Advertisement

Does Q-Free's (OB:QFR) CEO Salary Compare Well With Industry Peers?

Håkon Volldal became the CEO of Q-Free ASA (OB:QFR) in 2016, and we think it's a good time to look at the executive's compensation against the backdrop of overall company performance. This analysis will also assess whether Q-Free pays its CEO appropriately, considering recent earnings growth and total shareholder returns.

View our latest analysis for Q-Free

How Does Total Compensation For Håkon Volldal Compare With Other Companies In The Industry?

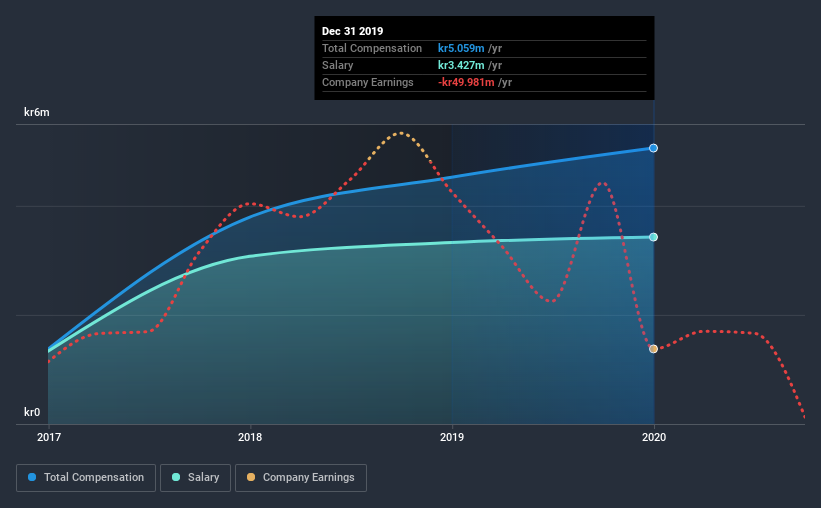

Our data indicates that Q-Free ASA has a market capitalization of kr446m, and total annual CEO compensation was reported as kr5.1m for the year to December 2019. That's a notable increase of 12% on last year. Notably, the salary which is kr3.43m, represents most of the total compensation being paid.

In comparison with other companies in the industry with market capitalizations under kr1.8b, the reported median total CEO compensation was kr5.1m. From this we gather that Håkon Volldal is paid around the median for CEOs in the industry. Furthermore, Håkon Volldal directly owns kr1.1m worth of shares in the company.

| Component | 2019 | 2018 | Proportion (2019) |

| Salary | kr3.4m | kr3.3m | 68% |

| Other | kr1.6m | kr1.2m | 32% |

| Total Compensation | kr5.1m | kr4.5m | 100% |

Speaking on an industry level, nearly 40% of total compensation represents salary, while the remainder of 60% is other remuneration. Q-Free is paying a higher share of its remuneration through a salary in comparison to the overall industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at Q-Free ASA's Growth Numbers

Q-Free ASA has reduced its earnings per share by 62% a year over the last three years. In the last year, its revenue is down 8.1%.

Overall this is not a very positive result for shareholders. And the fact that revenue is down year on year arguably paints an ugly picture. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Q-Free ASA Been A Good Investment?

Since shareholders would have lost about 37% over three years, some Q-Free ASA investors would surely be feeling negative emotions. This suggests it would be unwise for the company to pay the CEO too generously.

To Conclude...

As previously discussed, Håkon is compensated close to the median for companies of its size, and which belong to the same industry. Meanwhile, EPS growth and shareholder returns have been in the red for the last three years. Considering overall performance, shareholders will likely hold off support for a raise until results improve.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. We've identified 1 warning sign for Q-Free that investors should be aware of in a dynamic business environment.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

If you decide to trade Q-Free, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Q-Free might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About OB:QFR

Q-Free

Q-Free ASA supplies intelligent transportation system products and solutions worldwide.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.6% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|25.6% undervalued

GM

Community Contributor