Advertisement

- Norway

- /

- Communications

- /

- OB:HDLY

We're Interested To See How Huddly (OB:HDLY) Uses Its Cash Hoard To Grow

We can readily understand why investors are attracted to unprofitable companies. For example, although software-as-a-service business Salesforce.com lost money for years while it grew recurring revenue, if you held shares since 2005, you'd have done very well indeed. But while history lauds those rare successes, those that fail are often forgotten; who remembers Pets.com?

So should Huddly (OB:HDLY) shareholders be worried about its cash burn? For the purpose of this article, we'll define cash burn as the amount of cash the company is spending each year to fund its growth (also called its negative free cash flow). Let's start with an examination of the business' cash, relative to its cash burn.

View our latest analysis for Huddly

When Might Huddly Run Out Of Money?

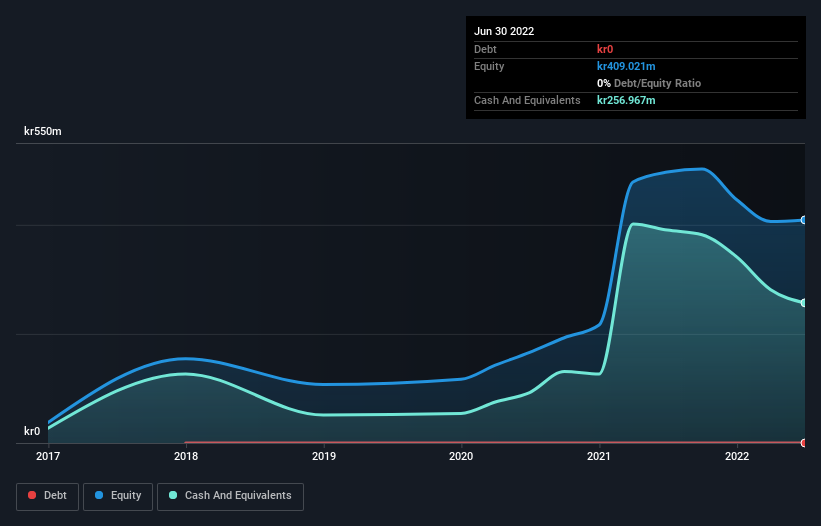

A cash runway is defined as the length of time it would take a company to run out of money if it kept spending at its current rate of cash burn. As at June 2022, Huddly had cash of kr257m and no debt. Importantly, its cash burn was kr78m over the trailing twelve months. So it had a cash runway of about 3.3 years from June 2022. There's no doubt that this is a reassuringly long runway. Depicted below, you can see how its cash holdings have changed over time.

Is Huddly's Revenue Growing?

We're hesitant to extrapolate on the recent trend to assess its cash burn, because Huddly actually had positive free cash flow last year, so operating revenue growth is probably our best bet to measure, right now. While it's not that amazing, we still think that the 15% increase in revenue from operations was a positive. Clearly, however, the crucial factor is whether the company will grow its business going forward. So you might want to take a peek at how much the company is expected to grow in the next few years.

How Hard Would It Be For Huddly To Raise More Cash For Growth?

Notwithstanding Huddly's revenue growth, it is still important to consider how it could raise more money, if it needs to. Companies can raise capital through either debt or equity. Many companies end up issuing new shares to fund future growth. We can compare a company's cash burn to its market capitalisation to get a sense for how many new shares a company would have to issue to fund one year's operations.

Since it has a market capitalisation of kr1.1b, Huddly's kr78m in cash burn equates to about 7.1% of its market value. Given that is a rather small percentage, it would probably be really easy for the company to fund another year's growth by issuing some new shares to investors, or even by taking out a loan.

So, Should We Worry About Huddly's Cash Burn?

As you can probably tell by now, we're not too worried about Huddly's cash burn. In particular, we think its cash runway stands out as evidence that the company is well on top of its spending. And even though its revenue growth wasn't quite as impressive, it was still a positive. After taking into account the various metrics mentioned in this report, we're pretty comfortable with how the company is spending its cash, as it seems on track to meet its needs over the medium term. When you don't have traditional metrics like earnings per share and free cash flow to value a company, many are extra motivated to consider qualitative factors such as whether insiders are buying or selling shares. Please Note: Huddly insiders have been trading shares, according to our data. Click here to check whether insiders have been buying or selling.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of interesting companies, and this list of stocks growth stocks (according to analyst forecasts)

Valuation is complex, but we're here to simplify it.

Discover if Huddly might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OB:HDLY

Huddly

A technology company, creates tools for team collaboration in Europe, the Middle East, Africa, the Asia Pacific, and the Americas.

Excellent balance sheet with slight risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor