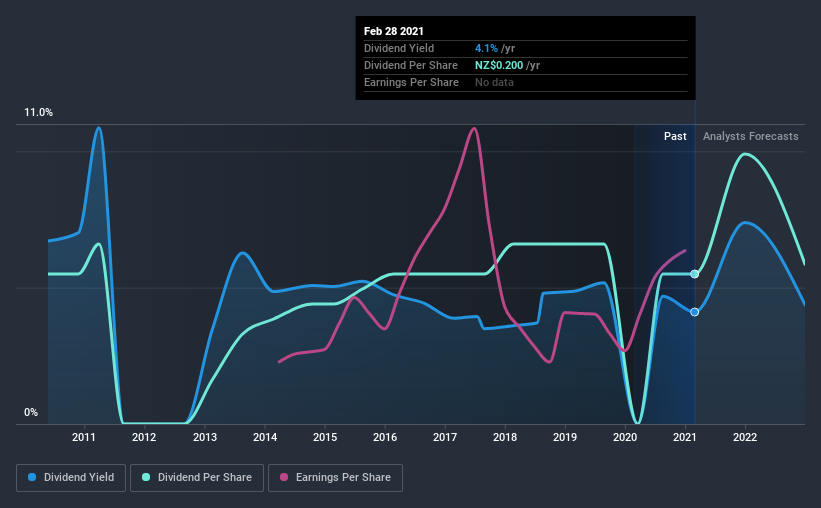

Seeka's upcoming dividend is NZ$0.14 a share, following on from the last 12 months, when the company distributed a total of NZ$0.20 per share to shareholders. Looking at the last 12 months of distributions, Seeka has a trailing yield of approximately 4.1% on its current stock price of NZ$4.87. If you buy this business for its dividend, you should have an idea of whether Seeka's dividend is reliable and sustainable. That's why we should always check whether the dividend payments appear sustainable, and if the company is growing.

Check out our latest analysis for Seeka

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. Seeka paid out just 19% of its profit last year, which we think is conservatively low and leaves plenty of margin for unexpected circumstances. Yet cash flows are even more important than profits for assessing a dividend, so we need to see if the company generated enough cash to pay its distribution. Over the last year it paid out 55% of its free cash flow as dividends, within the usual range for most companies.

It's positive to see that Seeka's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

Click here to see how much of its profit Seeka paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Stocks in companies that generate sustainable earnings growth often make the best dividend prospects, as it is easier to lift the dividend when earnings are rising. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. For this reason, we're glad to see Seeka's earnings per share have risen 13% per annum over the last five years. Seeka has an average payout ratio which suggests a balance between growing earnings and rewarding shareholders. This is a reasonable combination that could hint at some further dividend increases in the future.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. Seeka's dividend payments are effectively flat on where they were 10 years ago.

To Sum It Up

From a dividend perspective, should investors buy or avoid Seeka? From a dividend perspective, we're encouraged to see that earnings per share have been growing, the company is paying out less than half of its earnings, and a bit over half its free cash flow. There's a lot to like about Seeka, and we would prioritise taking a closer look at it.

While it's tempting to invest in Seeka for the dividends alone, you should always be mindful of the risks involved. Our analysis shows 3 warning signs for Seeka that we strongly recommend you have a look at before investing in the company.

We wouldn't recommend just buying the first dividend stock you see, though. Here's a list of interesting dividend stocks with a greater than 2% yield and an upcoming dividend.

When trading Seeka or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NZSE:SEK

Seeka

Provides orchard lease and management, and post-harvest and retail services to the horticulture industry in New Zealand and Australia.

Mediocre balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.1% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.2% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.2% undervalued

MA

Community Contributor