Advertisement

StrongPoint's (OB:STRO) Dividend Will Be Increased To kr0.80

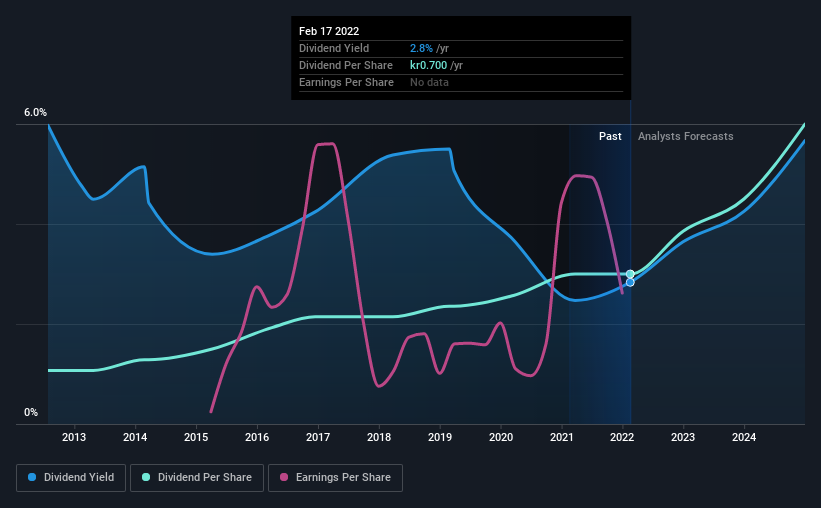

StrongPoint ASA (OB:STRO) has announced that it will be increasing its dividend on the 1st of January to kr0.80, which will be 14% higher than last year. This makes the dividend yield 3.2%, which is above the industry average.

See our latest analysis for StrongPoint

StrongPoint's Dividend Is Well Covered By Earnings

While it is great to have a strong dividend yield, we should also consider whether the payment is sustainable. Before this announcement, StrongPoint was paying out 89% of earnings, but a comparatively small 14% of free cash flows. In general, cash flows are more important than earnings, so we are comfortable that the dividend will be sustainable going forward, especially with so much cash left over for reinvestment.

Looking forward, earnings per share is forecast to rise by 92.9% over the next year. Under the assumption that the dividend will continue along recent trends, we think the payout ratio could be 57% which would be quite comfortable going to take the dividend forward.

StrongPoint Has A Solid Track Record

The company has an extended history of paying stable dividends. Since 2012, the first annual payment was kr0.25, compared to the most recent full-year payment of kr0.70. This means that it has been growing its distributions at 11% per annum over that time. We can see that payments have shown some very nice upward momentum without faltering, which provides some reassurance that future payments will also be reliable.

The Dividend Has Limited Growth Potential

Investors could be attracted to the stock based on the quality of its payment history. However, things aren't all that rosy. StrongPoint's earnings per share has shrunk at 14% a year over the past five years. Such rapid declines definitely have the potential to constrain dividend payments if the trend continues into the future. Over the next year, however, earnings are actually predicted to rise, but we would still be cautious until a track record of earnings growth can be built.

In Summary

In summary, while it's always good to see the dividend being raised, we don't think StrongPoint's payments are rock solid. The company is generating plenty of cash, but we still think the dividend is a bit high for comfort. This company is not in the top tier of income providing stocks.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. As an example, we've identified 1 warning sign for StrongPoint that you should be aware of before investing. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OB:STRO

StrongPoint

Engages in the development, sale, and implementation of integrated technology solutions to retailers in Scandinavia and internationally.

Good value with reasonable growth potential.

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Nevgold ·

The U.S. Government Is Desperate for This Metal. This Tiny Miner Has It -- Its Closest Peer Is Already Worth Double.

Fair Value:US$2.1946.6% undervalued

38 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6513.0% undervalued

61 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

JD

JD009 on Celsius Holdings ·

From $5M to $2B: Why the 2024 Crash Was the Best Buying Opportunity in Consumer Stocks

Fair Value:US$55.4347.7% undervalued

22 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

WA

Wavefarer on Accenture ·

High-quality global services company facing an AI-driven valuation reset.

Fair Value:US$30152.3% undervalued

16 followersusers have followed this narrative

1 commentusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

RO

Robbo on Microsoft ·

Is Microsoft on sale? and Its Case in the AI Race

Fair Value:US$4042.5% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AnimalDoctorKwon on Ultragenyx Pharmaceutical ·

burns cash despite four approved drugs, trapped by structural inefficiencies and gene-therapy scaling hurdles that thin safety margins.

Fair Value:US$2612.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AnimalDoctorKwon on BridgeBio Pharma ·

Faces a brutal commercial dogfight against Pfizer’s entrenched monopoly and Alnylam’s silencers, compressing its safety margins

Fair Value:US$25225.5% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75027.5% undervalued

96 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5458.4% undervalued

64 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6513.0% undervalued

61 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Trending Discussion

BE

benjamin_lvieq on PayPal Holdings ·

An investment case is not about loving the product. Its about price vs reality.

2

|0

ST

StoxEurope on Koninklijke Ahold Delhaize ·

I ran Ahold Delhaize through a three-model triangulation — DCF, dividend discount, and residual inco...

1

|0