Advertisement

- Malaysia

- /

- Specialty Stores

- /

- KLSE:TOMEI

There's Been No Shortage Of Growth Recently For Tomei Consolidated Berhad's (KLSE:TOMEI) Returns On Capital

What trends should we look for it we want to identify stocks that can multiply in value over the long term? One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. So on that note, Tomei Consolidated Berhad (KLSE:TOMEI) looks quite promising in regards to its trends of return on capital.

Understanding Return On Capital Employed (ROCE)

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. To calculate this metric for Tomei Consolidated Berhad, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.16 = RM49m ÷ (RM525m - RM212m) (Based on the trailing twelve months to March 2022).

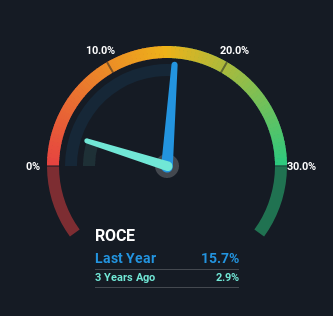

Thus, Tomei Consolidated Berhad has an ROCE of 16%. On its own, that's a standard return, however it's much better than the 11% generated by the Specialty Retail industry.

See our latest analysis for Tomei Consolidated Berhad

Historical performance is a great place to start when researching a stock so above you can see the gauge for Tomei Consolidated Berhad's ROCE against it's prior returns. If you're interested in investigating Tomei Consolidated Berhad's past further, check out this free graph of past earnings, revenue and cash flow.

The Trend Of ROCE

Tomei Consolidated Berhad is displaying some positive trends. The data shows that returns on capital have increased substantially over the last five years to 16%. The company is effectively making more money per dollar of capital used, and it's worth noting that the amount of capital has increased too, by 58%. This can indicate that there's plenty of opportunities to invest capital internally and at ever higher rates, a combination that's common among multi-baggers.

In another part of our analysis, we noticed that the company's ratio of current liabilities to total assets decreased to 40%, which broadly means the business is relying less on its suppliers or short-term creditors to fund its operations. This tells us that Tomei Consolidated Berhad has grown its returns without a reliance on increasing their current liabilities, which we're very happy with. However, current liabilities are still at a pretty high level, so just be aware that this can bring with it some risks.

The Bottom Line

In summary, it's great to see that Tomei Consolidated Berhad can compound returns by consistently reinvesting capital at increasing rates of return, because these are some of the key ingredients of those highly sought after multi-baggers. Since the stock has returned a solid 54% to shareholders over the last five years, it's fair to say investors are beginning to recognize these changes. In light of that, we think it's worth looking further into this stock because if Tomei Consolidated Berhad can keep these trends up, it could have a bright future ahead.

One final note, you should learn about the 3 warning signs we've spotted with Tomei Consolidated Berhad (including 1 which is concerning) .

While Tomei Consolidated Berhad isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

Valuation is complex, but we're here to simplify it.

Discover if Tomei Consolidated Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:TOMEI

Tomei Consolidated Berhad

An investment holding company, engages in manufacturing, retailing, and wholesale of gold ornaments and jewelry in Malaysia.

Proven track record with adequate balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|31.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|24.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|13.5% overvalued

DA

Community Contributor