Advertisement

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, CRG Incorporated Berhad (KLSE:CRG) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for CRG Berhad

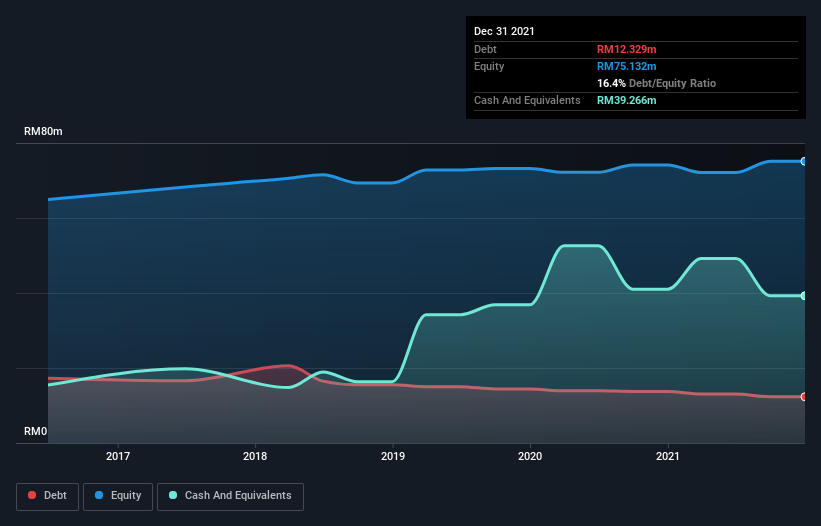

How Much Debt Does CRG Berhad Carry?

As you can see below, CRG Berhad had RM12.3m of debt at December 2021, down from RM13.8m a year prior. However, its balance sheet shows it holds RM39.3m in cash, so it actually has RM26.9m net cash.

A Look At CRG Berhad's Liabilities

We can see from the most recent balance sheet that CRG Berhad had liabilities of RM18.2m falling due within a year, and liabilities of RM26.4m due beyond that. Offsetting this, it had RM39.3m in cash and RM15.8m in receivables that were due within 12 months. So it can boast RM10.5m more liquid assets than total liabilities.

This surplus suggests that CRG Berhad has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Simply put, the fact that CRG Berhad has more cash than debt is arguably a good indication that it can manage its debt safely.

Another good sign is that CRG Berhad has been able to increase its EBIT by 27% in twelve months, making it easier to pay down debt. The balance sheet is clearly the area to focus on when you are analysing debt. But it is CRG Berhad's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. While CRG Berhad has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Happily for any shareholders, CRG Berhad actually produced more free cash flow than EBIT over the last three years. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing up

While we empathize with investors who find debt concerning, you should keep in mind that CRG Berhad has net cash of RM26.9m, as well as more liquid assets than liabilities. And it impressed us with free cash flow of RM14m, being 247% of its EBIT. So we don't think CRG Berhad's use of debt is risky. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 4 warning signs for CRG Berhad you should be aware of.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:CARLORINO

Carlo Rino Group Berhad

An investment holding company, designs, promotes, markets, distributes, and retails women's footwear, handbags, and accessories under the Carlo Rino brand in Malaysia.

Flawless balance sheet average dividend payer.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor