Advertisement

The Price Is Right For ArcticZymes Technologies ASA (OB:AZT) Even After Diving 28%

ArcticZymes Technologies ASA (OB:AZT) shareholders that were waiting for something to happen have been dealt a blow with a 28% share price drop in the last month. The drop over the last 30 days has capped off a tough year for shareholders, with the share price down 41% in that time.

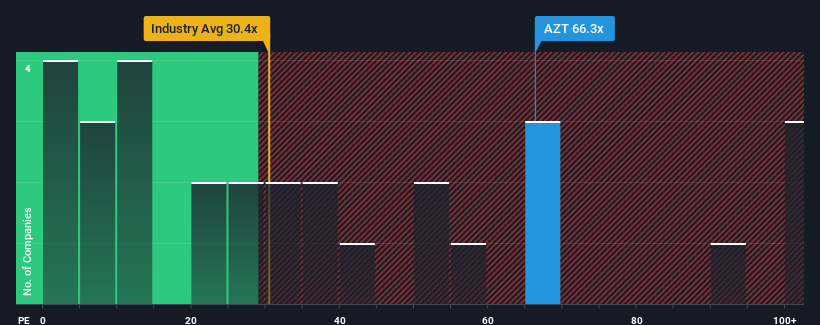

Even after such a large drop in price, ArcticZymes Technologies' price-to-earnings (or "P/E") ratio of 66.3x might still make it look like a strong sell right now compared to the market in Norway, where around half of the companies have P/E ratios below 11x and even P/E's below 7x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

ArcticZymes Technologies could be doing better as it's been growing earnings less than most other companies lately. It might be that many expect the uninspiring earnings performance to recover significantly, which has kept the P/E from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Check out our latest analysis for ArcticZymes Technologies

Is There Enough Growth For ArcticZymes Technologies?

There's an inherent assumption that a company should far outperform the market for P/E ratios like ArcticZymes Technologies' to be considered reasonable.

If we review the last year of earnings, the company posted a result that saw barely any deviation from a year ago. Whilst it's an improvement, it wasn't enough to get the company out of the hole it was in, with earnings down 79% overall from three years ago. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Turning to the outlook, the next three years should generate growth of 56% per year as estimated by the two analysts watching the company. That's shaping up to be materially higher than the 24% per annum growth forecast for the broader market.

With this information, we can see why ArcticZymes Technologies is trading at such a high P/E compared to the market. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

What We Can Learn From ArcticZymes Technologies' P/E?

Even after such a strong price drop, ArcticZymes Technologies' P/E still exceeds the rest of the market significantly. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that ArcticZymes Technologies maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. It's hard to see the share price falling strongly in the near future under these circumstances.

You need to take note of risks, for example - ArcticZymes Technologies has 2 warning signs (and 1 which can't be ignored) we think you should know about.

Of course, you might also be able to find a better stock than ArcticZymes Technologies. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OB:AZT

ArcticZymes Technologies

A life sciences company, develops, manufactures, and commercializes recombinant enzymes for use in molecular research, in vitro diagnostics, and biomanufacturing in Norway, Germany, Lithuania, France, Italy, the United Kingdom, rest of Europe, the United States, and internationally.

Flawless balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|32.0% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|21.7% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|0.5% overvalued

DA

Community Contributor