- Netherlands

- /

- Machinery

- /

- ENXTAM:ENVI

Euronext Amsterdam's Top Growth Companies With High Insider Ownership August 2024

Reviewed by Simply Wall St

As the European markets navigate mixed earnings reports and economic indicators, investors are increasingly focusing on growth opportunities within stable economies like the Netherlands. In this context, identifying companies with high insider ownership can be particularly insightful, as it often signals strong confidence from those who know the business best. In today's article, we explore three standout growth companies listed on Euronext Amsterdam that boast significant insider ownership—a factor that may offer added assurance amid fluctuating market conditions.

Top 5 Growth Companies With High Insider Ownership In The Netherlands

| Name | Insider Ownership | Earnings Growth |

| BenevolentAI (ENXTAM:BAI) | 27.8% | 62.8% |

| Ebusco Holding (ENXTAM:EBUS) | 33.2% | 113.8% |

| Envipco Holding (ENXTAM:ENVI) | 36.7% | 68.9% |

| Basic-Fit (ENXTAM:BFIT) | 12% | 78.3% |

| MotorK (ENXTAM:MTRK) | 35.8% | 108.4% |

| PostNL (ENXTAM:PNL) | 35.8% | 23.9% |

Let's review some notable picks from our screened stocks.

Basic-Fit (ENXTAM:BFIT)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Basic-Fit N.V., with a market cap of €1.45 billion, operates fitness clubs through its subsidiaries.

Operations: Revenue from Basic-Fit N.V.'s fitness clubs is divided into €505.17 million from Benelux and €626.41 million from France, Spain, and Germany.

Insider Ownership: 12%

Revenue Growth Forecast: 15.1% p.a.

Basic-Fit shows promising growth potential with earnings forecasted to grow significantly at 78.3% per year, outpacing the Dutch market's 18.9%. Revenue is expected to rise by 15.1% annually, faster than the market average of 10%. Despite recent volatility, insider ownership remains strong with more shares bought than sold in the past three months. Recent earnings reports highlight improved financial performance, transitioning from a net loss to a net income of €4.18 million for H1 2024.

- Click here to discover the nuances of Basic-Fit with our detailed analytical future growth report.

- The analysis detailed in our Basic-Fit valuation report hints at an inflated share price compared to its estimated value.

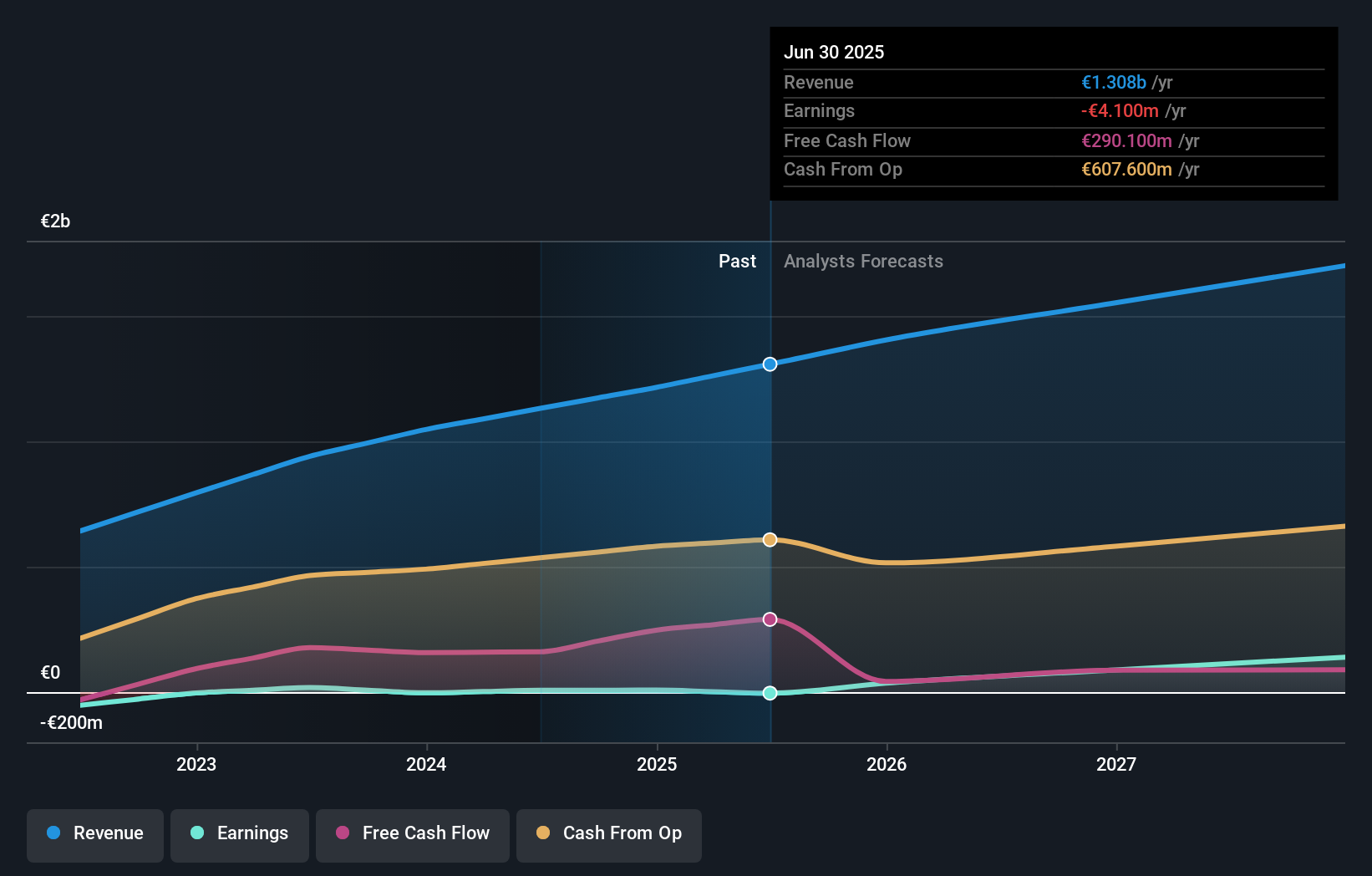

Envipco Holding (ENXTAM:ENVI)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Envipco Holding N.V. designs, manufactures, and services reverse vending machines for used beverage containers in the Netherlands, North America, and Europe with a market cap of €340.37 million.

Operations: Envipco Holding generates revenue by designing, developing, manufacturing, assembling, marketing, selling, leasing, and servicing reverse vending machines to collect and process used beverage containers primarily in the Netherlands, North America, and Europe.

Insider Ownership: 36.7%

Revenue Growth Forecast: 33.3% p.a.

Envipco Holding's revenue is forecast to grow 33.3% per year, significantly outpacing the Dutch market's 10%. Earnings are expected to rise by 68.9% annually, transitioning from a net loss to a net income of €0.147 million in Q1 2024. Trading at 22.7% below estimated fair value, it has seen more insider buying than selling recently despite high share price volatility and past shareholder dilution concerns.

- Dive into the specifics of Envipco Holding here with our thorough growth forecast report.

- Our valuation report unveils the possibility Envipco Holding's shares may be trading at a premium.

MotorK (ENXTAM:MTRK)

Simply Wall St Growth Rating: ★★★★★☆

Overview: MotorK plc, with a market cap of €271.71 million, offers software-as-a-service solutions to the automotive retail industry across Italy, Spain, France, Germany, and the Benelux Union.

Operations: MotorK plc generates revenue of €42.50 million from its Software & Programming segment, providing SaaS solutions to the automotive retail sector in several European countries.

Insider Ownership: 35.8%

Revenue Growth Forecast: 22.1% p.a.

MotorK is forecasted to achieve profitability within the next three years, with revenue expected to grow at 22.1% annually, outpacing the Dutch market's 10%. Despite a recent net loss of €6.48 million for H1 2024, down from €7.8 million last year, it shows promising earnings growth of 108.44% per year. Insider ownership remains high without significant insider trading in the past three months. Recent executive changes include appointing Zoltan Gelencser as CFO.

- Click to explore a detailed breakdown of our findings in MotorK's earnings growth report.

- Our comprehensive valuation report raises the possibility that MotorK is priced higher than what may be justified by its financials.

Make It Happen

- Explore the 6 names from our Fast Growing Euronext Amsterdam Companies With High Insider Ownership screener here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Envipco Holding might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTAM:ENVI

Envipco Holding

Designs, develops, manufactures, assembles, markets, sells, leases, and services reverse vending machines (RVM) to collect and process used beverage containers primarily in the Netherlands, North America, and rest of Europe.

High growth potential with excellent balance sheet.