Advertisement

- New Zealand

- /

- Oil and Gas

- /

- NZSE:CHI

NZ$1.09: That's What Analysts Think The New Zealand Refining Company Limited (NZSE:NZR) Is Worth After Its Latest Results

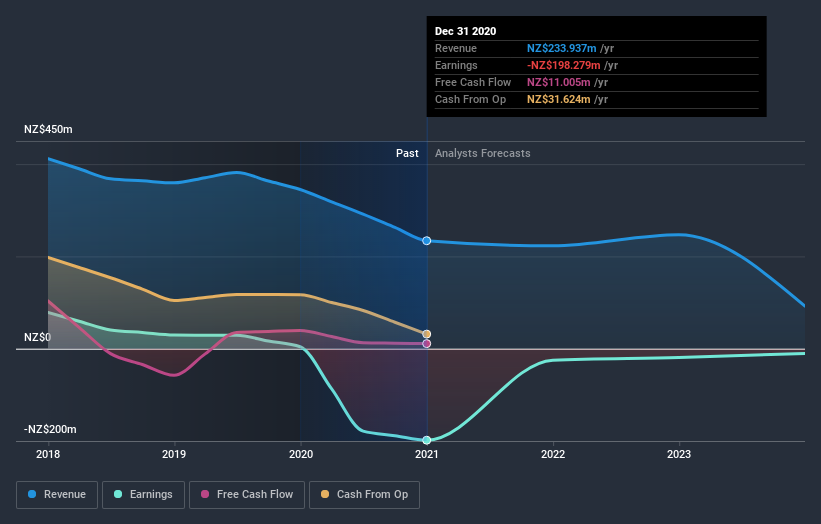

The New Zealand Refining Company Limited (NZSE:NZR) just released its latest annual results and things are looking bullish. New Zealand Refining beat expectations with revenues of NZ$234m arriving 4.2% ahead of forecasts. The company also reported a statutory loss of NZ$0.64, 6.9% smaller than was expected. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

View our latest analysis for New Zealand Refining

After the latest results, the consensus from New Zealand Refining's two analysts is for revenues of NZ$222.8m in 2021, which would reflect a perceptible 4.8% decline in sales compared to the last year of performance. Losses are predicted to fall substantially, shrinking 87% to NZ$0.08. Before this earnings announcement, the analysts had been modelling revenues of NZ$231.5m and losses of NZ$0.089 per share in 2021. While the revenue estimates fell, sentiment seems to have improved, with the analysts making a notable improvement in losses per share in particular.

The analysts have cut their price target 18% to NZ$1.09per share, suggesting that the declining revenue was a more crucial indicator than the forecast reduction in losses.

Of course, another way to look at these forecasts is to place them into context against the industry itself. One thing that stands out from these estimates is that shrinking revenues are expected to moderate from the historical decline of 7.4% per annum over the past five years.

The Bottom Line

The most obvious conclusion is that the analysts made no changes to their forecasts for a loss next year. Unfortunately, they also downgraded their revenue estimates, and our data indicates revenues are expected to perform worse than the wider industry. Even so, earnings per share are more important to the intrinsic value of the business. Even so, long term profitability is more important for the value creation process. Furthermore, the analysts also cut their price targets, suggesting that the latest news has led to greater pessimism about the intrinsic value of the business.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. At least one analyst has provided forecasts out to 2023, which can be seen for free on our platform here.

Before you take the next step you should know about the 1 warning sign for New Zealand Refining that we have uncovered.

If you’re looking to trade New Zealand Refining, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NZSE:CHI

Channel Infrastructure NZ

Provides infrastructure solutions to meet fuel and energy needs in New Zealand.

Adequate balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor