Advertisement

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Petrolia SE (OB:PSE) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Petrolia

What Is Petrolia's Debt?

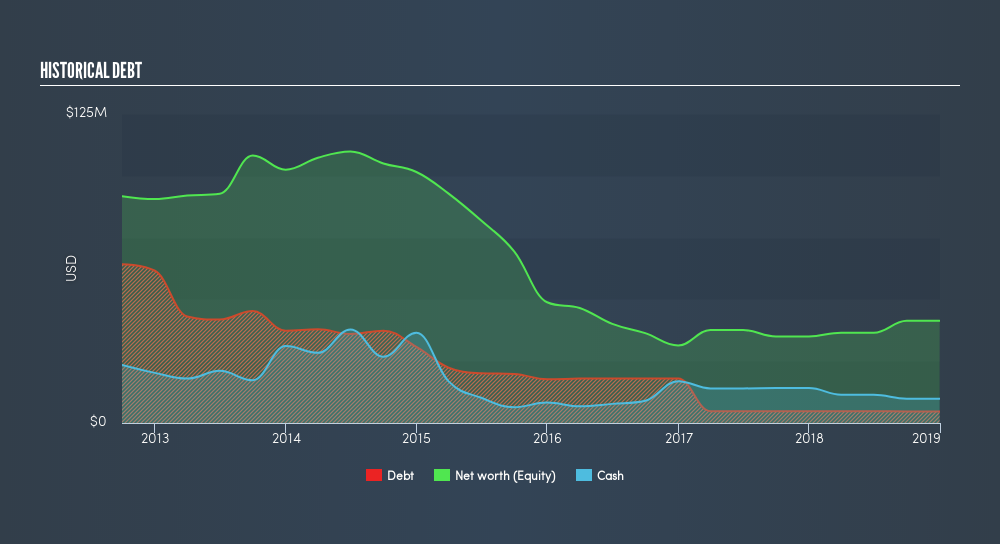

You can click the graphic below for the historical numbers, but it shows that Petrolia had US$4.70m of debt in December 2018, down from US$7.82m, one year before. However, it does have US$9.85m in cash offsetting this, leading to net cash of US$5.15m.

A Look At Petrolia's Liabilities

We can see from the most recent balance sheet that Petrolia had liabilities of US$15.2m falling due within a year, and liabilities of US$5.62m due beyond that. Offsetting these obligations, it had cash of US$9.85m as well as receivables valued at US$15.9m due within 12 months. So it actually has US$4.92m more liquid assets than total liabilities.

This excess liquidity suggests that Petrolia is taking a careful approach to debt. Because it has plenty of assets, it is unlikely to have trouble with its lenders. Succinctly put, Petrolia boasts net cash, so it's fair to say it does not have a heavy debt load!

It was also good to see that despite losing money on the EBIT line last year, Petrolia turned things around in the last 12 months, delivering and EBIT of US$5.5m. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Petrolia will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. While Petrolia has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Looking at the most recent year, Petrolia recorded free cash flow of 28% of its EBIT, which is weaker than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Summing up

While it is always sensible to investigate a company's debt, in this case Petrolia has US$5.1m in net cash and a decent-looking balance sheet. So we don't have any problem with Petrolia's use of debt. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all. If you've also come to that realization, you're in luck, because today you can view this interactive graph of Petrolia's earnings per share history for free.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About OB:PSE

Petrolia

Engages in the rental and sale of energy service equipment to energy industry in Norway, rest of Europe, Asia, and Australia.

Flawless balance sheet with solid track record.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|31.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|24.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|13.5% overvalued

DA

Community Contributor