Advertisement

Akastor ASA (OB:AKA) is a small-cap stock with a market capitalization of øre3.5b. While investors primarily focus on the growth potential and competitive landscape of the small-cap companies, they end up ignoring a key aspect, which could be the biggest threat to its existence: its financial health. Why is it important? Given that AKA is not presently profitable, it’s essential to evaluate the current state of its operations and pathway to profitability. The following basic checks can help you get a picture of the company's balance sheet strength. However, these checks don't give you a full picture, so I recommend you dig deeper yourself into AKA here.

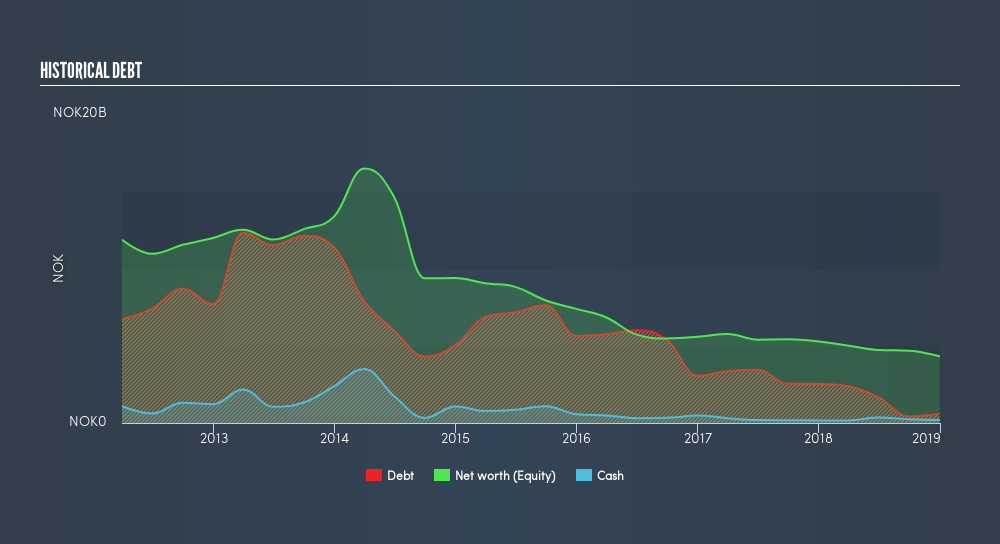

Does AKA Produce Much Cash Relative To Its Debt?

AKA has shrunk its total debt levels in the last twelve months, from øre2.5b to øre602m , which includes long-term debt. With this debt payback, AKA's cash and short-term investments stands at øre198m to keep the business going. Additionally, AKA has generated øre315m in operating cash flow during the same period of time, resulting in an operating cash to total debt ratio of 52%, indicating that AKA’s operating cash is sufficient to cover its debt.

Can AKA meet its short-term obligations with the cash in hand?

Looking at AKA’s øre3.2b in current liabilities, the company has been able to meet these obligations given the level of current assets of øre3.9b, with a current ratio of 1.23x. The current ratio is the number you get when you divide current assets by current liabilities. For Energy Services companies, this ratio is within a sensible range since there is a bit of a cash buffer without leaving too much capital in a low-return environment.

Is AKA’s debt level acceptable?

With a debt-to-equity ratio of 14%, AKA's debt level may be seen as prudent. This range is considered safe as AKA is not taking on too much debt obligation, which may be constraining for future growth. AKA's risk around capital structure is low, and the company has the headroom and ability to raise debt should it need to in the future.

Next Steps:

AKA’s high cash coverage and low debt levels indicate its ability to utilise its borrowings efficiently in order to generate ample cash flow. In addition to this, the company will be able to pay all of its upcoming liabilities from its current short-term assets. I admit this is a fairly basic analysis for AKA's financial health. Other important fundamentals need to be considered alongside. I recommend you continue to research Akastor to get a better picture of the stock by looking at:

- Future Outlook: What are well-informed industry analysts predicting for AKA’s future growth? Take a look at our free research report of analyst consensus for AKA’s outlook.

- Valuation: What is AKA worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether AKA is currently mispriced by the market.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About OB:AKAST

Akastor

Operates as an oilfield services investment company in Norway and internationally.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|33.3% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|23.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|8.5% overvalued

DA

Community Contributor