Advertisement

- Malaysia

- /

- Healthcare Services

- /

- KLSE:HONGSENG

Is Hong Seng Consolidated Berhad (KLSE:HONGSENG) Weighed On By Its Debt Load?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Hong Seng Consolidated Berhad (KLSE:HONGSENG) makes use of debt. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Hong Seng Consolidated Berhad

What Is Hong Seng Consolidated Berhad's Net Debt?

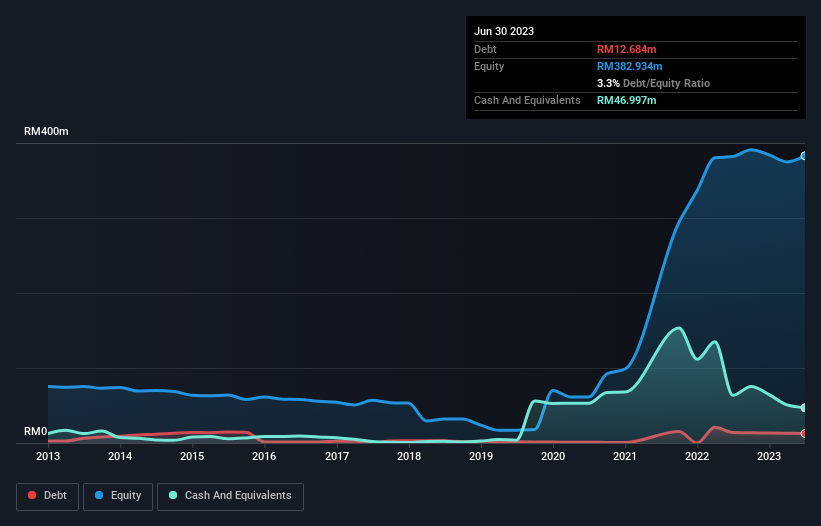

As you can see below, Hong Seng Consolidated Berhad had RM12.7m of debt at June 2023, down from RM13.9m a year prior. However, its balance sheet shows it holds RM47.0m in cash, so it actually has RM34.3m net cash.

How Healthy Is Hong Seng Consolidated Berhad's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Hong Seng Consolidated Berhad had liabilities of RM149.6m due within 12 months and liabilities of RM12.6m due beyond that. Offsetting these obligations, it had cash of RM47.0m as well as receivables valued at RM161.9m due within 12 months. So it actually has RM46.7m more liquid assets than total liabilities.

It's good to see that Hong Seng Consolidated Berhad has plenty of liquidity on its balance sheet, suggesting conservative management of liabilities. Given it has easily adequate short term liquidity, we don't think it will have any issues with its lenders. Succinctly put, Hong Seng Consolidated Berhad boasts net cash, so it's fair to say it does not have a heavy debt load! The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Hong Seng Consolidated Berhad will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Hong Seng Consolidated Berhad had a loss before interest and tax, and actually shrunk its revenue by 97%, to RM8.8m. To be frank that doesn't bode well.

So How Risky Is Hong Seng Consolidated Berhad?

Statistically speaking companies that lose money are riskier than those that make money. And we do note that Hong Seng Consolidated Berhad had an earnings before interest and tax (EBIT) loss, over the last year. Indeed, in that time it burnt through RM86m of cash and made a loss of RM27m. But the saving grace is the RM34.3m on the balance sheet. That means it could keep spending at its current rate for more than two years. Overall, its balance sheet doesn't seem overly risky, at the moment, but we're always cautious until we see the positive free cash flow. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 3 warning signs for Hong Seng Consolidated Berhad (1 is a bit concerning!) that you should be aware of before investing here.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if Hong Seng Consolidated Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:HONGSENG

Hong Seng Consolidated Berhad

An investment holding company, engages in gloves and NBL manufacturing, healthcare, and financial services in Malaysia and Australia.

Mediocre balance sheet low.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|32.0% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|21.7% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|0.5% overvalued

DA

Community Contributor