- Netherlands

- /

- Hospitality

- /

- ENXTAM:BFIT

Euronext Amsterdam Growth Companies With High Insider Ownership And At Least 14% Revenue Growth

Reviewed by Simply Wall St

As global markets navigate through a phase of cautious optimism, the Netherlands market remains a focal point for investors seeking robust growth opportunities. Amidst this landscape, Euronext Amsterdam highlights several growth companies with high insider ownership and impressive revenue growth, signaling strong confidence from those closest to these enterprises.

Top 5 Growth Companies With High Insider Ownership In The Netherlands

| Name | Insider Ownership | Earnings Growth |

| BenevolentAI (ENXTAM:BAI) | 27.8% | 62.8% |

| Envipco Holding (ENXTAM:ENVI) | 26.8% | 68.9% |

| Ebusco Holding (ENXTAM:EBUS) | 33.2% | 114.0% |

| MotorK (ENXTAM:MTRK) | 35.8% | 105.8% |

| Basic-Fit (ENXTAM:BFIT) | 12% | 66.1% |

| PostNL (ENXTAM:PNL) | 35.8% | 23.9% |

Let's explore several standout options from the results in the screener.

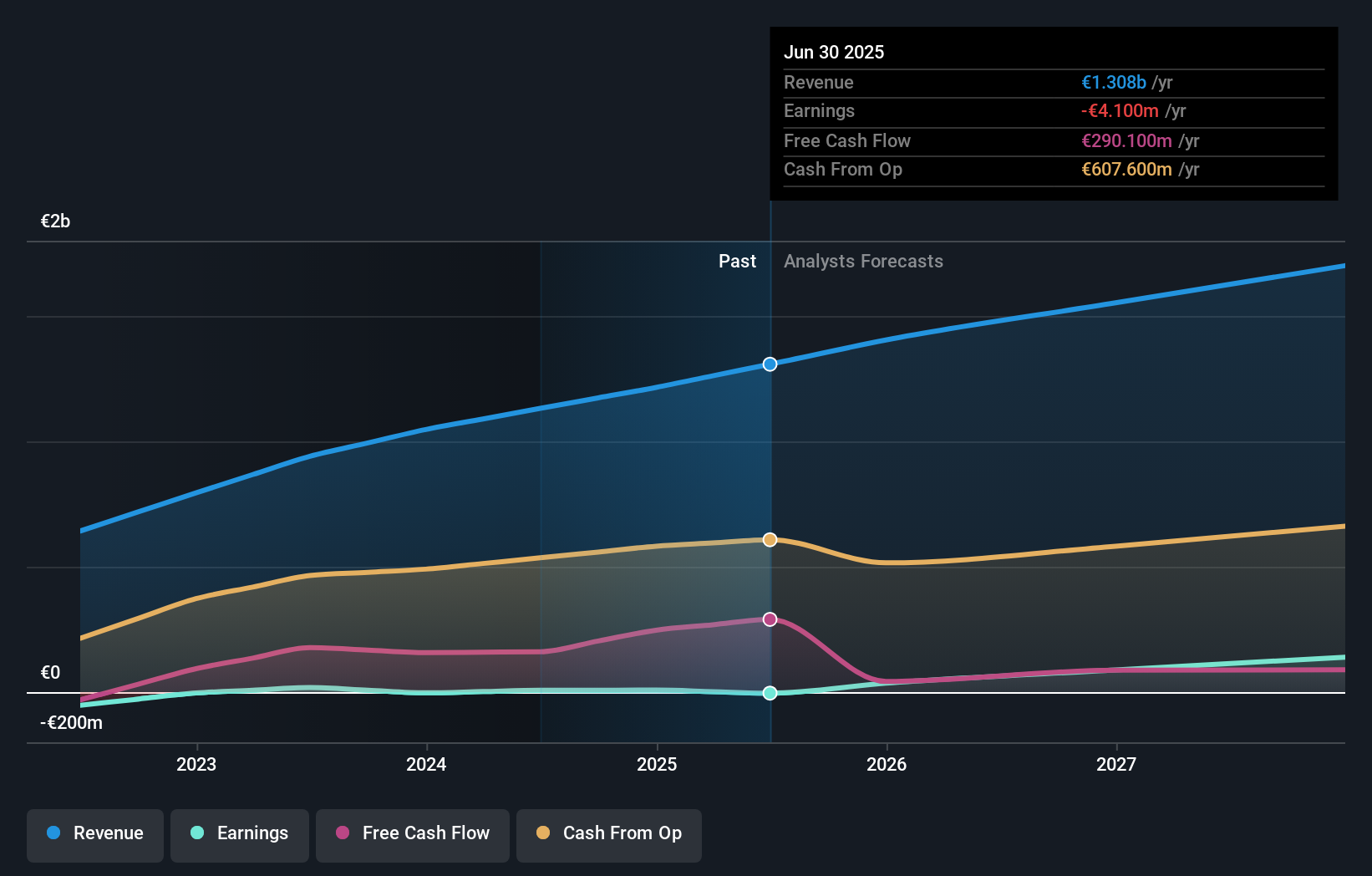

Basic-Fit (ENXTAM:BFIT)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Basic-Fit N.V. operates a chain of fitness clubs across Europe, with a market capitalization of approximately €1.40 billion.

Operations: The company generates its revenue from two primary geographical segments: Benelux at €479.04 million and France, Spain & Germany at €568.21 million.

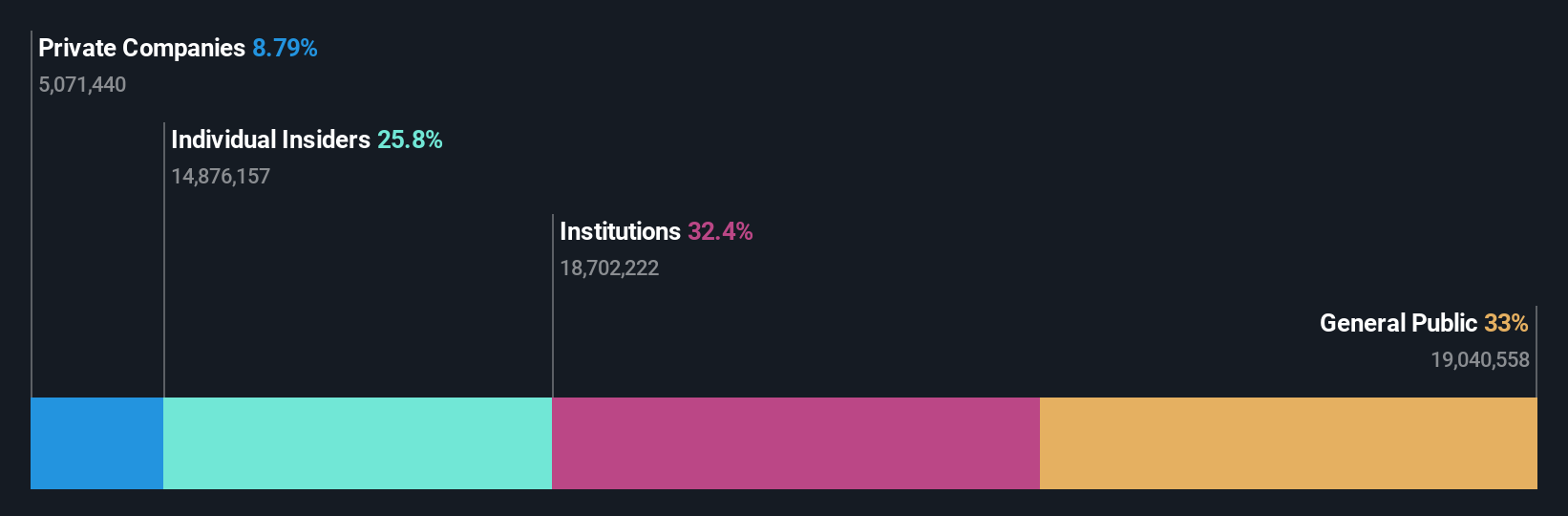

Insider Ownership: 12%

Revenue Growth Forecast: 14.9% p.a.

Basic-Fit, a prominent fitness club operator in the Netherlands, is expected to see significant growth with its revenue increasing at 14.9% annually, outpacing the Dutch market's 9.8%. Despite not reaching the top echelon for insider ownership growth companies, it shows promise with no substantial insider sales recently and modest insider buying over the past three months. Analysts predict a substantial price increase of 62%, and Basic-Fit is forecasted to become profitable within three years, supported by an anticipated high return on equity of 26.7%.

- Click here and access our complete growth analysis report to understand the dynamics of Basic-Fit.

- Insights from our recent valuation report point to the potential overvaluation of Basic-Fit shares in the market.

Envipco Holding (ENXTAM:ENVI)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Envipco Holding N.V. specializes in designing, developing, manufacturing, and selling or leasing reverse vending machines (RVMs) for recycling used beverage containers, primarily operating in the Netherlands, North America, and Europe with a market capitalization of €340.37 million.

Operations: The company generates revenue by designing, developing, manufacturing, and either selling or leasing reverse vending machines for recycling used beverage containers across the Netherlands, North America, and Europe.

Insider Ownership: 26.8%

Revenue Growth Forecast: 33.3% p.a.

Envipco Holding N.V. has shown notable growth, with its first-quarter sales jumping to €27.44 million from €10.41 million year-over-year, turning a previous net loss into a profit of €0.147 million. The company's revenue is expected to grow by 33.3% annually, outstripping the Dutch market forecast of 9.9%. Despite high share price volatility and recent shareholder dilution, insider transactions have been positive but not substantial in volume, with more buying than selling over the past three months.

- Click here to discover the nuances of Envipco Holding with our detailed analytical future growth report.

- Our expertly prepared valuation report Envipco Holding implies its share price may be too high.

MotorK (ENXTAM:MTRK)

Simply Wall St Growth Rating: ★★★★★☆

Overview: MotorK plc operates as a provider of software-as-a-service solutions for the automotive retail industry across Italy, Spain, France, Germany, and the Benelux Union, with a market capitalization of approximately €273.01 million.

Operations: The company generates its revenue primarily through its software and programming segment, which contributed €42.94 million.

Insider Ownership: 35.8%

Revenue Growth Forecast: 24% p.a.

MotorK, amidst a backdrop of executive changes including the recent appointment of Helen Protopapas as director, is poised for robust growth with expected annual revenue increases of 24%, outpacing the Dutch market's 9.9%. Although shareholder dilution occurred last year, earnings are projected to surge by over 100% annually. The firm reported a slight dip in Q1 revenue to €11.25 million from €11.43 million year-over-year but is on track to profitability within three years.

- Navigate through the intricacies of MotorK with our comprehensive analyst estimates report here.

- The analysis detailed in our MotorK valuation report hints at an inflated share price compared to its estimated value.

Turning Ideas Into Actions

- Investigate our full lineup of 6 Fast Growing Euronext Amsterdam Companies With High Insider Ownership right here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Basic-Fit might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTAM:BFIT

High growth potential low.