Stock Analysis

- Netherlands

- /

- Logistics

- /

- ENXTAM:PNL

Top Insider-Owned Growth Stocks On Euronext Amsterdam In July 2024

Reviewed by Simply Wall St

As European markets navigate through a period of political uncertainty and fluctuating bond yields, the Euronext Amsterdam stands out with its unique offerings. In this context, companies with high insider ownership can be particularly appealing, as they often signal strong confidence from those closest to the business in its growth prospects.

Top 5 Growth Companies With High Insider Ownership In The Netherlands

| Name | Insider Ownership | Earnings Growth |

| BenevolentAI (ENXTAM:BAI) | 27.8% | 62.8% |

| Envipco Holding (ENXTAM:ENVI) | 16% | 68.9% |

| Ebusco Holding (ENXTAM:EBUS) | 33.2% | 114.0% |

| MotorK (ENXTAM:MTRK) | 35.8% | 105.8% |

| Basic-Fit (ENXTAM:BFIT) | 12% | 66.1% |

| PostNL (ENXTAM:PNL) | 30.8% | 24% |

Here's a peek at a few of the choices from the screener.

Basic-Fit (ENXTAM:BFIT)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Basic-Fit N.V., along with its subsidiaries, operates fitness clubs and has a market capitalization of approximately €1.34 billion.

Operations: The company generates its revenues primarily from two segments: Benelux, which contributes approximately €479.04 million, and the combined regions of France, Spain, and Germany, which bring in about €568.21 million.

Insider Ownership: 12%

Earnings Growth Forecast: 66.1% p.a.

Basic-Fit, a prominent fitness chain in the Netherlands, demonstrates promising growth with insider confidence reflected through more buying than selling of shares recently, albeit in modest volumes. Analysts project a significant 63.8% potential increase in stock price from current levels. The company is expected to achieve profitability within three years, with revenue and earnings growth forecasts outpacing the broader Dutch market significantly at 14.9% and 66.07% per year respectively, alongside a robust projected Return on Equity of 26.7%.

- Click here and access our complete growth analysis report to understand the dynamics of Basic-Fit.

- Our expertly prepared valuation report Basic-Fit implies its share price may be too high.

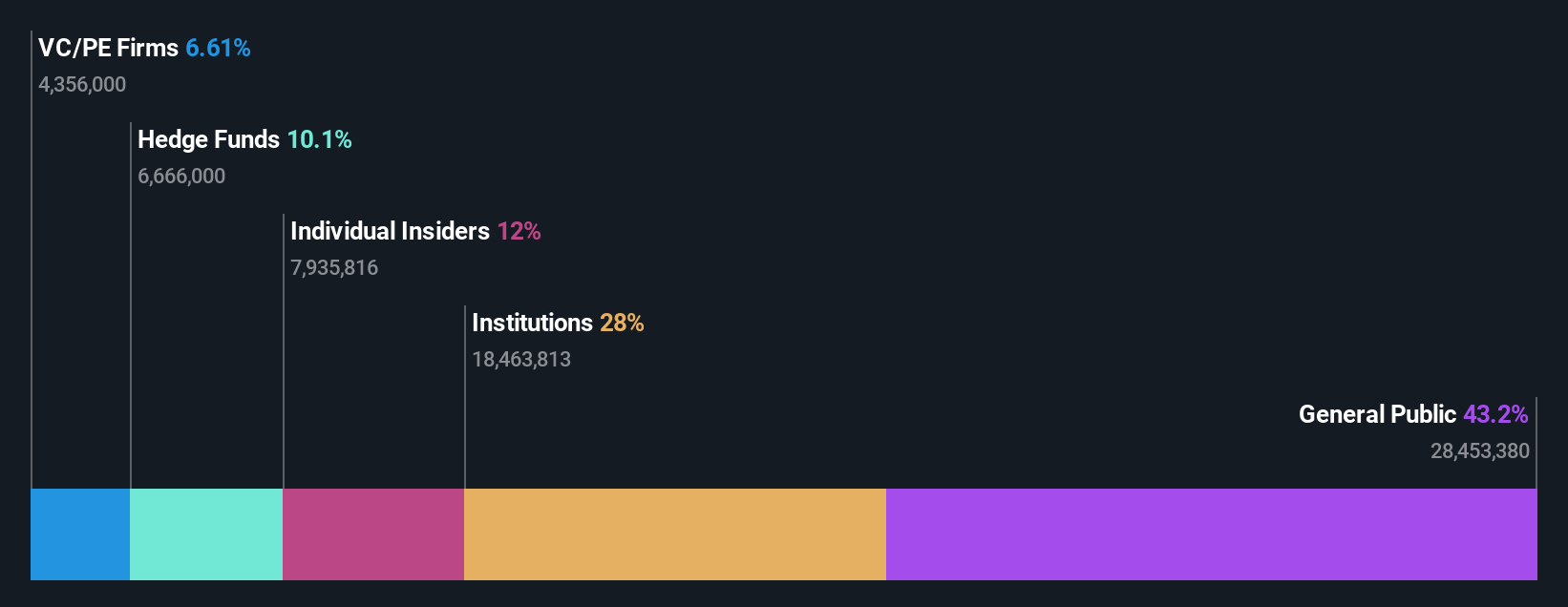

MotorK (ENXTAM:MTRK)

Simply Wall St Growth Rating: ★★★★★☆

Overview: MotorK plc operates as a provider of software-as-a-service solutions tailored for the automotive retail industry across Italy, Spain, France, Germany, and the Benelux Union, with a market capitalization of approximately €273.01 million.

Operations: The company generates its revenue primarily from the Software & Programming segment, amounting to €42.94 million.

Insider Ownership: 35.8%

Earnings Growth Forecast: 105.8% p.a.

MotorK, despite recent executive changes, including the appointment of Helen Protopapas and the resignation of Mauro Pretolani, has shown resilience with a slight revenue dip in Q1 2024 to €11.25 million from €11.43 million year-over-year. The company is not currently profitable but is expected to reverse this trend within three years, with anticipated earnings growth of 105.85% per year and revenue growth projected at 24% annually, significantly outpacing the Dutch market average.

- Get an in-depth perspective on MotorK's performance by reading our analyst estimates report here.

- The analysis detailed in our MotorK valuation report hints at an inflated share price compared to its estimated value.

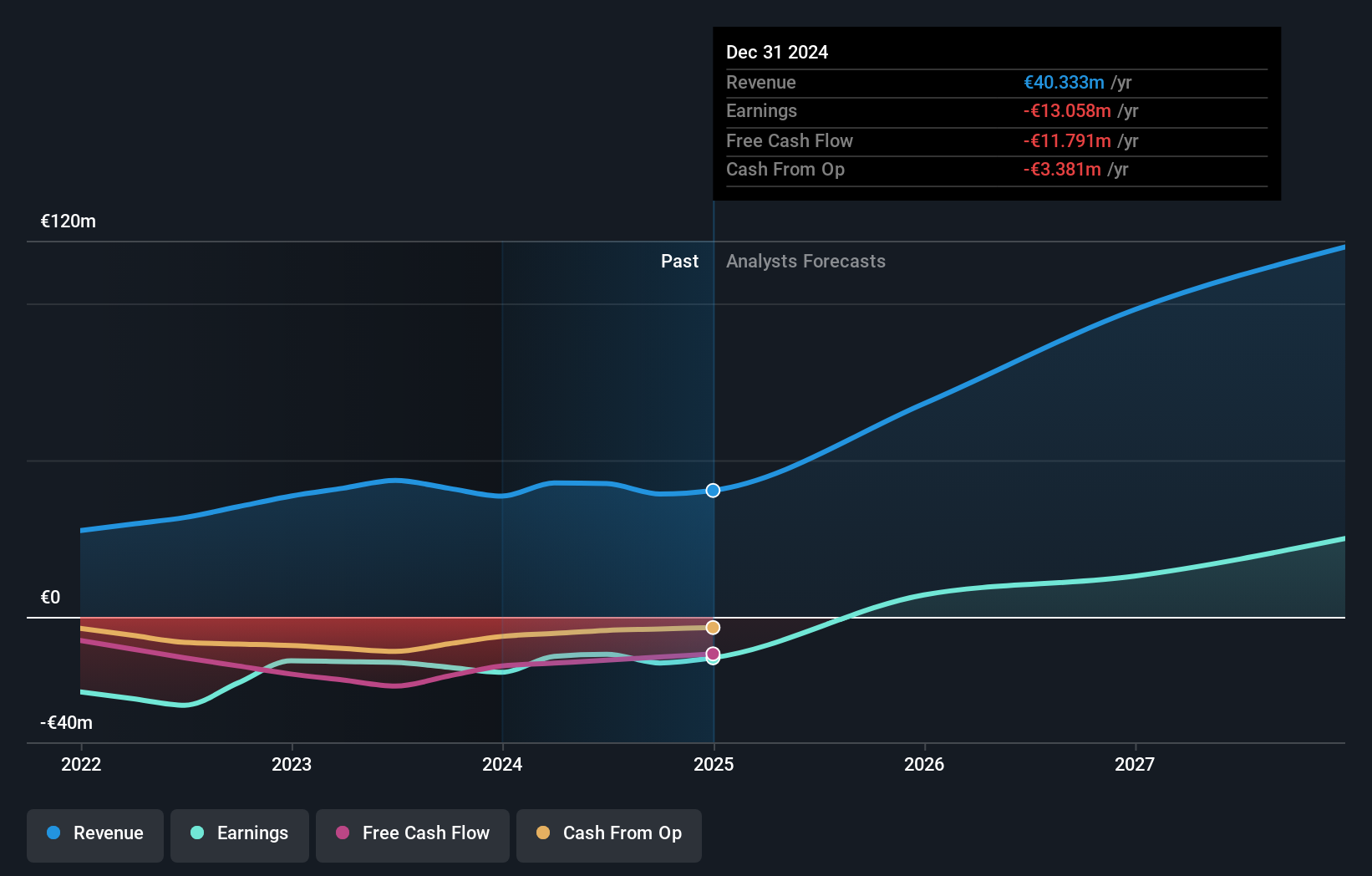

PostNL (ENXTAM:PNL)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: PostNL N.V. offers postal and logistics services across the Netherlands, Europe, and globally, with a market capitalization of approximately €0.64 billion.

Operations: PostNL's revenue is primarily generated from its Packages and Mail in The Netherlands segments, which respectively brought in €2.25 billion and €1.35 billion.

Insider Ownership: 30.8%

Earnings Growth Forecast: 24% p.a.

PostNL, despite a highly volatile share price and an unstable dividend track record, shows potential with earnings forecasted to grow by 24% annually, outpacing the Dutch market's 18%. However, its revenue growth lags behind at 3.3% annually compared to the market's 9.8%. The company recently completed a €298.67 million sustainability-linked bond offering but reported a net loss of €20 million in Q1 2024. Trading significantly below fair value, PostNL faces challenges but has growth prospects with expected high return on equity in three years.

- Navigate through the intricacies of PostNL with our comprehensive analyst estimates report here.

- In light of our recent valuation report, it seems possible that PostNL is trading behind its estimated value.

Summing It All Up

- Click this link to deep-dive into the 6 companies within our Fast Growing Euronext Amsterdam Companies With High Insider Ownership screener.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're helping make it simple.

Find out whether PostNL is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTAM:PNL

PostNL

Provides postal and logistics services to businesses and consumers in the Netherlands, rest of Europe, and internationally.

Good value with reasonable growth potential and pays a dividend.