- Norway

- /

- Energy Services

- /

- OB:EMGS

Health Check: How Prudently Does Electromagnetic Geoservices (OB:EMGS) Use Debt?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Electromagnetic Geoservices ASA (OB:EMGS) makes use of debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Electromagnetic Geoservices

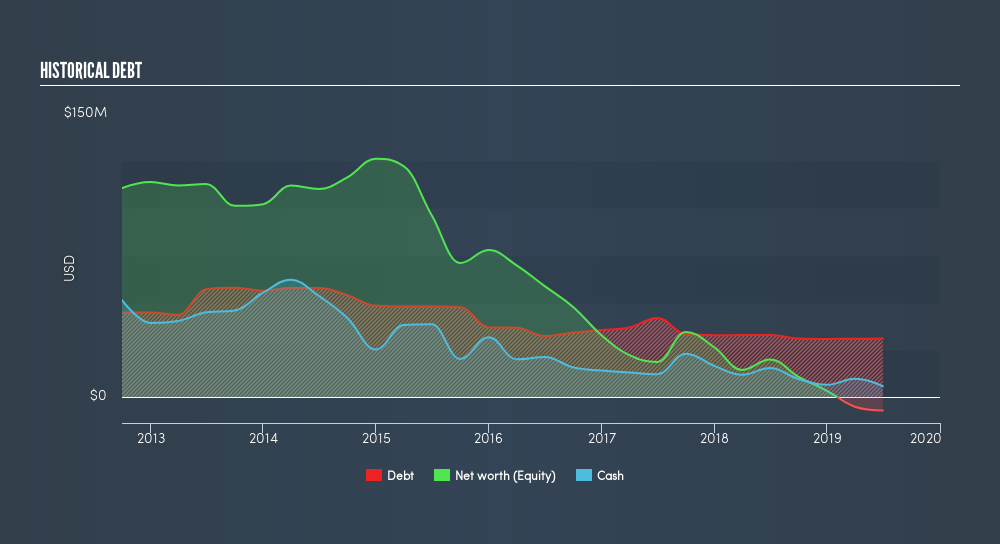

How Much Debt Does Electromagnetic Geoservices Carry?

As you can see below, Electromagnetic Geoservices had US$31.0m of debt at June 2019, down from US$33.1m a year prior. However, because it has a cash reserve of US$5.78m, its net debt is less, at about US$25.2m.

How Strong Is Electromagnetic Geoservices's Balance Sheet?

The latest balance sheet data shows that Electromagnetic Geoservices had liabilities of US$35.2m due within a year, and liabilities of US$61.9m falling due after that. Offsetting these obligations, it had cash of US$5.78m as well as receivables valued at US$13.6m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$77.7m.

This deficit casts a shadow over the US$32.1m company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. After all, Electromagnetic Geoservices would likely require a major re-capitalisation if it had to pay its creditors today. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Electromagnetic Geoservices can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year Electromagnetic Geoservices managed to grow its revenue by 33%, to US$45m. With any luck the company will be able to grow its way to profitability.

Caveat Emptor

Despite the top line growth, Electromagnetic Geoservices still had negative earnings before interest and tax (EBIT), over the last year. Its EBIT loss was a whopping US$17m. Considering that alongside the liabilities mentioned above make us nervous about the company. We'd want to see some strong near-term improvements before getting too interested in the stock. Not least because it burned through US$542k in negative free cash flow over the last year. That means it's on the risky side of things. When we look at a riskier company, we like to check how their profits (or losses) are trending over time. Today, we're providing readers this interactive graph showing how Electromagnetic Geoservices's profit, revenue, and operating cashflow have changed over the last few years.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About OB:EMGS

Electromagnetic Geoservices

Provides electromagnetic (EM) surveying technology and services to the offshore oil and gas exploration industry.

Moderate risk and slightly overvalued.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion