Stock Analysis

- Netherlands

- /

- Hospitality

- /

- ENXTAM:BFIT

Euronext Amsterdam Growth Companies With High Insider Ownership And 27% Return On Equity

Reviewed by Simply Wall St

Amid a backdrop of fluctuating global markets, the Netherlands continues to present intriguing investment opportunities, particularly in growth companies with high insider ownership. These firms not only demonstrate robust confidence from those closest to the business but also align well with current market conditions that favor entities with solid internal commitment and promising financial metrics like a 27% return on equity.

Top 5 Growth Companies With High Insider Ownership In The Netherlands

| Name | Insider Ownership | Earnings Growth |

| Envipco Holding (ENXTAM:ENVI) | 15.1% | 62.7% |

| Ebusco Holding (ENXTAM:EBUS) | 32.6% | 122.5% |

| MotorK (ENXTAM:MTRK) | 39.1% | 105.8% |

| Basic-Fit (ENXTAM:BFIT) | 12% | 66.1% |

| PostNL (ENXTAM:PNL) | 31.1% | 33.6% |

Underneath we present a selection of stocks filtered out by our screen.

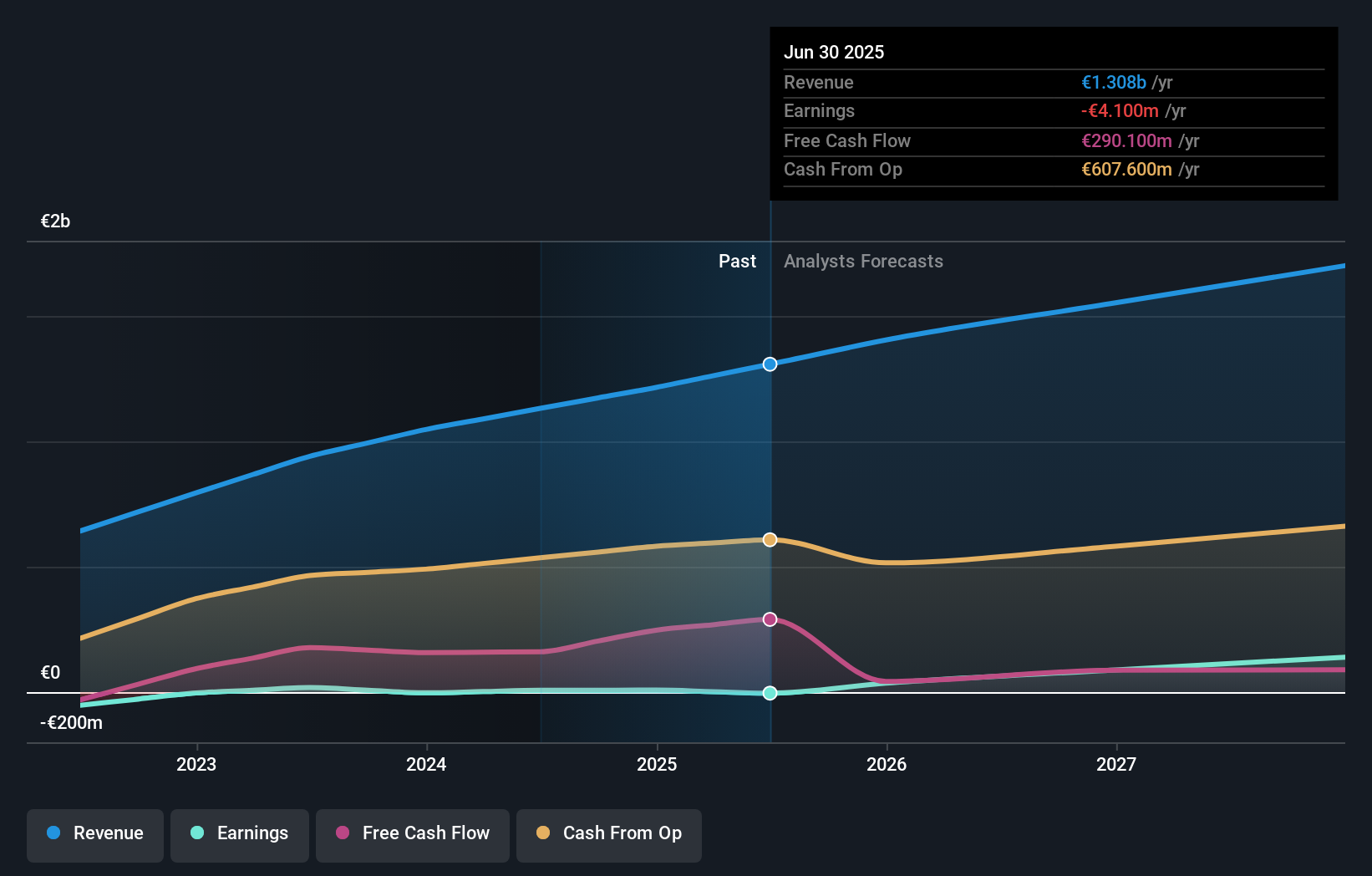

Basic-Fit (ENXTAM:BFIT)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Basic-Fit N.V. operates a chain of fitness clubs across Europe, with a market capitalization of approximately €1.48 billion.

Operations: The company generates its revenues primarily from two segments: Benelux at €479.04 million and France, Spain & Germany at €568.21 million.

Insider Ownership: 12%

Return On Equity Forecast: 25% (2026 estimate)

Basic-Fit, a Dutch fitness chain, is anticipated to see significant growth with revenue expected to increase by 15% annually, outpacing the national average of 9.2%. The company is projected to turn profitable within three years, with earnings potentially growing at an annual rate of 66.07%. Insiders have been net buyers of shares recently, though not in large volumes. Despite this insider confidence and strong growth forecasts, the stock has experienced high volatility recently. Analysts remain optimistic, predicting a potential price increase of 52.1%.

- Click here to discover the nuances of Basic-Fit with our detailed analytical future growth report.

- Our valuation report here indicates Basic-Fit may be overvalued.

Envipco Holding (ENXTAM:ENVI)

Simply Wall St Growth Rating: ★★★★★★

Overview: Envipco Holding N.V. specializes in designing, developing, manufacturing, and selling or leasing reverse vending machines for recycling used beverage containers, primarily serving markets in the Netherlands, North America, and Europe with a market capitalization of approximately €340.37 million.

Operations: The company generates its revenue by designing, developing, manufacturing, and marketing reverse vending machines for recycling used beverage containers across the Netherlands, North America, and Europe.

Insider Ownership: 15.1%

Return On Equity Forecast: 26% (2026 estimate)

Envipco Holding N.V. has shown promising growth, turning profitable this year with earnings expected to rise by 62.66% annually, outperforming the Dutch market's 15.9%. Revenue forecasts also surpass market expectations at a 33% annual increase. Despite recent share price volatility and shareholder dilution over the past year, the company's value is considered significantly below its fair value. Additionally, Envipco completed a €300 million follow-on equity offering recently, signaling potential for expansion and investment.

- Dive into the specifics of Envipco Holding here with our thorough growth forecast report.

- Our valuation report unveils the possibility Envipco Holding's shares may be trading at a discount.

PostNL (ENXTAM:PNL)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: PostNL N.V. offers postal and logistics services across the Netherlands, Europe, and globally, with a market capitalization of approximately €0.63 billion.

Operations: The company generates revenue primarily from packages and mail services in the Netherlands, with segments reporting €2.25 billion and €1.35 billion respectively.

Insider Ownership: 31.1%

Return On Equity Forecast: 27% (2027 estimate)

PostNL N.V. has recently transitioned from a net loss to profitability, with an encouraging outlook as earnings are anticipated to grow by 33.58% annually. Despite a recent quarterly performance dip, with sales and profits down from the previous year, the company maintains a strong forecast for profit growth that significantly exceeds average market expectations. However, it faces challenges such as high debt levels and slower revenue growth compared to the market, alongside no significant insider buying or selling in recent months.

- Take a closer look at PostNL's potential here in our earnings growth report.

- Upon reviewing our latest valuation report, PostNL's share price might be too pessimistic.

Where To Now?

- Click here to access our complete index of 5 Fast Growing Euronext Amsterdam Companies With High Insider Ownership.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're helping make it simple.

Find out whether Basic-Fit is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTAM:BFIT

High growth potential with imperfect balance sheet.