Norbit (OB:NORBT): Valuation Check After NOK 170m European Defence Contract Win

Reviewed by Simply Wall St

Norbit (OB:NORBT) just landed roughly NOK 170 million in contract manufacturing orders from a European defence and security client, with most deliveries slated for early 2026, giving investors fresh visibility into future revenue.

See our latest analysis for Norbit.

That backdrop helps explain why, despite a softer 90 day share price return of around negative 9 percent, Norbit still boasts an 84 percent year to date share price gain and a standout five year total shareholder return near 1,000 percent. This suggests momentum has paused rather than disappeared.

If this kind of contract driven growth story appeals, it could be worth scanning aerospace and defense stocks to spot other defence focused names that might be building similar long term trajectories.

With revenue and earnings still growing double digits, the share price well off recent highs, and analysts seeing upside from here, the key question is whether Norbit remains undervalued or if the market is already pricing in further growth.

Most Popular Narrative Narrative: 25.8% Undervalued

With Norbit last closing at NOK178.20 against a narrative fair value of NOK240.00, the story leans firmly toward a still discounted future.

Significant revenue growth is expected to continue, supported by rapid adoption of Norbit's proprietary sonar and IoT solutions in industrial, maritime, and defense markets fueled by global digitalization and automation trends. This should directly raise top-line growth and, with product mix improvements, support stable or improving gross margins.

Curious how fast growing sonar and IoT demand, rising margins, and a lower future earnings multiple can still justify a sharply higher price? Read on.

Result: Fair Value of $240 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, heavy R&D and capacity spending, along with dependence on a few large defense projects, could squeeze cash flow and derail that bullish earnings path.

Find out about the key risks to this Norbit narrative.

Another Angle on Valuation

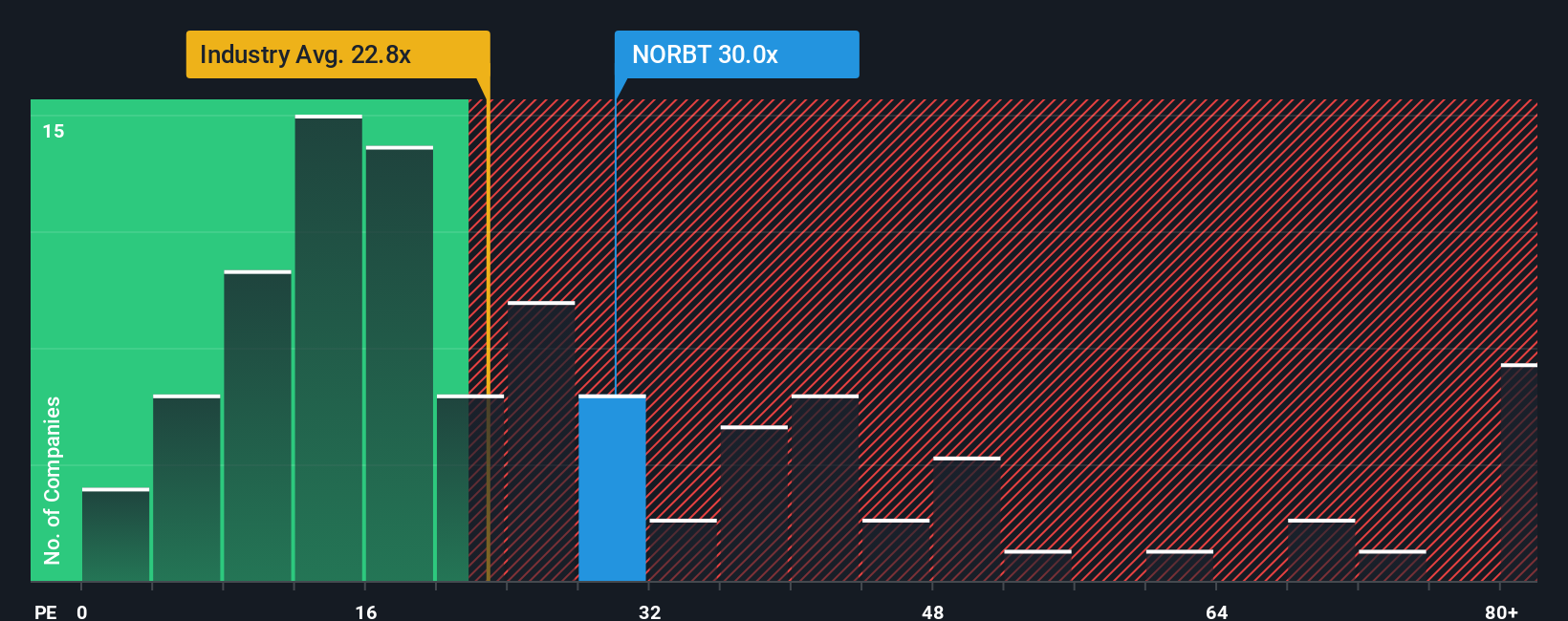

There is a catch: Norbit trades on about 30 times earnings versus 22.8 times for the wider European electronics group, even though our fair ratio suggests the market could comfortably justify 33.3 times. That premium leaves less room for error if growth stumbles.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Norbit Narrative

If you see the story differently or want to dig into the numbers yourself, you can build a personalized view in just minutes using Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Norbit.

Ready for more investment ideas?

Before you move on, consider using our screeners to uncover focused stock ideas that match your strategy and time horizon.

- Explore potential turnarounds by checking out these 913 undervalued stocks based on cash flows that the market may be overlooking despite solid underlying cash flows.

- Target cutting edge innovation with these 24 AI penny stocks positioned at the front line of artificial intelligence adoption and monetization.

- Strengthen your income stream through these 12 dividend stocks with yields > 3% that offer attractive yields alongside sustainable payout profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Norbit might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OB:NORBT

Norbit

Provides technology solutions to customers in a range of industries.

Outstanding track record with high growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion