Advertisement

- Malaysia

- /

- Metals and Mining

- /

- KLSE:HIAPTEK

If You Like EPS Growth Then Check Out Hiap Teck Venture Berhad (KLSE:HIAPTEK) Before It's Too Late

It's only natural that many investors, especially those who are new to the game, prefer to buy shares in 'sexy' stocks with a good story, even if those businesses lose money. But as Warren Buffett has mused, 'If you've been playing poker for half an hour and you still don't know who the patsy is, you're the patsy.' When they buy such story stocks, investors are all too often the patsy.

In the age of tech-stock blue-sky investing, my choice may seem old fashioned; I still prefer profitable companies like Hiap Teck Venture Berhad (KLSE:HIAPTEK). While profit is not necessarily a social good, it's easy to admire a business that can consistently produce it. In comparison, loss making companies act like a sponge for capital - but unlike such a sponge they do not always produce something when squeezed.

See our latest analysis for Hiap Teck Venture Berhad

Hiap Teck Venture Berhad's Improving Profits

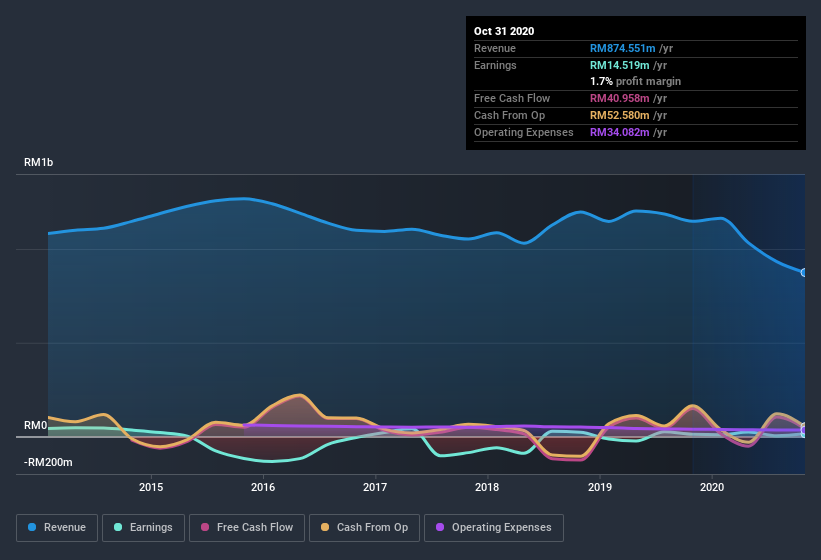

Over the last three years, Hiap Teck Venture Berhad has grown earnings per share (EPS) like young bamboo after rain; fast, and from a low base. So I don't think the percent growth rate is particularly meaningful. Thus, it makes sense to focus on more recent growth rates, instead. It's good to see that Hiap Teck Venture Berhad's EPS have grown from RM0.0087 to RM0.011 over twelve months. I doubt many would complain about that 24% gain.

I like to take a look at earnings before interest and (EBIT) tax margins, as well as revenue growth, to get another take on the quality of the company's growth. Unfortunately, revenue is down and so are margins. That is, not a hint of euphemism here, suboptimal.

In the chart below, you can see how the company has grown earnings, and revenue, over time. For finer detail, click on the image.

Hiap Teck Venture Berhad isn't a huge company, given its market capitalization of RM605m. That makes it extra important to check on its balance sheet strength.

Are Hiap Teck Venture Berhad Insiders Aligned With All Shareholders?

I like company leaders to have some skin in the game, so to speak, because it increases alignment of incentives between the people running the business, and its true owners. As a result, I'm encouraged by the fact that insiders own Hiap Teck Venture Berhad shares worth a considerable sum. To be specific, they have RM74m worth of shares. That shows significant buy-in, and may indicate conviction in the business strategy. That amounts to 12% of the company, demonstrating a degree of high-level alignment with shareholders.

Is Hiap Teck Venture Berhad Worth Keeping An Eye On?

As I already mentioned, Hiap Teck Venture Berhad is a growing business, which is what I like to see. Just as polish makes silverware pop, the high level of insider ownership enhances my enthusiasm for this growth. The combination sparks joy for me, so I'd consider keeping the company on a watchlist. You still need to take note of risks, for example - Hiap Teck Venture Berhad has 3 warning signs (and 1 which can't be ignored) we think you should know about.

Of course, you can do well (sometimes) buying stocks that are not growing earnings and do not have insiders buying shares. But as a growth investor I always like to check out companies that do have those features. You can access a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

If you’re looking to trade Hiap Teck Venture Berhad, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Hiap Teck Venture Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About KLSE:HIAPTEK

Hiap Teck Venture Berhad

Manufactures, rents, distributes, and sells steel pipes, hollow sections, scaffolding equipment and accessories, and other steel products in Malaysia.

Undervalued with solid track record.

Market Insights

Advertisement

Community Narratives

A Quality Compounder Marked Down on Overblown Fears

Fair Value US$120.72|59.6% undervalued

BA

Community Contributor

Wyndham Continues Global Expansion with 19% Ancillary Revenue Growth

Fair Value US$105.80|20.8% undervalued

ZW

Community Contributor