Advertisement

- Norway

- /

- Renewable Energy

- /

- OB:MGN

Bullish: Analysts Just Made A Massive Upgrade To Their Magnora ASA (OB:MGN) Forecasts

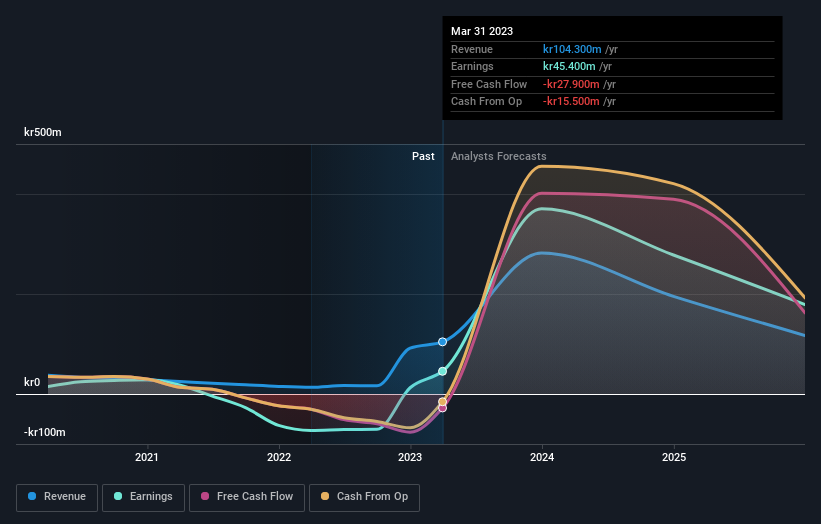

Magnora ASA (OB:MGN) shareholders will have a reason to smile today, with the analysts making substantial upgrades to this year's forecasts. Consensus estimates suggest investors could expect greatly increased statutory revenues and earnings per share, with the analysts modelling a real improvement in business performance.

After the upgrade, the three analysts covering Magnora are now predicting revenues of kr282m in 2023. If met, this would reflect a major 171% improvement in sales compared to the last 12 months. Statutory earnings per share are presumed to jump 710% to kr5.59. Previously, the analysts had been modelling revenues of kr213m and earnings per share (EPS) of kr3.96 in 2023. There has definitely been an improvement in perception recently, with the analysts substantially increasing both their earnings and revenue estimates.

See our latest analysis for Magnora

Although the analysts have upgraded their earnings estimates, there was no change to the consensus price target of US$3.99, suggesting that the forecast performance does not have a long term impact on the company's valuation. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. There are some variant perceptions on Magnora, with the most bullish analyst valuing it at US$4.42 and the most bearish at US$3.71 per share. This is a very narrow spread of estimates, implying either that Magnora is an easy company to value, or - more likely - the analysts are relying heavily on some key assumptions.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. For example, we noticed that Magnora's rate of growth is expected to accelerate meaningfully, with revenues forecast to exhibit 277% growth to the end of 2023 on an annualised basis. That is well above its historical decline of 1.1% a year over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in the industry are forecast to see their revenue grow 11% per year. Not only are Magnora's revenues expected to improve, it seems that the analysts are also expecting it to grow faster than the wider industry.

The Bottom Line

The most important thing to take away from this upgrade is that analysts upgraded their earnings per share estimates for this year, expecting improving business conditions. Fortunately, analysts also upgraded their revenue estimates, and our data indicates sales are expected to perform better than the wider market. Some investors might be disappointed to see that the price target is unchanged, but we feel that improving fundamentals are usually a positive - assuming these forecasts are met! So Magnora could be a good candidate for more research.

These earnings upgrades look like a sterling endorsement, but before diving in - you should know that we've spotted 2 potential flag with Magnora, including dilutive stock issuance over the past year. You can learn more, and discover the 1 other flag we've identified, for free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OB:MGN

Magnora

Operates as a renewable energy development company in Norway, Sweden, South Africa and the United Kingdom.

Exceptional growth potential with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor